MNSO: Large-format stores fuel rev., overseas boosts profit; Is IP retail set for tailwinds?

On the afternoon of Mar 31 Beijing time, MINISO Group (9896.HK) (MNSO.N) released Q4 FY2025 results. Overall, revenue was solid and topped the high end of guidance, but the key issue remained margin pressure, i.e., higher sales did not translate into proportional profit. Key takeaways are as follows: $Miniso(MNSO.US) $MNSO(09896.HK)

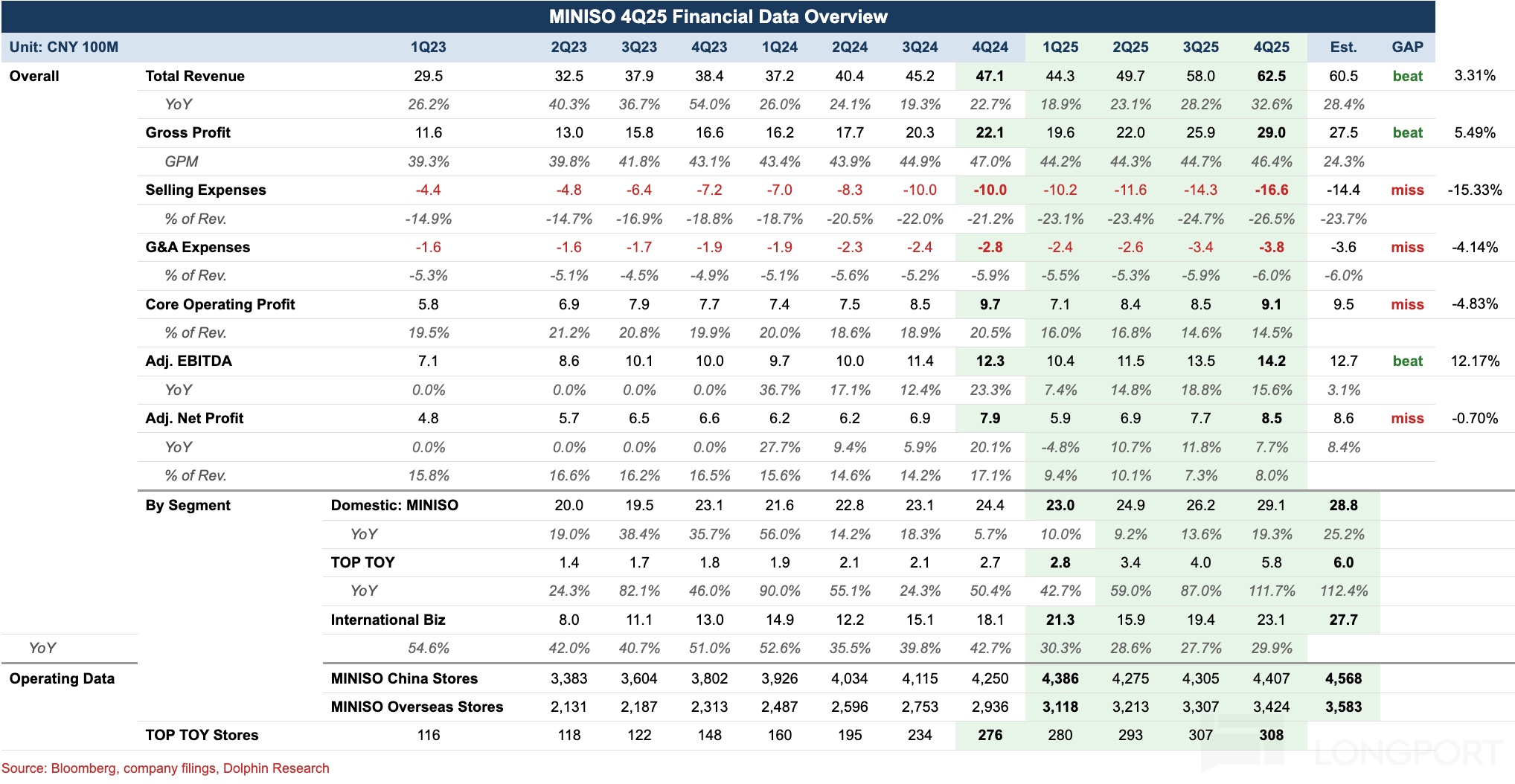

1) Revenue above guidance: Q4 FY25 group revenue reached RMB 6.25bn, up 32.6% YoY, beating the 20%-25% guidance given in Q3. By segment, helped by the full rollout of the large-format store strategy and the Nov Zootopia 2 collaboration, domestic same-store sales returned to double-digit growth, with the MINISO core brand up 25.2% YoY and accelerating QoQ. TOP TOY, driven by hit IPs such as Nommi, rose 112% YoY, extending the strong Q3 momentum.

