AI’s Hard Limit: Compute Boom Meets a Power Crunch; Gas Turbines the Hidden Boss?

In the prior piece 'AI 竞赛终局:电力说了算?', Dolphin Research argued that the U.S. power shortfall is not a cyclical mismatch but a structural conflict between surging AI compute and long‑lagging energy and grid build‑out. This is not a near‑term issue that supply-demand cycles can easily resolve.

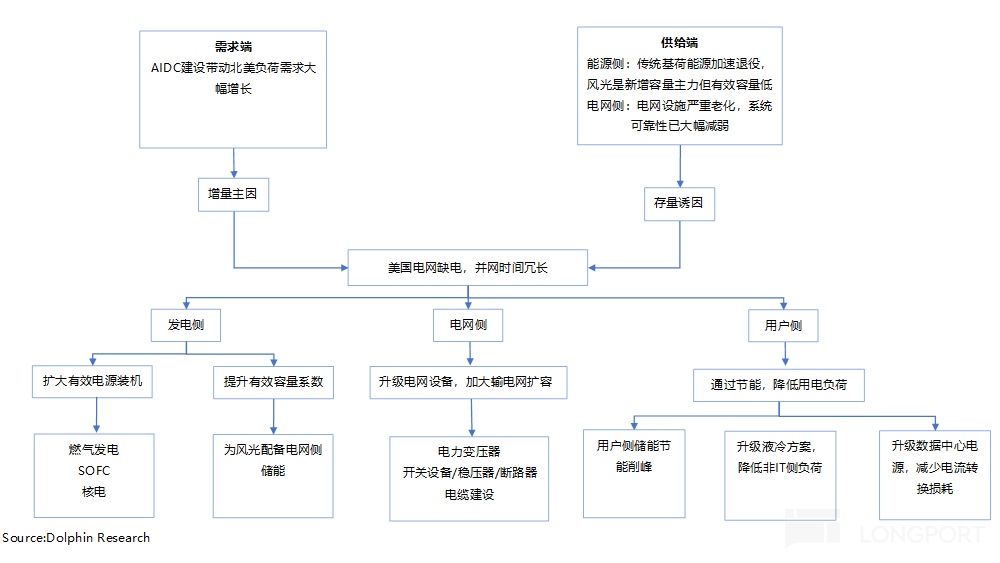

On the demand side, reshoring of manufacturing and the inflexible load from AI data centers are pushing electricity demand into an accelerated growth phase, with peak‑load pressure rising sharply. Load profiles are becoming both larger and peakier.

On the supply side, traditional high‑reliability baseload is retiring, while wind and solar’s 'energy substitution' cannot fill the 'capacity gap', leaving effective supply inadequate. On the grid side, aging assets, under‑investment, tight critical equipment supply and long build cycles are amplifying the imbalance. These constraints compound each other.

In this piece, Dolphin Research will dig into: 1) How to resolve North America’s structural power shortage? 2) Supply options: which are effective for AIDC power, and where are the investable angles?

1. How to resolve North America’s structural power shortage? Given AI‑driven load tearing apart the supply-demand balance, there is no single silver bullet. Policy must address supply, transmission and consumption in parallel, with 'time certainty' at the core.

The near‑term priority is speed over cost to secure 'fast power on' behind the meter. Over the medium term, systemic investment is needed for 'sustained good power' via grid upgrades and nuclear.

