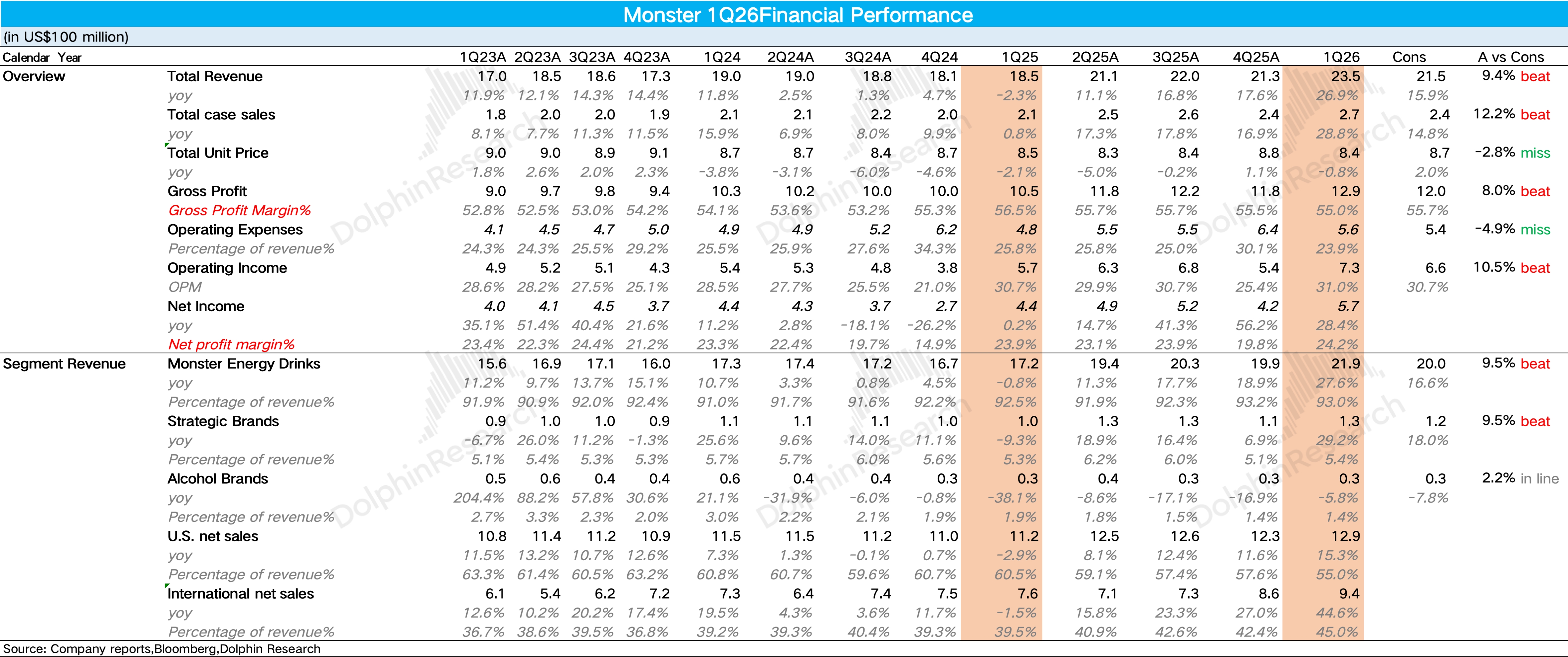

Monster 1Q26 First Take: Overall, Q1 results were very strong. Sell-side c-store trackers had already flagged double-digit growth for major energy-drink players, including Monster, so the bar was high. Actuals still topped that, with the only blemish being some GPM pressure as Intl. scaled rapidly.

1) Revenue growth surged to 27%, the highest quarterly rate in nearly four years. Monster posted Q1 revenue of $2.35bn, up 27% YoY. That beat consensus of $2.15bn (~+16% YoY).

On volume/price, unit case volume jumped 28.8% YoY to 274mn cases, the core driver, indicating strong gains across e-comm, mass, and foodservice channels. ASP slipped 0.8% YoY to $8.4 per case, weighed by a higher mix of value brands in Intl. markets.

2) Core Monster brand accelerated QoQ. The flagship Monster brand grew 27.6% YoY, faster than Q4. Beyond continued strength in the zero-sugar Ultra line, Dolphin Research believes the broader FLRT rollout in Mar drove better-than-expected initial placement and sell-through.

Other strategic brands rose 29.2% YoY, also accelerating QoQ, driven by value labels such as Predator and Fury reaching the harvest phase of distribution in emerging markets. By region, Intl. grew 45% YoY and mix rose to 45%, a record high.

3) Operating leverage continued to expand. Despite a higher mix of lower-margin Intl. and rising aluminum costs, GPM slipped 150bps to 55%. Mix and input inflation were the key headwinds.

On opex, the company is shifting from broad extreme-sports sponsorships to more efficient, data-driven digital marketing and gaming tie-ups, improving marketing ROI. Together with operational efficiencies, OPM expanded 30bps to 31.0%, beating estimates. For more detail, follow Dolphin Research's detailed take and earnings call notes. $Monster Beverage(MNST.US)

The copyright of this article belongs to the original author/organization.

The views expressed herein are solely those of the author and do not reflect the stance of the platform. The content is intended for investment reference purposes only and shall not be considered as investment advice. Please contact us if you have any questions or suggestions regarding the content services provided by the platform.