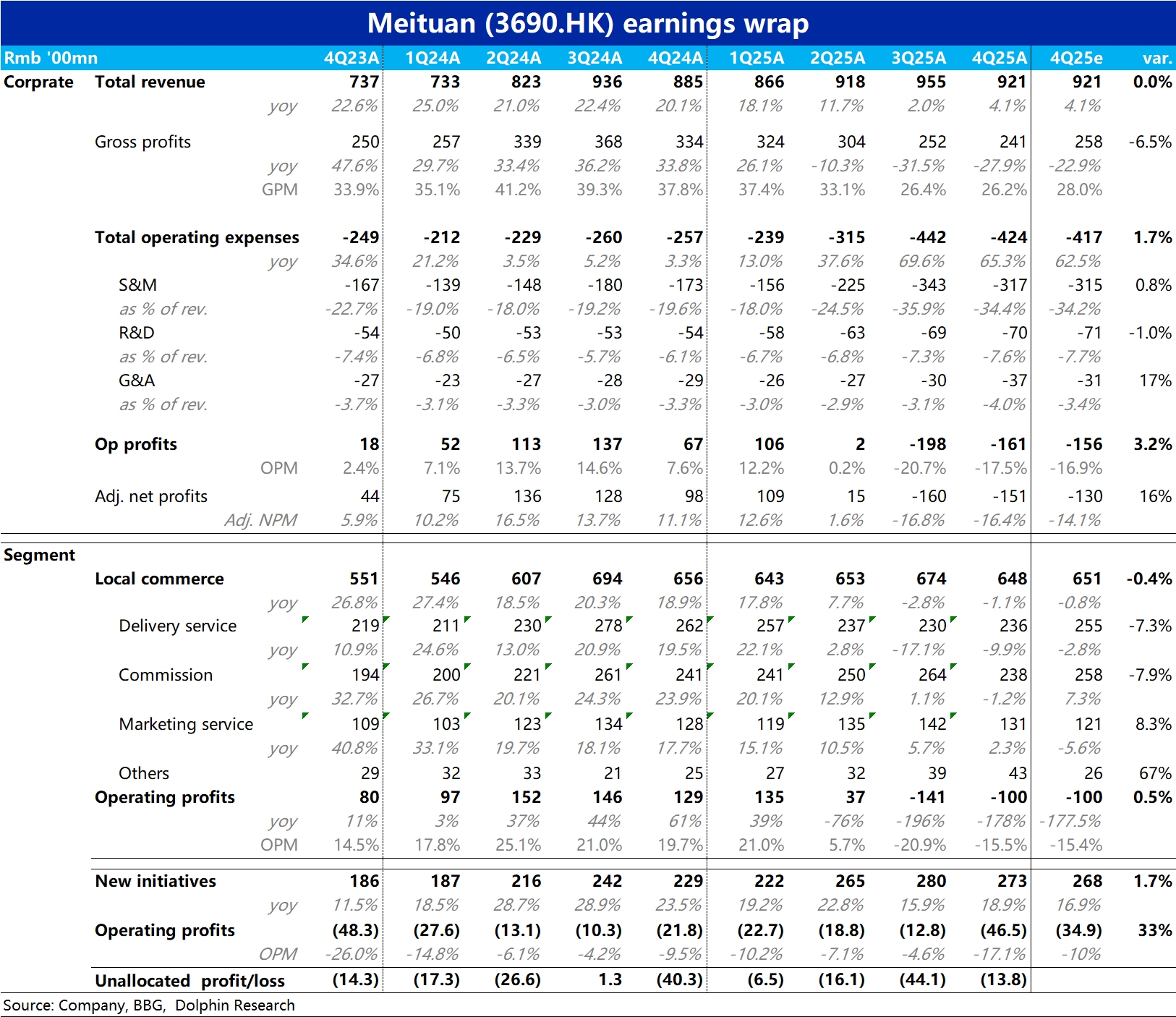

Meituan 4Q25 First Take: With the prior profit warning, losses under GAAP for Core Local Commerce and the group were largely flagged, so the headline print was broadly in line. That said, underlying profitability still came in a bit below expectations.

In detail, two points stand out. See below.

1) First, by segment. Losses in new initiatives were ~RMB 1.2bn above expectations.

2) On costs and expenses, GP clearly missed while OP roughly matched forecasts. This is because non-operating items booked within OP this quarter, including changes in financial asset values and other gains/losses, totaled ~RMB 2.2bn, distorting the true profit picture.

On a core OP basis (GP minus S&M, R&D and G&A), the quarter posted a loss of ~RMB 18.3bn. Compared with ~RMB 19.0bn in the prior quarter, the narrowing was actually very limited.

In other words, on an underlying basis, most of the improvement in Core Local Commerce was offset by losses in new initiatives. As for key metrics, Core Local Commerce revenue decline narrowed from ~3% YoY last quarter to 1% YoY, and marketing spend fell by ~RMB 2.5bn QoQ; these align with the industry-wide pullback in food delivery spending and losses, and were broadly in line with expectations, with nothing particularly noteworthy. $MEITUAN(03690.HK) $Meituan(MPNGY.US) $MEITUAN-WR(83690.HK)

The copyright of this article belongs to the original author/organization.

The views expressed herein are solely those of the author and do not reflect the stance of the platform. The content is intended for investment reference purposes only and shall not be considered as investment advice. Please contact us if you have any questions or suggestions regarding the content services provided by the platform.