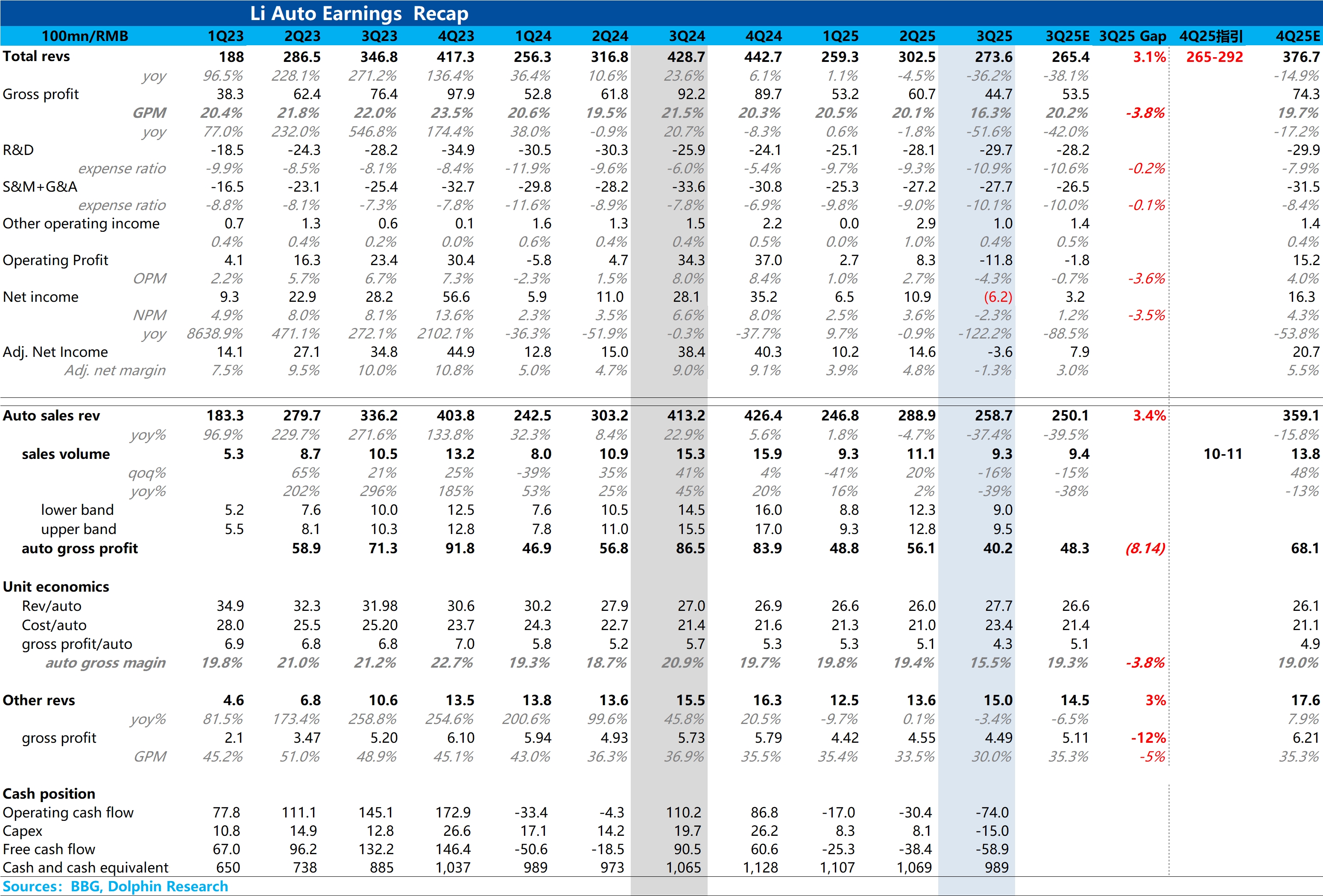

Li Auto 3Q25 Quick Interpretation: Dolphin Research's first glance at Li Auto's financial report can only be described as 'unbearable to look at,' with a significant drop in gross margin and net profi......

