AI data center laying network cables, this one is quietly digging for gold

In this wave of AI data centers, everyone is focused on NVIDIA's H100 and B200, a few are watching Broadcom's ASICs, but—who is making money from the network cable extending from each GPU, the network responsible for letting tens of thousands of GPUs "talk to each other"?

The answer most people first think of is ARISTA. But actually, $Cisco(CSCO.US), this networking old-timer founded in 1984, has quietly risen 27% year-to-date, up 29% since the Q2 earnings release, and even surged another 4.78% in a single day on May 8th—this old stock is set to announce Q3 earnings after the US market close on 5/13 (Beijing time, morning of 5/14).

Many people's impression of Cisco still lingers on the "King of the Dot-com Bubble" from 2000—a peak market cap of over $500 billion, then a crash. But the reason this company can make money from AI today needs to be broken down.

First, what does Cisco do? The simplest understanding: the "enterprise-grade + data-center-grade" products corresponding to the WiFi router in your home. Specifically, it includes four areas: networking hardware (routers, switches), network security (firewalls, zero trust), collaboration tools (Webex), and observability platforms (Splunk). For the past two years, Wall Street has seen it as a "low-growth, stable-dividend" old-tech stock, barely justifying a 30x P/E.

So what's the turning point? It's that AI data centers have changed the game of networking.

For example. In the past, within a data center, CPU servers occasionally chatted, and 1G/10G network cables were enough. The AI era is different—ten thousand GPUs need to train, each card sending out hundreds of GB of data per second to synchronize parameters with other cards. It's like cramming ten thousand employees of a company into the same meeting room, with each person needing to talk to everyone else every minute—network bandwidth, latency, and stability instantly become decisive factors.

Cisco has played two cards in this matter.

First card: Silicon One. This is Cisco's self-developed networking chip family, which can be understood as the "GPU chip of the networking world." Q2 earnings disclosed cumulative shipments reached 1 million units, with the latest G300 architecture offering a single-chip switching bandwidth of 102.4 Tbps—hyperscale cloud providers building AI training clusters use it directly. The N9000 and 8000 series based on G300 are specifically designed for the largest AI backend fabric market in 2026-2027.

Second card: Optics. When tens of thousands of GPUs are spread apart, electrical signals aren't enough, requiring laser signals and fiber optics—this needs "optical modules." In 2021, Cisco spent $4.5B to acquire a company called Acacia Communications, specializing in coherent optics. Since then, Cisco has shipped 750,000 400G ports, 25,000 800G ports, and 100,000 1.2T DSP ports, with over 450 customers using its pluggable optical modules. The latest NCS 1014 system packs 16 800G transponders per card, with a total bandwidth of 12.8 Tbps, saving 50% rack space and 38% power compared to the previous 400G generation—this is the "infrastructure shovel" sold directly to hyperscale cloud providers building AI data centers.

Combined, these two cards resulted in Cisco reporting $2.1B in AI orders for Q2, with the full-year (FY26) AI order expectation raised to over $5 billion, of which about $3 billion is expected to convert to revenue within this fiscal year.

So for the Q3 earnings (5/13), what's worth watching isn't whether revenue can beat the $15.56B expectation, but three things:

First, will the full-year AI order guidance be raised again? The market has already taken "FY26 AI orders of $5 billion" as the starting line.

Second, Splunk synergy. Splunk is the security + observability company Cisco acquired for $28B in March 2024, and 5/13 marks exactly two and a half years. H1 added 500 customers, with a year-end target of 1000. The market wants to see if Splunk can help Cisco sell an additional subscription in enterprise renewals.

Third, gross margin guidance. The Q3 gross margin guidance given during Q2 was 65.5%-66.5%, while the market previously expected 68.2%. This gap caused the stock to drop 12% in a single day. Whether the upcoming Q4 guidance can repair this will determine whether short-term valuation can expand further.

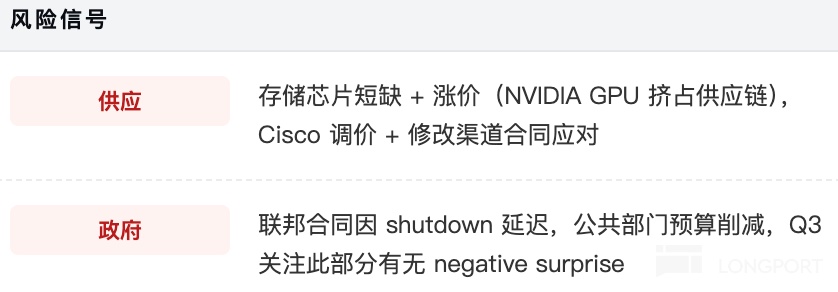

On the risk side, I have to mention a few points. Memory chip shortage—CEO Chuck Robbins himself admitted on the Q2 call that rising memory chip prices are squeezing hardware vendor costs, forcing Cisco to adjust prices and modify contract terms with channel partners. This is an industry-wide issue. Also, the previous US government shutdown caused federal contract delays, and public sector budgets were cut—Cisco's business in this area is significant, so we need to see if there will be a negative surprise in Q3.

I think the interesting thing about this stock now isn't betting on how much it will jump on earnings day, but: Cisco has finally shed the stereotype of "low-growth, stable-dividend" and repositioned itself as an "AI infrastructure stealth winner." The Silicon One + Acacia optics line is complementary to NVIDIA's system-level solutions—no matter how many H100s you buy, you still need network cables to connect them.

My judgment is, if the 5/13 earnings report raises the full-year AI order guidance from $5 billion to $5.5-$6 billion, there's still room for P/E revaluation; if the AI order numbers are flat and gross margin guidance remains conservative, the +27% gain over the past two months will face adjustment pressure. I won't bet on the direction in the short term, but for the long term, I'm willing to build a position in batches within the $85-$90 range.

The copyright of this article belongs to the original author/organization.

The views expressed herein are solely those of the author and do not reflect the stance of the platform. The content is intended for investment reference purposes only and shall not be considered as investment advice. Please contact us if you have any questions or suggestions regarding the content services provided by the platform.