Is the semiconductor sector overbought?

① Three clues to judge: credit risk, technical momentum, and industry weight.

Data 1 shows: HYG, SPY, QQQ, and SMH are rebounding in sync, with the most critical point being that HYG is not weakening. High-yield bonds typically reflect credit risk appetite, and a strong HYG indicates the market is not currently pricing in systemic credit pressure.

In this environment, capital is re-entering risk assets, SPY is recovering, QQQ is stronger, and it's not surprising that SMH, as the most elastic direction within tech growth, is leading the gains.

This shows the semiconductor rally is not an isolated event, but a typical risk-on trading chain: easing credit risk → recovery in equity risk appetite → growth stocks outperform → semiconductors lead the rally.

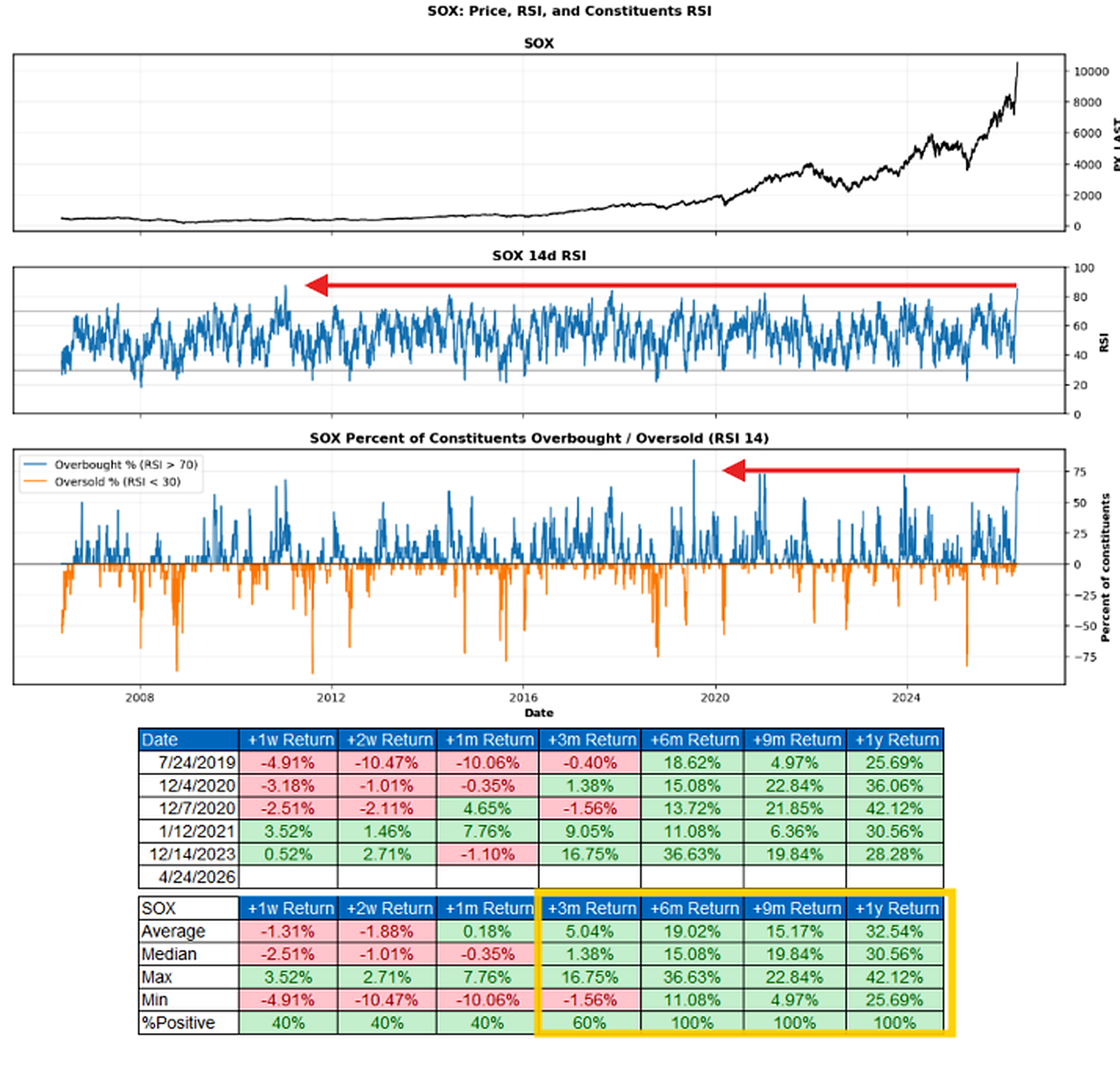

② The SOX semiconductor index has entered a short-term overheated zone.

Data 2: The 14-day RSI is near historically high levels, and the proportion of overbought component stocks has also risen significantly, meaning momentum is spreading within the sector and capital crowding is increasing.

In other words, semiconductors are not experiencing a weak rebound, but a strong trend; however, continuing to chase the rally at this level has reduced the short-term risk-reward ratio.

· Overbought does not equal a top: Strong-trend assets often continue to operate within high RSI ranges. What truly needs vigilance is not the RSI itself, but whether, as prices hit new highs, sector breadth deteriorates, leaders stagnate, or earnings expectations are revised downward.

If these signals do not appear simultaneously, judging a top simply based on "having risen too much" can lead to exiting too early.

③ The market cap weight of the US semiconductor sector has risen to a historical extreme, even surpassing highs around 2000. Data 3 provides a longer-term structural signal, indicating the market has repriced semiconductors from a traditional cyclical industry to a core infrastructure asset of the AI era.

The logic behind it is not complicated:

Continued expansion in cloud provider capital expenditure drives demand for GPUs, ASICs, HBM, advanced packaging, foundry services, and semiconductor equipment, ultimately reflected in the market cap expansion of leading companies like NVIDIA, TSMC, Broadcom, AMD, and ASML.

④ The rise in semiconductor weight is essentially a systemic revaluation of the AI industry chain. Market consensus is already very concentrated.

Semiconductors are both the strongest theme in the current US stock market and one of the most crowded trades. When a sector's weight, valuation, and sentiment are all at high levels, any rise in interest rates, credit disturbances, cooling AI capital expenditure, or underperformance of leading companies' earnings can amplify volatility.

· Semiconductors are overbought in the short term, but cannot be simplistically defined as having peaked in the medium term.

A more accurate current assessment is: Semiconductors are in a "hot, strong trend" phase. The trend remains, but the risk-reward ratio has declined; the theme is intact, but volatility risk has risen.

For existing positions, the key is not to exit immediately because the RSI is high, but to reduce leverage, control position size, and monitor HYG, the 50-day moving average, and leading companies' earnings expectations. For those not invested, it's not suitable to chase the rally emotionally now; more reasonable opportunities come from confirmation of support after a pullback.

Semiconductors are hot, but not broken yet. What truly determines an inflection point in the market is not overbought conditions themselves, but whether credit risk, AI capital expenditure, and leading companies' earnings expectations reverse.

$iShares Semiconductor ETF(SOXX.US) $VanEck Semiconductor ETF(SMH.US)

The copyright of this article belongs to the original author/organization.

The views expressed herein are solely those of the author and do not reflect the stance of the platform. The content is intended for investment reference purposes only and shall not be considered as investment advice. Please contact us if you have any questions or suggestions regarding the content services provided by the platform.