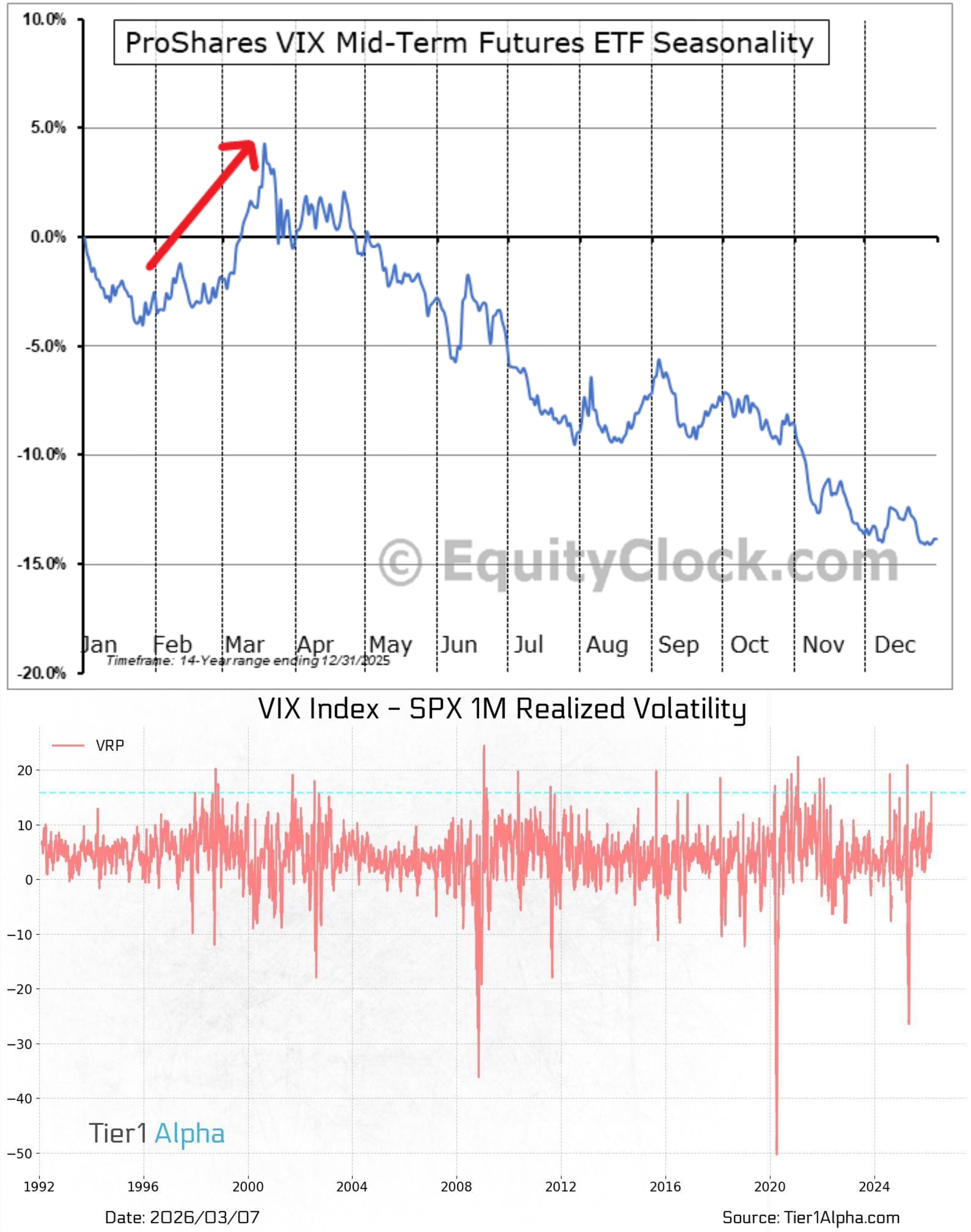

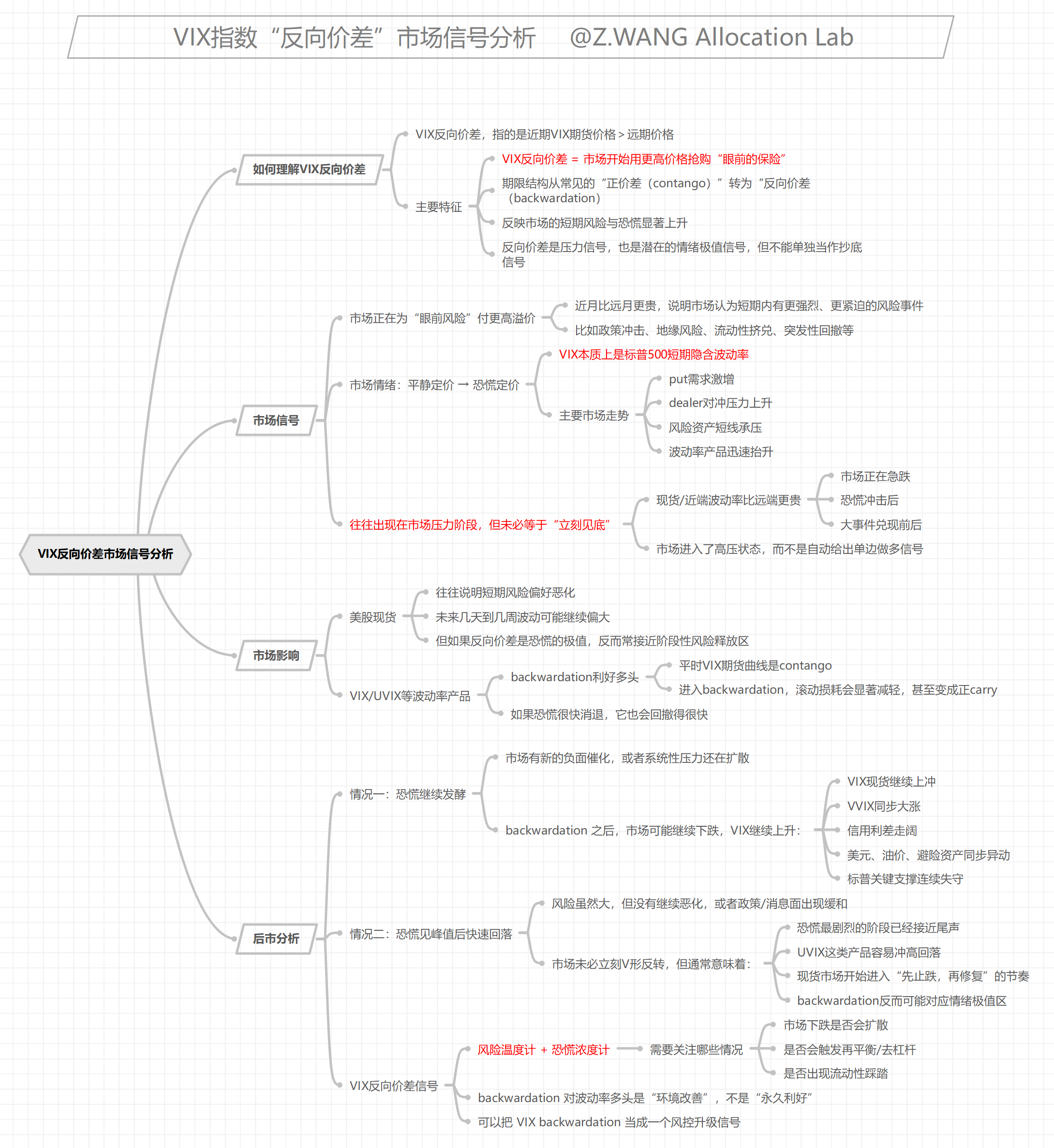

What does a VIX backwardation mean?

VIX backwardation refers to a situation where the price of near-month VIX futures is higher than that of farther-month futures, meaning the term structure has shifted from the common "contango" to "backwardation".

① A significant signal has recently emerged in the market:

The near-month VIX futures have turned into a premium relative to the next-month futures, with the term structure entering backwardation. This is usually not ordinary volatility, but rather the market starting to pay a higher premium for "immediate risks".

Cboe's explanation of the VIX term structure also points out that VIX futures are in contango most of the time. The curve only inverts significantly when short-term risks are sharply re-evaluated.

② Looking at the context this time, the triggering factors are not singular.

In early March 2026, U.S. stocks faced energy shocks from escalating Middle East conflicts, with oil prices surging sharply within a week, U.S. crude oil rising above $90, and disruptions to shipping in the Strait of Hormuz.

On the other hand, U.S. employment data weakened, and the market began to worry about dual pressures of "slowing growth + resurgent inflation". Reuters reports showed that the S&P 500 closed lower on March 6, with the VIX rising to its highest level since April 2025.

This is also why, when looking at charts alone, backwardation cannot be simply understood as "the market is about to crash". Its more accurate meaning is: short-term panic has entered a stage of concentrated pricing.

Whether it's VX1-VX2 turning positive again, or "the spread of the highest VIX futures contract relative to the spot VIX" falling below zero, the essence is the same thing – the focus of market trading has shifted from long-term uncertainty to the immediate shocks themselves.

