Targeting $2.237 Billion by 2032: An Analysis of the 'Moat' of the Leading Orthodontic Bracket Company

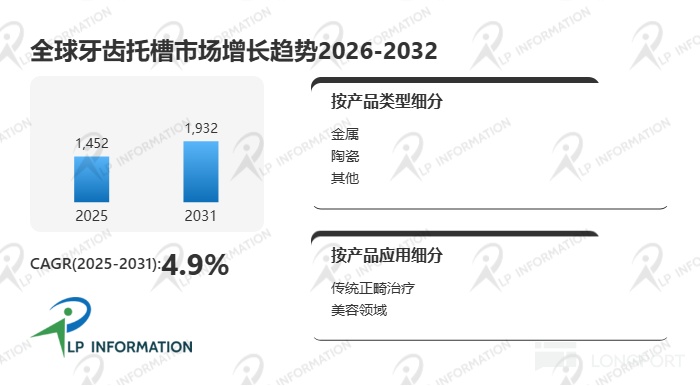

According to preliminary research by LP Information, the global orthodontic bracket market size in 2025 is approximately US$1.452 billion, and is expected to grow to US$1.932 billion by 2031, with a compound annual growth rate (CAGR) of 4.9% during the 2025–2031 period.

This report will also concurrently analyze current U.S. tariff policies and differentiated trade response measures from various countries, assessing their impact on the industry's competitive landscape, regional medical device market, and supply chain stability.

Orthodontic brackets are the core instrument components in fixed orthodontic treatment. By bonding to the tooth surface and working in conjunction with the archwire system to apply continuous and controllable corrective forces, they enable precise three-dimensional movement of teeth, thereby addressing malocclusion and dental alignment issues. Brackets are typically made from metal alloys (such as stainless steel), ceramics, or polymer composite materials, playing a crucial role in force transmission and position control within the orthodontic system, serving as an irreplaceable foundational structure for traditional fixed appliance treatment plans.

From the perspective of the industry chain structure, the upstream segment of the orthodontic bracket industry mainly includes suppliers of stainless steel, titanium alloys, ceramic materials, and polymer composites, while also encompassing precision manufacturing equipment and medical-grade surface treatment technologies; the midstream consists of orthodontic instrument manufacturers responsible for bracket design, microstructure processing, and medical registration compliance; the downstream segment comprises dental medical institutions, dental clinics, and chain dental healthcare service systems. The entire industry chain is highly dependent on the synergy of material science, precision manufacturing capabilities, and medical certification systems.

In terms of market structure, the global orthodontic bracket industry exhibits a structural characteristic of "dominance by international medical device giants + supplementation by regional brands." Companies such as Henry Schein, Dentsply, 3M Unitek, Ormco, and American Orthodontics hold dominant positions in the global market, collectively accounting for approximately 50% market share, demonstrating clear advantages in product standardization, clinical collaboration networks, and brand influence. Europe is the largest consumption region globally, accounting for about 33% of the market share, followed by the North American market at about 29%. Meanwhile, local enterprises in China and the Asia-Pacific region, such as Shanghai Emendo and Zhejiang Xinya Medical, are accelerating the import substitution process, driving the restructuring of the mid-to-low-end market.

From the perspective of the industry's policy environment, regulations on dental medical devices are continuously tightening worldwide. The European and American markets, centered around the FDA and CE certification systems, impose high requirements on material biocompatibility, long-term implant safety, and clinical validation; China, under the framework of the "Regulations on the Supervision and Administration of Medical Devices," continues to strengthen registration approval and clinical data requirements. Simultaneously, the coverage scope of healthcare systems and dental healthcare payment policies directly affect the pace of orthodontic demand release.

From the perspective of market drivers, the growth of the global orthodontic bracket market is primarily driven by multiple factors. Firstly, the significant increase in global awareness of oral health has gradually expanded orthodontic demand from the youth demographic to the adult market; secondly, enhanced aesthetic demands and the influence of social media aesthetics have led to simultaneous growth in demand for invisible and functional orthodontics; thirdly, rising incomes and the popularization of dental healthcare services in developing countries are accelerating market penetration. Additionally, the expansion of chain dental institutions and the application of digital orthodontic technologies (such as 3D scanning and digital tooth alignment) are also improving overall treatment efficiency.

However, the industry still faces certain obstacles. Firstly, the relatively high cost of orthodontic treatment remains a non-essential medical expenditure in some regions, affecting penetration rate improvement; secondly, the rapid development of invisible appliances (such as clear aligners) creates substitution pressure on traditional brackets; thirdly, the long training cycle for clinicians and insufficient operational standardization also limit the expansion speed in some markets. Furthermore, patients' concerns about long treatment cycles and initial discomfort continue to impose some constraints on demand release.

From the perspective of development opportunities, the orthodontic bracket industry is evolving towards "material upgrades + digital orthodontics + personalized customization." On one hand, the application of low-friction self-ligating brackets, ceramic clear brackets, and high-strength composite materials is continuously improving product performance; on the other hand, digital oral scanning and AI orthodontic design systems are driving the intelligence of treatment processes. Moreover, the rapid improvement of dental healthcare infrastructure in emerging markets (such as Southeast Asia, India, and Latin America) provides ongoing growth space for the industry.

By material type:

- Metal brackets

- Ceramic brackets

- Other materials

By application:

- Traditional orthodontic treatment

- Aesthetic orthodontics field

Main regions/countries covered in this article:

Americas (United States, Canada, Mexico, Brazil)

Asia-Pacific (China, Japan, South Korea, Southeast Asia, India, Australia)

Europe (Germany, France, United Kingdom, Italy, Russia)

Middle East & Africa (Egypt, South Africa, Israel, Turkey, Gulf region countries)

Main enterprises included in this article:

International and regional manufacturers such as Henry Schein, Dentsply, 3M Unitek, Ormco, American Orthodontics, Forestadent, Dentaurum, and G&H Orthodontics.

The copyright of this article belongs to the original author/organization.

The views expressed herein are solely those of the author and do not reflect the stance of the platform. The content is intended for investment reference purposes only and shall not be considered as investment advice. Please contact us if you have any questions or suggestions regarding the content services provided by the platform.