Search...

Company Encyclopedia

View More

Eco Wave Power Global AB

WAVE.US

Eco Wave Power Global AB (publ), a wave energy company, develops a wave energy conversion (WEC) technology that converts ocean and sea waves into clean electricity. The company also holds various agreements, including power purchase agreements, concession agreements, and other agreements worldwide with pipeline of projects with approximately 404.7 megawatts, as well as letters of intent. It operates in the United States, Taiwan, Sweden, Israel, Portugal, Mexico, and internationally. The company was formerly known as EWPG Holding AB (publ) and changed its name to Eco Wave Power Global AB (publ) in June 2021.

211.67 B

WAVE.USMarket value -Rank by Market Cap -/-

Valuation analysis

P/E

1Y

3Y

5Y

10Y

P/E

-

Industry Ranking

-/-

- P/E

- Price

- High

- Median

- Low

P/B

1Y

3Y

5Y

10Y

P/B

-

Industry Ranking

-/-

- P/B

- Price

- High

- Median

- Low

P/S

1Y

3Y

5Y

10Y

P/S

-

Industry Ranking

-/-

- P/S

- Price

- High

- Median

- Low

Dividend Yield

1Y

3Y

5Y

10Y

Dividend Yield

-

Industry Ranking

-/-

- Dividend Yield

- Price

- High

- Median

- Low

Institutional View & Shareholder

Analyst Ratings

- Price--

- Highest--

- Lowest--

News

View More

Posts

View More

Featured

$BitMine Immersion Tech(BMNR.US)

BMNR seems to be in its fourth wave of a huge 5 wave impulse. This ticker is best seen on a log chart (attached).

As of post, it looks to be in a bottoming process and a...

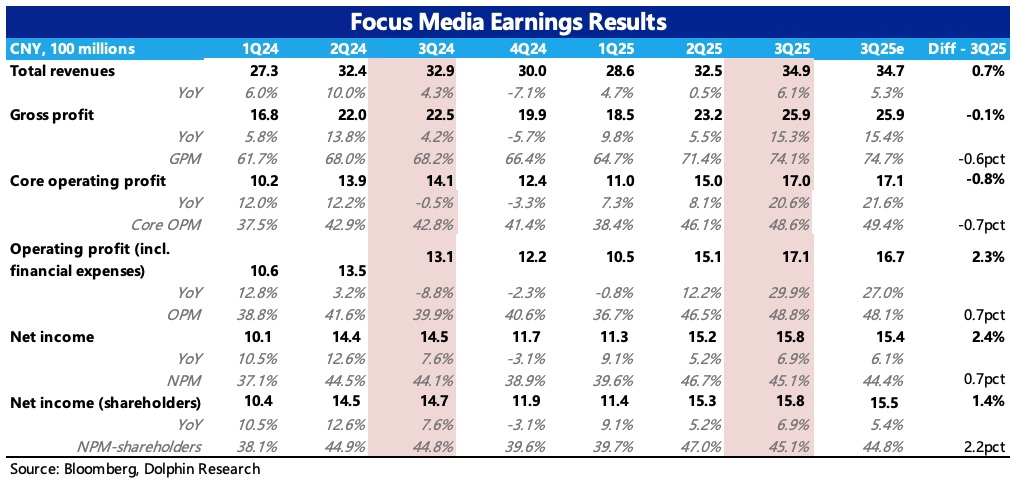

Focus Media 3Q25 Quick Interpretation: Third-quarter performance basically met expectations, with the final net profit beat mainly due to differences in expectations regarding interest, investment inc...