1) Supply side: lock in 'firm capacity' and go off‑grid with self‑build

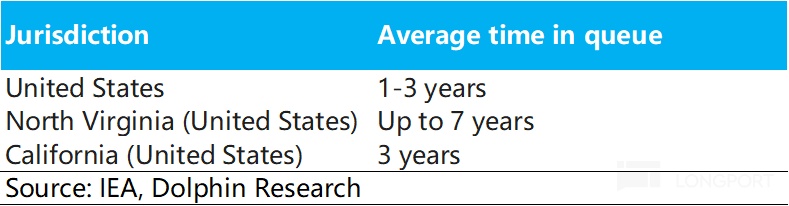

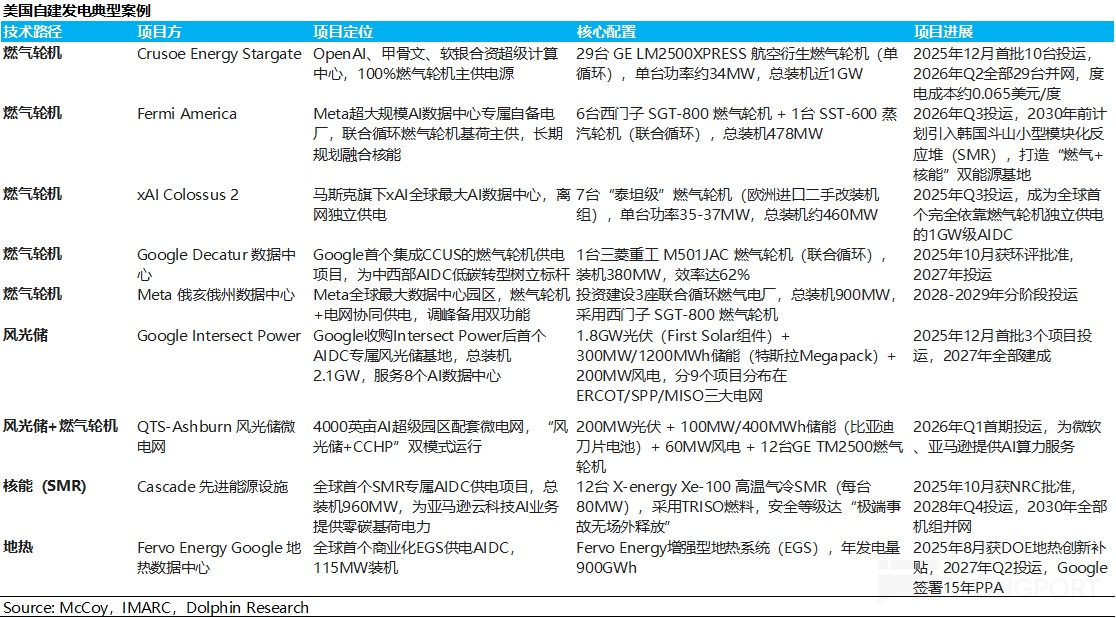

a. Off‑grid self‑build is now Big Tech’s default: To bypass 3–5 years, even 7 years, of interconnection queues, tech majors are pivoting to self‑build, shifting from 'drawing from the grid' to 'self‑generation, avoiding interconnection'. They are turning to distributed resources such as gas turbines, SOFCs and small modular reactors (SMRs), while U.S. Senator Tom Cotton has proposed the 'DATA Act of 2026' to allow data centers to trade 'physical isolation' for FERC oversight exemptions, creating a potential legal path to fully go off‑grid.

Musk’s xAI is bypassing the grid by purchasing five heavy‑duty gas turbines (380MW each) from Doosan Heavy Industries, building a 1.9GW standalone microgrid as a benchmark for the off‑grid model. Google paid a 4.75bn premium to acquire Intersect Power to capture locked‑in grid interconnection rights, effectively 'buying time' with capital.

b. Expand effective capacity on the supply side: Within the U.S. mix, resources that offer high effective capacity factors and sufficient headroom include gas turbine generation, SOFC fuel cells and nuclear. These are the most practical near‑to‑mid‑term levers.

c. Lift effective capacity factors: Pairing wind/solar with storage to time‑shift output can turn intermittent resources into dispatchable capacity, mining incremental 'firm' supply from the stock. This combo upgrades variability into usable capacity.

2) Grid side: expansion and upgrades are the long‑term inevitability The grid is the physical backbone connecting generation and load, and congestion from poor interconnection (queues up to 7 years in some areas) stems from aging and insufficient lines. Upgrading and adding transmission is essential to accommodate geographic rebalancing of new loads.

This will drive a supercycle in transformers (the grid’s heart), high‑voltage switchgear/circuit breakers and copper/aluminum cables. Transformers are already the key bottleneck, with delivery lead times stretched. Supply is the tightest at this node of the chain.

3) User side: fine‑tune for 'efficiency gains' and 'load management' When 'sourcing' is constrained, data centers’ ability to save and flex load becomes bargaining chips for interconnection approval. Utilities value flexible demand.

a. Add storage to shave peaks and fill valleys: Behind‑the‑meter storage can lower a site’s peak demand, arbitrage time‑of‑use spreads, and replace diesel gensets as backup. More importantly, storage smooths AI’s violent load swings, reducing 'poor quality' shocks to the grid; in PJM and ERCOT, storage is now a must‑have for interconnection and queue shortening.

b. Cut non‑IT energy use: Data center total energy = IT load + cooling + power distribution losses. Cooling tech upgrades: As air cooling hits limits at high densities, liquid cooling from cold plates → micro‑channels → immersion becomes mandatory, lowering PUE to allocate more power to compute. Power architecture shift (HVDC/SST): To serve MW‑class racks, power delivery is moving to 800V HVDC, cutting conversion losses, footprint and copper. Solid‑state transformers (SSTs), with >98% conversion efficiency, are the next‑gen AIDC core; Nvidia expects volume production from 2027.

