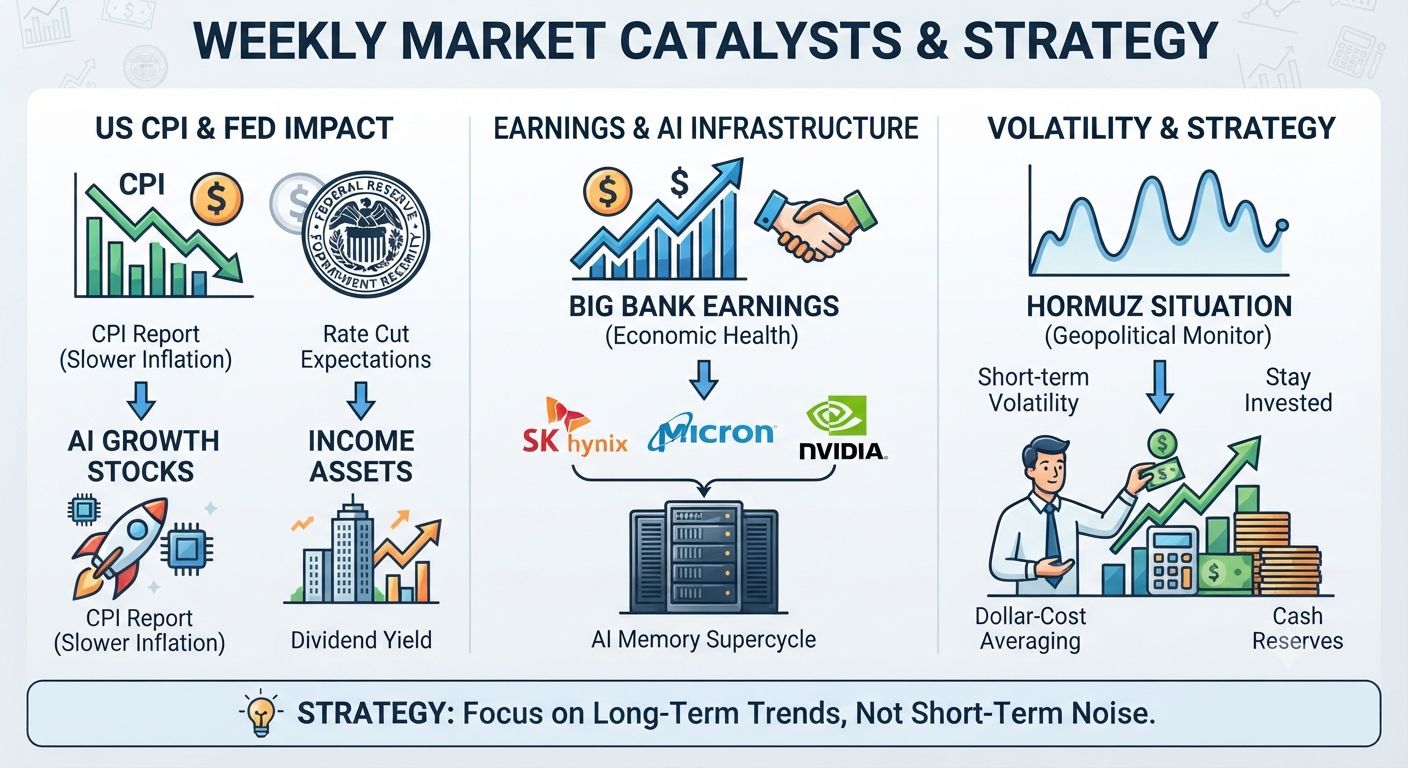

For me, the biggest catalyst this week is still the US CPI report. Inflation will shape expectations for the Fed, and that affects almost every asset class I own—from AI growth stocks to Singapore REITs and banks. If CPI comes in softer than expected, I think the market will quickly shift back to pricing in lower rates, which would be supportive for both technology and income assets.

I'm also paying close attention to the big bank earnings. They will give us an early read on the health of the US economy, loan demand, credit quality, and corporate activity. Strong guidance could reinforce confidence that economic growth remains resilient. At the same time, I'm keeping a close eye on AI infrastructure names like$SK Hynix(SKHY.US), $Micron Tech(MU.US), and $NVIDIA(NVDA.US) because I still believe the AI memory supercycle has several years left to run, and any pullback is an opportunity for me to add gradually.

The Hormuz situation is definitely something I won't ignore, but I see it more as a short-term source of volatility unless it leads to a prolonged disruption in global energy supplies. My strategy hasn't changed—I stay invested, keep some cash ready, and continue dollar-cost averaging into high-conviction companies whenever market fear creates attractive entry points. Volatility comes and goes, but long-term trends are where I believe the biggest opportunities are.