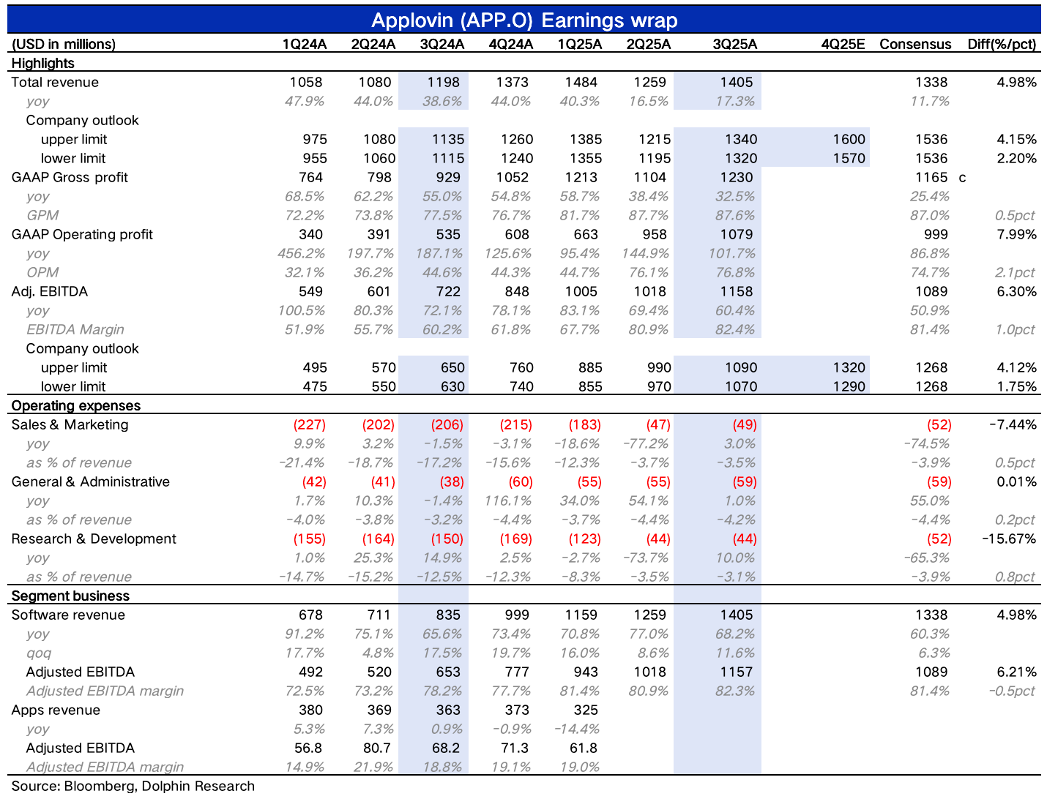

Applovin 3Q25 Quick Interpretation: Overall, it was a slightly better-than-expected strong growth, and the post-market reaction aligned with the extent of the surprise.

Before the earnings report, asid...