Overseas, Southeast Asia and LatAm were weighed by business model transitions (agent-to-self-operated/strong-control models). But North America, supported by earlier cluster expansion and more refined operations, helped drive overseas revenue up 30% YoY.

2) Faster store openings QoQ. On cadence, domestic closures of many low-efficiency stores in lower-tier cities during Q1 led to a net decline in store count. From Q2, openings accelerated QoQ and peaked in Q4, with a focus on lower-tier markets including Tier-2, Tier-3 and below. Overseas added 159 stores, concentrated in high-purchasing-power regions such as North America and Europe, while the proportion of self-operated stores rose another 90bps to 19.5%.

3) Mild GPM decline. On gross margin, we infer that during shopping peaks such as Double 11 and Black Friday, the company prioritized share gains, lifting the mix of value-priced, lower-margin SKUs. In addition, to clear seasonal inventory, MINISO stepped up promotional discounts, bringing GPM down 60bps YoY to 46.4%.

4) Higher opex ratio; profit release lagged. On spending, MINISO remains in overseas expansion mode (notably North America), requiring upfront investments in openings, hiring, and brand marketing. Selling and G&A ratios both rose in Q4, with Adj. NP at RMB 850mn (+7.7% YoY), slightly below expectations.

5) Detailed financials:

Dolphin Research view:

For MINISO, the market focused on two questions in Q4: whether domestic same-store growth is sustainable and how overseas margins will recover. We address both below.

First, while the company did not disclose exact domestic same-store figures, our checks suggest Q4 same-store growth improved to high single digits, near double digits, from low single digits in Q3. This indicates the large-format strategy emphasized over the past year is delivering.

In fact, since Q2, MINISO has accelerated closing small, low-efficiency stores (under 200 sqm) while opening larger stores (new stores average nearly 300 sqm). Management indicated remodels generally lift store productivity by ~30%.

We believe the rationale is that larger stores use IP-themed zones to create immersive experiences, extend dwell time, and raise conversion; while category and SKU optimization supports one-stop shopping, boosting attachment and ATV, ultimately restoring store productivity and same-store growth. Combined with management’s disclosure that Jan–Feb 2026 saw high single-digit same-store growth, momentum remains healthy.

On profitability, the 20%+ share-price drop post-Q3 largely reflected concerns that the ramp of directly operated stores in North America and Europe would suppress overseas margins due to a mismatch between upfront investment and revenue ramp.

After MINISO localized its US leadership in 2025 (the new CEO hails from US discount retailer Five Below), two major adjustments were made in North America:

a) Cluster-based expansion: Rather than the prior scattershot approach, the new CEO focused dense expansion in 24 core states accounting for 76% of the US population (e.g., CA, FL, NY, TX). The company exited lower-density, lower-consumption regions to maximize scale effects, enabling faster warehouse-to-store replenishment and lower logistics costs.

b) Dedicated North America merchandising team: The new CEO also tailored assortments to store formats and positioning, for example increasing the share of Asian-popular IPs in CA and NY with larger Chinese/Asian communities, while favoring more practical home goods aligned with local tastes in the Midwest. This significantly reduced slow movers and lifted store inventory turns.

Our checks suggest North America operating margin improved by a low-single-digit range in Q4 (to ~6%-7% vs. ~3%-4% a year ago), which we view positively.

From a valuation perspective, guided by high-teens revenue growth in FY2026 and assuming overseas profitability (led by North America) continues to recover in line with top-line growth, our neutral case implies ~22% growth in Adj. NP to ~RMB 3.5bn in FY2026, implying ~9x, which appears undervalued. Given the solid domestic base and improving North America self-operated network, we see room for a valuation rebound and suggest trading around 10x–15x, or RMB 35bn–RMB 52.5bn market cap.

Detailed earnings analysis follows:

I. Revenue above the high end of guidance

Q4 FY25 group revenue reached RMB 6.25bn, up 32.6% YoY, above the prior 20%–25% guide.

By sub-brand, helped by the rollout of large-format stores and the Nov Zootopia 2 collaboration, domestic same-store sales returned to double-digit growth. The MINISO core brand delivered RMB 2.88bn revenue, up 25.2% YoY and accelerating QoQ. This suggests the 'Chief Growth Officer' team formed late last year by the merchandising center is effective, integrating Merchandising, Operations, Channels, Marketing, and Digital for more efficient execution than the prior structure.