③ Historically, such signals often have two implications:

· First, before short-term risks are cleared, volatility products have the greatest elasticity, because the rise in near-month VIX futures combined with an improving term structure will make products like UVIX more sensitive than usual.

· Second, for the spot market, it often approaches an extreme sentiment zone instead. Cboe's past research also mentions that VIX entering backwardation often corresponds to a market stress phase, but it may not necessarily continue a one-sided decline afterwards. Many times, after panic is released, the market quickly enters a recovery phase.

④ When VIX shows backwardation, what's truly worth paying attention to is not "whether one can bottom-fish immediately", but two things:

· First, whether the inversion continues to deepen;

· Second, whether risks continue to spread to the levels of credit, liquidity, and earnings expectations.

If high oil prices, geopolitical conflicts, and growth concerns resonate, backwardation may persist longer;

But if the marginal impact of events eases, it often means the most intense panic trading has already been priced in by the market in advance. This is also the most critical judgment watershed for the current market.

Data source: 2026.Mcclellan Financial Publications

$2x Long VIX Futures ETF(UVIX.US)

$Pro Ultr Cvix Shrt Futures(UVXY.US)

$-1x Short VIX Futures ETF(SVIX.US)

The copyright of this article belongs to the original author/organization.

The views expressed herein are solely those of the author and do not reflect the stance of the platform. The content is intended for investment reference purposes only and shall not be considered as investment advice. Please contact us if you have any questions or suggestions regarding the content services provided by the platform.