Figma goes public❗️Why has it become the focus of attention❓

$Figma(FIG.US) (Stock code: FIG) was listed on the New York Stock Exchange on July 31, 2025, becoming a landmark event in the tech IPO market of 2025. Its listing, valuation fluctuations, and future trends are influenced by multiple factors. Based on the latest market dynamics and analysis, the core trends are analyzed as follows:

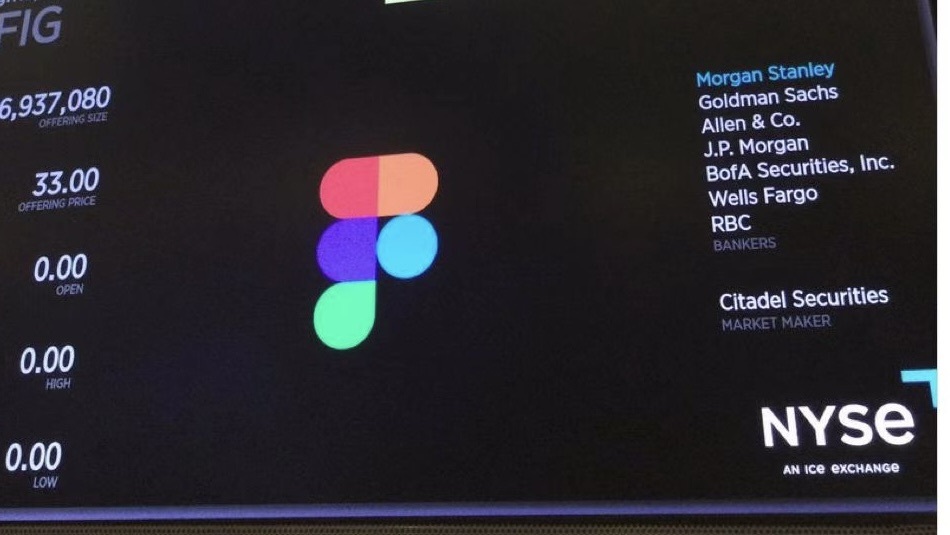

📈 1. IPO Pricing and First-Day Performance

Pricing Exceeds Expectations

- The initial pricing range was $25-$28, but due to strong investor demand (oversubscription reached 30-40 times), it was eventually raised to $30-$32, with the final offering price set at $33 (above the upper limit of the range).

- The financing scale reached $1.2 billion, with a company valuation of $19.3 billion (based on the offering price), close to Adobe's previous acquisition offer of $20 billion.

First-Day Trading Reaction

- The market predicted a first-day rise of 20%-30% (referencing similar IPOs like Circle and Chime Financial).

- Investor sentiment was high, primarily due to strong financial growth and the synergy of AI strategy.

📊 2. Financial and Business Fundamentals Analysis

Key Financial Metrics

| Metric | 2024 | 2025 Q1 | YoY Growth |

|---|---|---|---|

| Revenue | $749M | $228M | 46%↑ |

| Net Profit | Net loss of $732M | $44.9M | 314%↑ |

| Gross Margin | 88.3% | 91% | Improved |

| Net Dollar Retention (NDR) | 132% | - | Industry-leading |

Note: The net loss in 2024 was mainly due to operating costs and equity incentives; after excluding the $1 billion breakup fee from the terminated Adobe deal, actual operating profit improved significantly.

Business Strengths

- User Base: Monthly active users (MAU) reached 13 million, with over 11,000 enterprise customers (annual revenue >$100K) and 95% coverage of Fortune 500 companies.

- Product Ecosystem: AI tools (Dev Mode, Figma Make 2.0) expanded the product from design to full-process collaboration, tapping into a $47 billion market.

- Efficiency Metrics: Rule of 40 score of 63 (46% growth rate + 17% operating margin), ranking in the top 5% of the SaaS industry.

⚙️ 3. Growth Drivers and Market Positioning

- AI Strategy Deepening

- Generative AI design tools (e.g., auto-code generation, prototype generation) drove non-designer users to 67%, aiming to capture the $200 billion AI design market by 2030.

- Enterprise Stickiness and Expansion

- High retention rate (NDR 132%) + new product lines (FigJam, Figma Sites) expanded into marketing/manufacturing sectors.

- Crypto Asset Allocation

- Holds $70 million in Bitcoin ETF (Bitwise), planning to invest an additional $30 million, increasing speculative appeal.

⚠️ 4. Risks and Challenges

- Valuation Controversy

- Forward P/S ratio reached 20x, higher than peers like Adobe (~10x). If revenue growth slows below 35%, valuation pressure may arise.

- Governance Structure

- Under a dual-class share structure, CEO Dylan Field controls 73.6% voting power, weakening minority shareholders' voice.

- Competition and Macro Risks

- Threats from Adobe Firefly AI and emerging AI design tools;

- High sensitivity to interest rates—Fed rate hikes may trigger sell-offs in high-growth stocks.

💡 5. Investment Recommendations and Outlook

- Short-Term: Benefiting from IPO hype and AI premium, the stock may surge to $40-$42 (+21%-27% from the offering price), but beware of volatility from the CEO's planned sale of $658 million shares.

- Long-Term:

- Bull Case: AI monetization + enterprise expansion could drive revenue past $2 billion by 2027;

- Bear Risks: Economic recession may cut IT budgets, or AI competition could disrupt the market.

Tactical Advice:

- Aggressive Investors: Buy on dips, target $42 (12 months), betting on AI ecosystem expansion;

- Conservative Investors: Wait for Q2 earnings (August) to confirm growth sustainability, focusing on net profit and NDR metrics.

💎 Conclusion

Figma's IPO marks the 2025 tech sector recovery. Its high growth and AI integration justify premium valuation, but beware of bubbles and governance risks. Short-term trends depend on sentiment, while long-term value hinges on AI monetization and cross-sector penetration. Investors should allocate in phases, closely monitoring Q2 earnings and macro signals.

Not investment advice

The copyright of this article belongs to the original author/organization.

The views expressed herein are solely those of the author and do not reflect the stance of the platform. The content is intended for investment reference purposes only and shall not be considered as investment advice. Please contact us if you have any questions or suggestions regarding the content services provided by the platform.