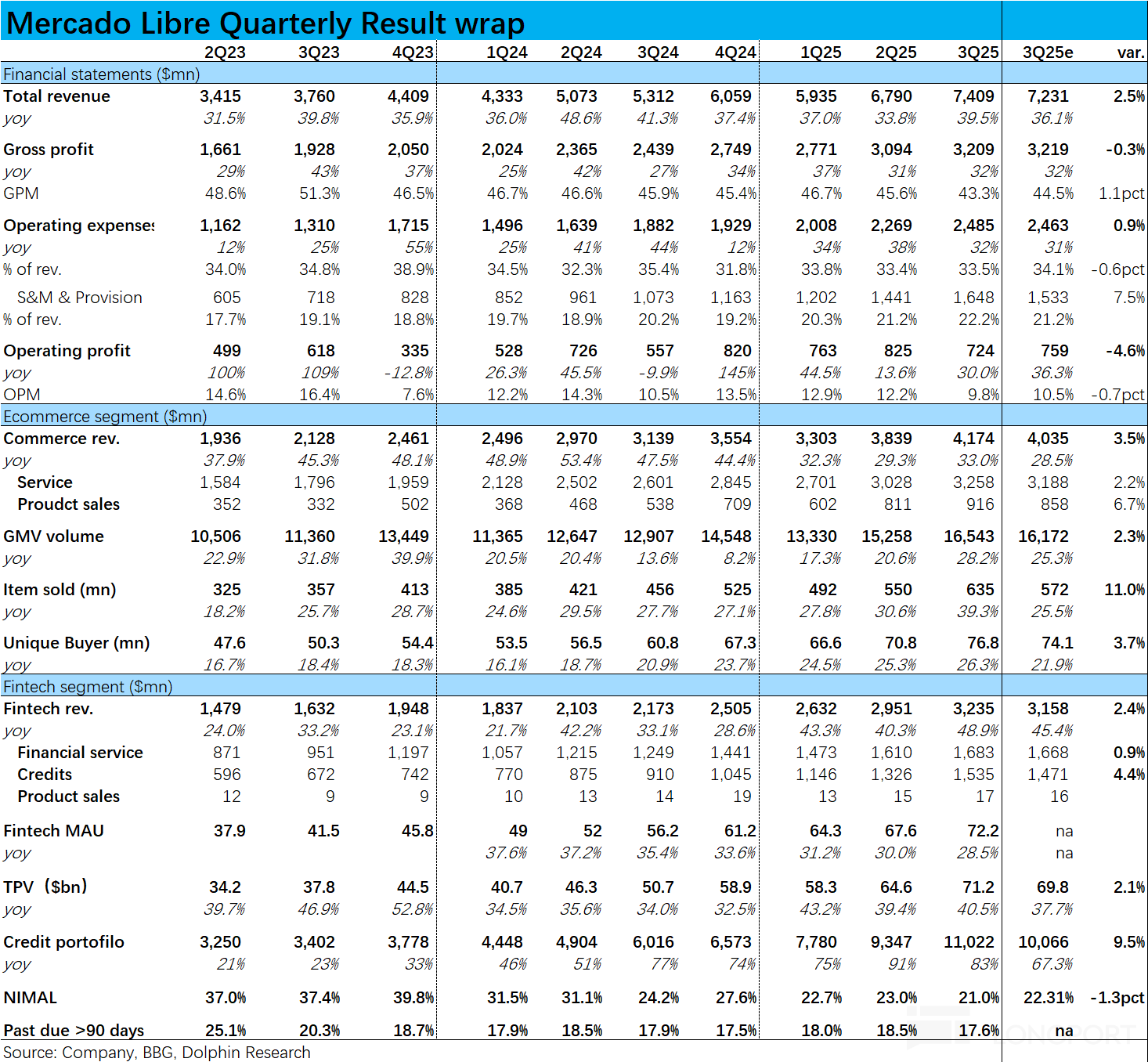

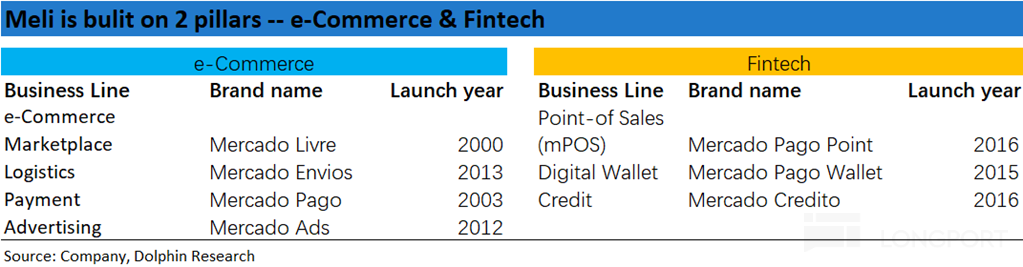

The Latin American version of "Alibaba"—$Mercadolibre(MELI.US) (hereinafter referred to as Meli) released its financial report for the third quarter of 2025 on October 30. Overall, the revenue side pe...

+6

+6

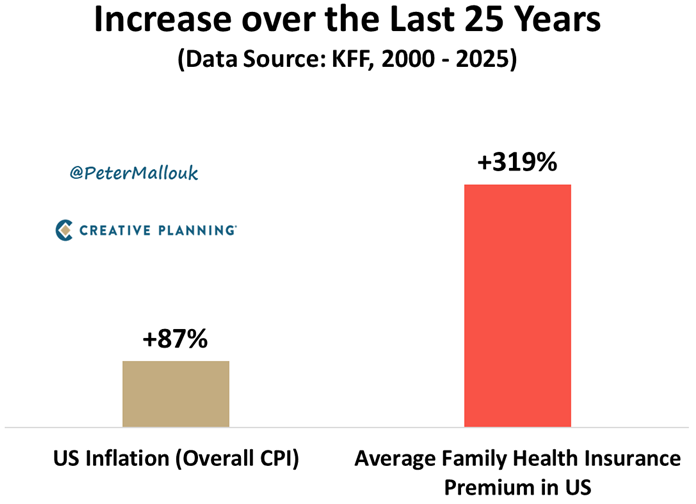

Over the past 25 years, inflation has gone up about 87%. Not great but at least somewhat predictable. What’s completely out of line is how health insurance premiums exploded 319% in that same span. Th...

...............