We therefore expect U.S. power tightness to drive: 1) build‑out of high‑reliability capacity sources such as gas, nuclear and SOFCs; 2) broad‑based storage demand on both grid and user sides;

3) demand for grid engineering equipment; 4) AIDC power upgrades, fueling strong demand for HVDC/SST and related electrical gear; 5) upgrades in data center liquid‑cooling solutions.

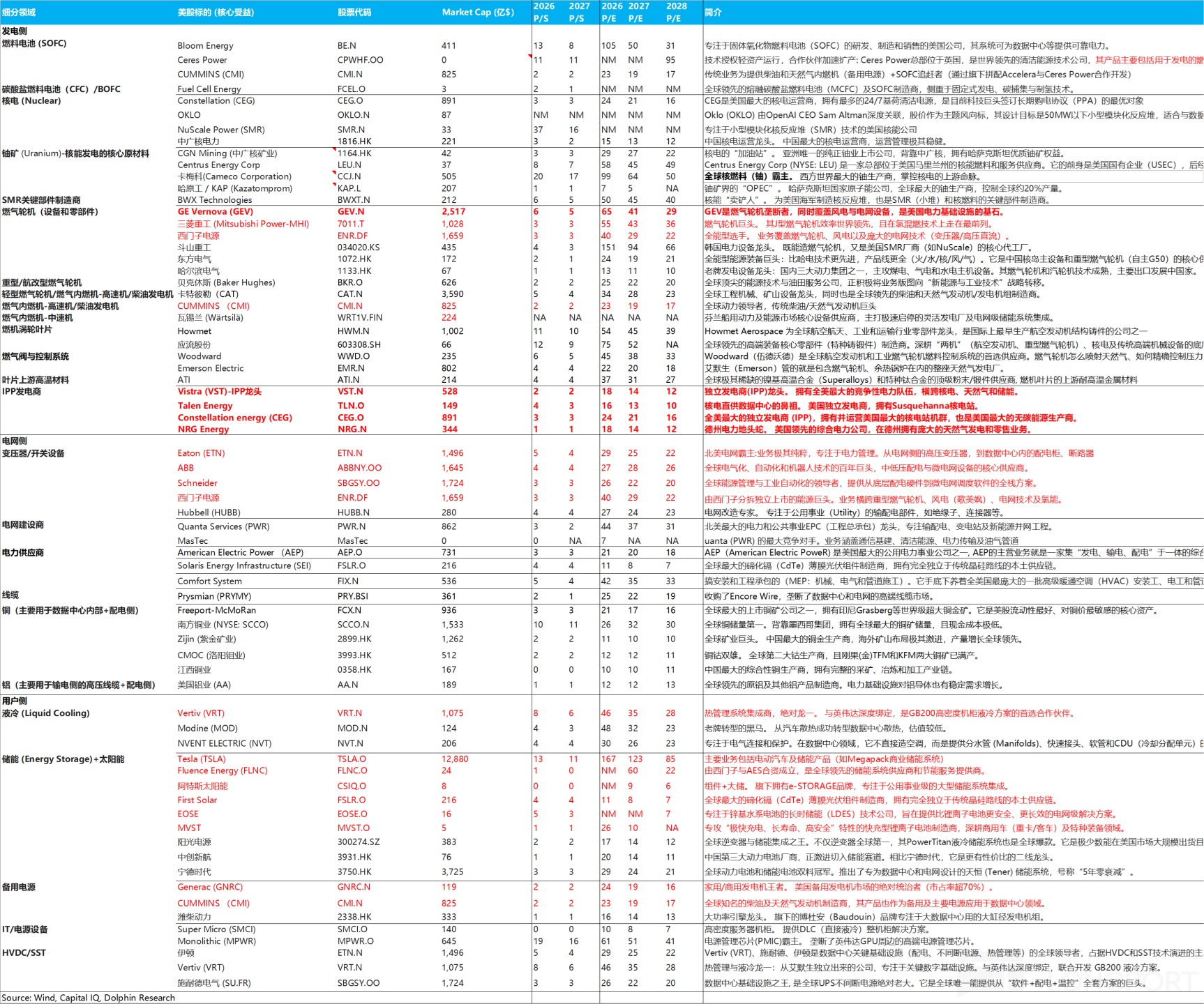

Along this value chain, Dolphin Research has compiled the key beneficiaries; see AI 电力与能源股单 for names and investment logic.

