MXL, up 380% in a month, insiders start selling. What happened?

$Maxlinear(MXL.US) This stock was still just over $20 in mid-April, and by May 11th Eastern Time (early morning May 12th Beijing time), it had reached $102—nearly a fivefold increase in a month. The most frequently asked question is: "What does it do? Why is it surging so much?"

I'll first dig into its background, then walk you through what happened this month step by step along the timeline.

MaxLinear makes optical communication and analog mixed-signal chips. It started by making modems for broadband TV set-top boxes, which sounds pretty boring, right? But since 2023, the company has been pivoting: moving its technology stack to data centers, creating an SSD storage accelerator called Keystone and an AI inference data movement platform called Panther. Simply put, in an AI computing factory, while GPUs are crunching numbers like crazy, data needs to be shuttled back and forth between hard drives and memory. If it can't be moved fast enough, the GPUs idle. MaxLinear makes that "data-moving shovel."

Next, let's go through the month's timeline; each step corresponds to a specific event.

April 13th (Eastern Time, same below), stock price .31—This was the starting point. The company hadn't made any major moves yet; the market was just beginning to anticipate a broader semiconductor sector recovery.

April 17th .27 (+12.5%), April 20th .73 (+20.8%)—Sector sentiment improved, MXL rose along with it, with no specific catalyst.