As MINISO’s trendy-toy brand, TOP TOY posted RMB 600mn revenue in Q4, up 112% YoY, a single-quarter record and a standout performance.

As we noted, TOP TOY’s prior weakness was over-reliance on licensed IPs, where licensors often authorize multiple producers to maximize profits. Combined with limited differentiation in secondary design, this constrained TOP TOY’s profitability.

That changed in 2025: in H1, TOP TOY invested RMB 5.1mn for a 51% stake in HiTOY Haichuang Culture, acquiring three IPs—'Nommi', 'Honey', and 'MayMei'—to strengthen self-owned IP via M&A and control.

Results indicate that through marketing and operating its own IPs, core IP 'Nommi' delivered RMB 70mn sales in Q4, approaching 20% of TOP TOY revenue, lifting the self-owned IP mix from 10%–12% in Q3 to 18%–22% in Q4.

Beyond revenue, the surge in self-owned IPs materially improved profitability, as self-owned IPs carry GPM more than 20ppt higher than licensed IPs.

With domestic growth slowing, MINISO has placed its 'second growth curve' overseas, particularly in North America, making international growth a key investor focus.

Overall, Q4 overseas revenue reached RMB 2.77bn, up 30% YoY and accelerating QoQ.

Benefiting from Black Friday, Christmas and New Year gifting seasons, plus improved North America operations, checks suggest North America same-store growth exceeded 20%, making it the core overseas growth engine. Southeast Asia and LatAm were softer due to model transitions (agent-to-self-operated/strong-control models).

II. Store expansion in 'sprint' phase

On cadence, domestic closures of numerous low-efficiency stores in lower-tier cities during Q1 produced a net decline in store count. From Q2, opening pace accelerated QoQ and peaked in Q4, with a focus on Tier-2, Tier-3 and below markets.

Overseas added 159 stores, lifting the overseas store mix by 2ppt to 45.7%. New stores were concentrated in higher-purchasing-power regions like North America and Europe, while the self-operated share rose another 90bps to 19.5%. In more mature markets such as Southeast Asia and LatAm, the company deepened partnerships with local operators to densify and penetrate networks.

III. Further acceleration in same-store growth

For the key store productivity metric, domestic same-store growth reached mid-teens in Q4, the highest of the year.

Drivers included the continued rollout of the large-format strategy, where concepts such as MINISO LAND create IP-themed, immersive experiences that extend dwell time and lift attachment and ATV; plus more refined store operations that stimulated demand.

Overseas same-store growth was estimated at ~15%, up QoQ. Compared with frequent stockouts of bestsellers last year, improved overseas warehousing and digitalized supply chain management significantly raised in-stock rates this year.

IV. Higher opex; profits missed expectations

On GPM, we infer that during Double 11 and Black Friday, the company pushed value-priced, lower-margin SKUs to gain share. It also increased discounting to clear seasonal inventory, leading to a 60bps YoY decline in GPM to 46.4%.

On opex, the company remains in an overseas expansion phase (especially North America), facing upfront costs for openings (accelerated in Q4), hiring, and brand spending. The selling expense ratio rose 5.3ppt YoY to 26.5%, while G&A was roughly flat, resulting in Q4 FY25 Adj. NP of RMB 850mn (+7.7% YoY), slightly below expectations.

<End of text>

Related articles:

Commentary:

Nov 21, 2025 earnings take: 'MINISO: Revenue 'money printer', spending 'shredder''

Aug 21, 2025 earnings take: 'MINISO: Can large-format stores revive IP retail?'

May 23, 2025 earnings take: 'MINISO: Share slump? Without an IP soul, it cannot be the next Pop Mart'

Mar 21, 2025 earnings take: 'MINISO: Another step-up in profitability – is IP retail a 'money printer'?'

Deep dives

MINISO: From '10-yuan store' roots to the endgame of blockbuster IP retail?

MINISO: Has Shein cracked? Offline 'daily goods Shein' stands out

Risk disclosure and disclaimer:Dolphin Research Disclaimer and General Disclosures

The copyright of this article belongs to the original author/organization.

The views expressed herein are solely those of the author and do not reflect the stance of the platform. The content is intended for investment reference purposes only and shall not be considered as investment advice. Please contact us if you have any questions or suggestions regarding the content services provided by the platform.