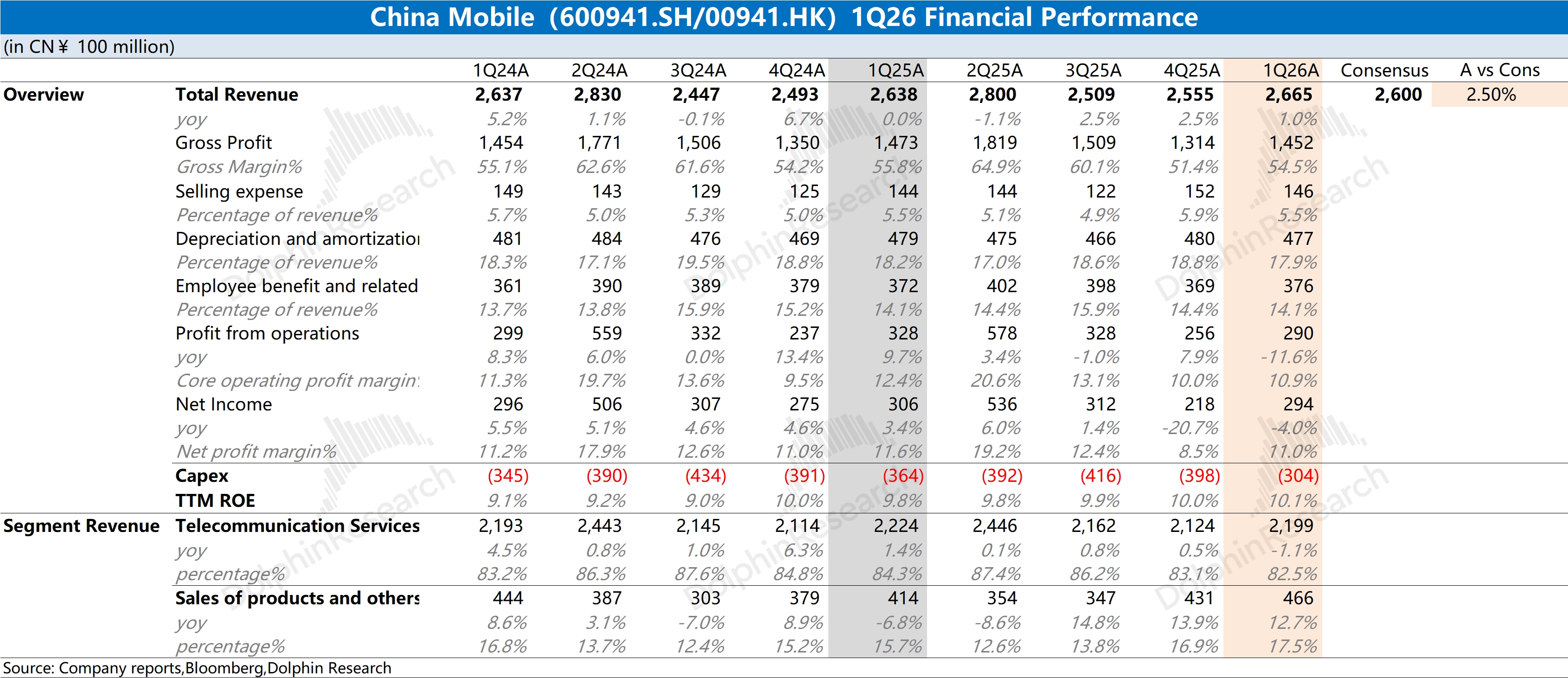

China Mobile Q1 2026 First Take: revenue grew at a low single-digit pace, while profit declined on GPM compression and higher costs.

With capex cut sharply in the quarter, after-tax cash operating profit still rose about 5%.

Connectivity remains the core biz., accounting for nearly 90% of revenue.

Mobile subscribers increased by 3.76 mn QoQ in the quarter. As the leading domestic operator, the QoQ add underscores its competitive position.

Behind China Mobile's steady print, the market is focused on three areas.

They are: a) capex, b) dividends, and c) the VAT policy shift.

a) Capex: Q1 capex was RMB 30.4bn, down RMB 6bn YoY.

Given the full-year plan of RMB 136.6bn, the remaining three quarters imply ~RMB 106.4bn in total, or ~RMB 35.2bn per quarter. As the 5G heavy investment cycle winds down, capex continues to contract.

b) Dividends: The company paid RMB 19.7bn in Q1.

Payouts are typically concentrated in Q2–Q3. Assuming a RMB 35.0bn dividend in Q2, the payout ratio would remain around 76%.

c) VAT change: Effective Jan 1, 2026, data, SMS and MMS will be reclassified from 'value-added telecom services' to 'basic telecom services'.

The applicable VAT rate will rise from 6% to 9%.

Overall, revenue and subscriber counts continue to grow, with capex trimmed and a high payout maintained.

While there are limited near-term growth drivers, it remains a solid dividend play. $CHINA MOBILE(00941.HK) $China Mobile(600941.SH) $CHINA MOBILE-R(80941.HK)

The copyright of this article belongs to the original author/organization.

The views expressed herein are solely those of the author and do not reflect the stance of the platform. The content is intended for investment reference purposes only and shall not be considered as investment advice. Please contact us if you have any questions or suggestions regarding the content services provided by the platform.