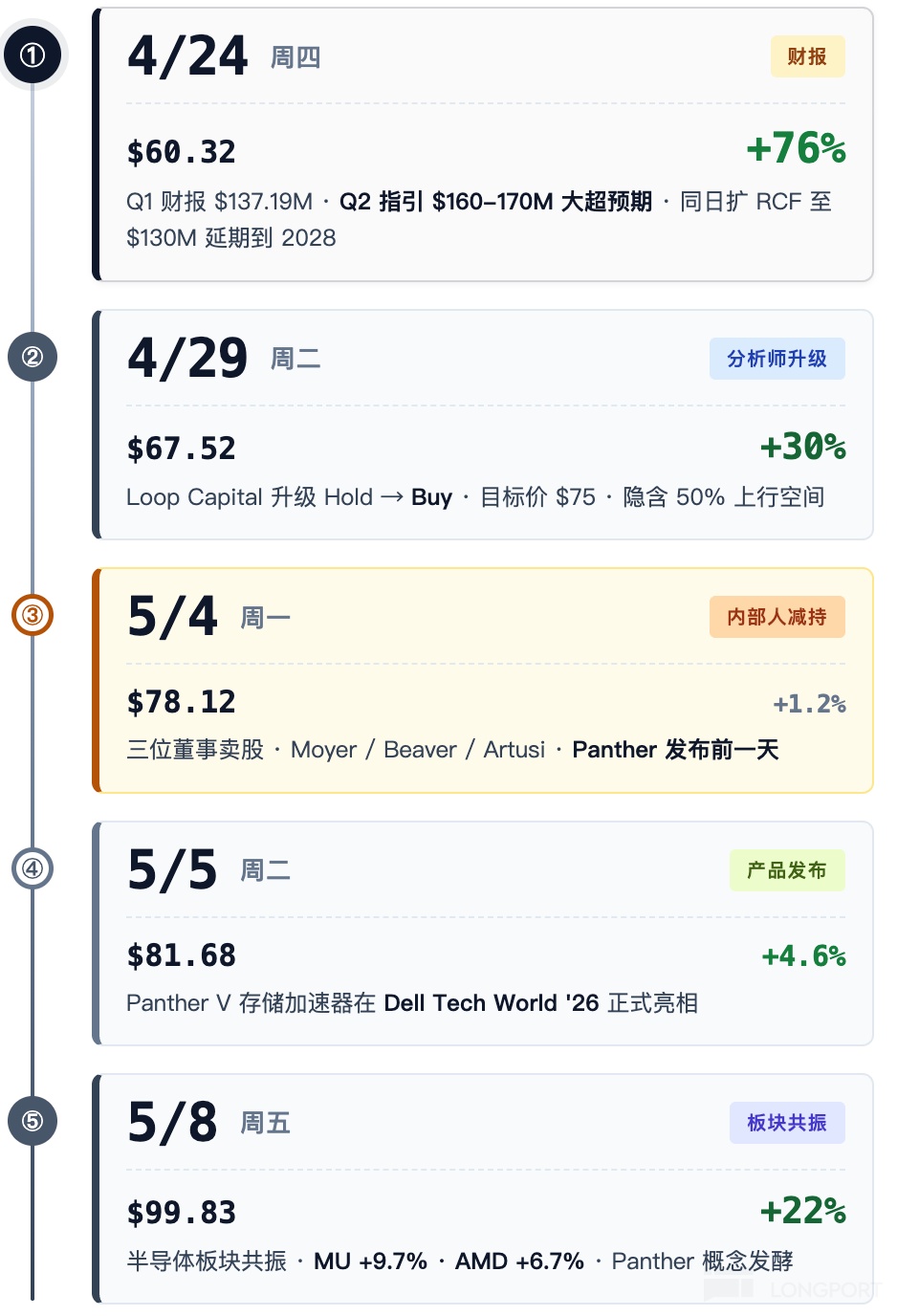

April 24th .32, single-day +76%—This was the first step. Q1 earnings were released after hours: revenue .19M, but the key was the Q2 revenue guidance of 0-170M, significantly higher than market expectations. The guidance beat was the focus because MaxLinear had been losing money for several quarters prior (net loss .14M). The market's previous expectation was "mediocre," but then it dropped a bomb—next quarter's revenue is expected to grow 25-30%. On the same day, the company also extended its 0M revolving credit facility to 2028, giving the market a "liquidity is no worry" reassurance.

April 29th .52, single-day +30%—This was the second step. Loop Capital upgraded its rating from Hold to Buy, raising the price target from (practically from the previous valuation, the original text didn't give the prior value) to —based on MXL's 4/28 closing price of , this implied over 50% upside potential. This kind of "authoritative analyst turn" has always been an amplifier for small-cap semiconductor stocks.

May 1st .18, May 4th-7th sideways trading .12-.37—Market digestion phase, no new information.

May 5th—MXL officially launched the Panther V storage accelerator at Dell Technologies World '26. The significance of this step is that it physically manifested the "Keystone sold to cloud vendors" story mentioned in the previous Q1 earnings report into a "tangible product + Dell's endorsement." This timing planted the seeds for the surge on 5/8.

May 8th .83, single-day +22.41%—This was the third step. MU rose 9.69% the same day due to AI demand, AMD rose 6.65%, and the entire semiconductor sector exploded. With Panther's concept and sector sentiment combined, MXL hit an intraday high of 0.30, closing at .83.

May 11th .27 (+2.44%)—Sentiment cooled off, but it could still hold steady above in after-hours trading.

Looking at this string of dates together, the logic chain becomes clear: Q1 earnings fundamentals laid the foundation → analyst upgrade acted as a catalyst → product launch delivered → sector resonance amplified. After these four steps, the stock price went from to 102.

But there's one thing: On May 4th, three company directors (Albert J. Moyer, Carolyn Beaver, Daniel A. Artusi) sold shares. This was the day before Panther's launch. The market's interpretation of such insider selling a few days before a launch has always been divided: one camp says it's a routine operation within the compliance window, the other says "even the executives know it's overhyped." I lean towards the latter.

Another detail I'm watching: SimplyWallSt's analysis on 4/30 estimated MaxLinear's fair value to be around .55—based on the current .27, that implies a 68% downside. Of course, that's the bearish camp's view. Optimistic analysts are still calling for 0-110, so readers should weigh it for themselves.

I think this stock's current position: the story is real, but the price has already priced in all the good news for the next two years. Q1 revenue of .19M corresponds to a current stock price of .27 and a market cap of roughly .9 billion, with a forward PS ratio approaching 15x—this is a small-cap semiconductor company that's still losing money, yet its valuation is already being priced as an "NVDA neighbor" in the AI era.

I won't chase it in the short term; I won't get on board even if it rises further—a stock that's gone up fivefold in a month could easily see a 30-40% pullback, which would be normal. But the mid-term Panther/Keystone story is real. I'll take another look when it falls back to -70 and the implied volatility drops.

The copyright of this article belongs to the original author/organization.

The views expressed herein are solely those of the author and do not reflect the stance of the platform. The content is intended for investment reference purposes only and shall not be considered as investment advice. Please contact us if you have any questions or suggestions regarding the content services provided by the platform.