2. Supply side: which solutions power AIDC effectively?

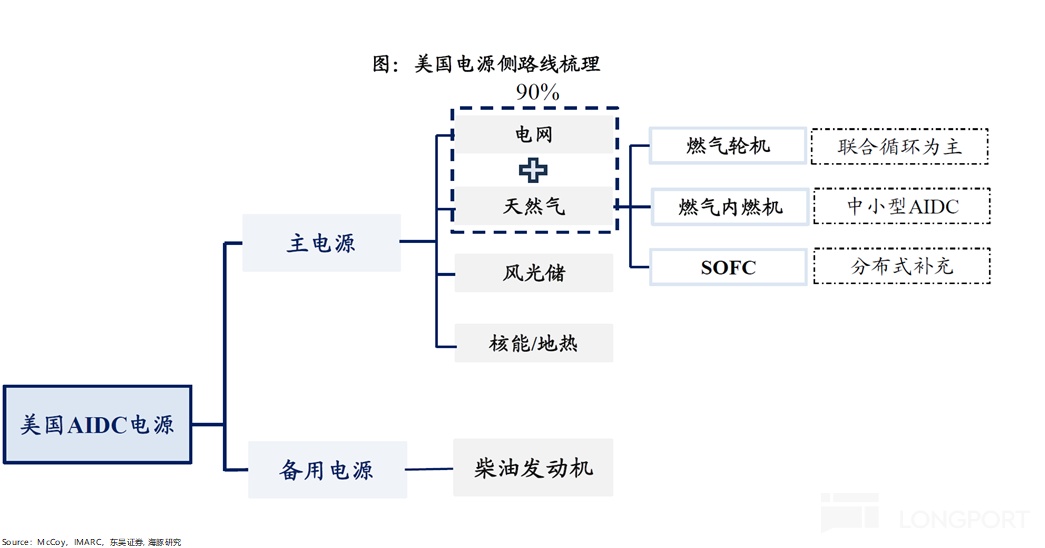

Demand side: off‑grid self‑build is gaining share Facing exhausted grid capacity and long interconnection queues, U.S. AIDC is shifting toward on‑site generation and microgrids. Supply architectures split into primary and backup sources.

Primary power: covers 100% of base load, often over‑provisioned to 120%–130% of Max Load for redundancy. Backup power: the last resort (e.g., diesel gensets), often optimized to ~50% of Max Load in microgrids, ensuring only core AI compute and key cooling loops survive a full primary outage.

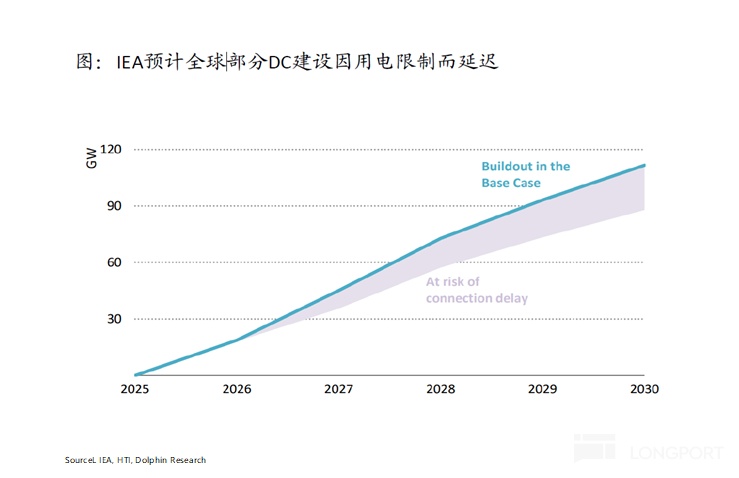

Bloom Energy’s survey points to a regime shift in power architectures. By 2030, 38% of data centers are expected to adopt on‑site generation, with 27% fully off‑grid and 100% reliant on on‑site primary power; by 2035, the on‑site share could approach 50%. This marks a historic inflection.

From the demand side, U.S. data center buyers pick primary energy based on 'reliability floor, delivery first, TCO‑optimal' principles. Their priorities, in order:

1) Power performance (hard constraint): 7x24 continuous, stable output, tightly matching AI’s millisecond‑scale swings (40%–100% power changes). This is non‑negotiable.

2) Delivery time (key competitive factor): AI chips depreciate fast, so waiting for power imposes huge opportunity costs. Users will pay up for faster delivery; in fact, speed now often trumps absolute cost and determines who wins the compute race.

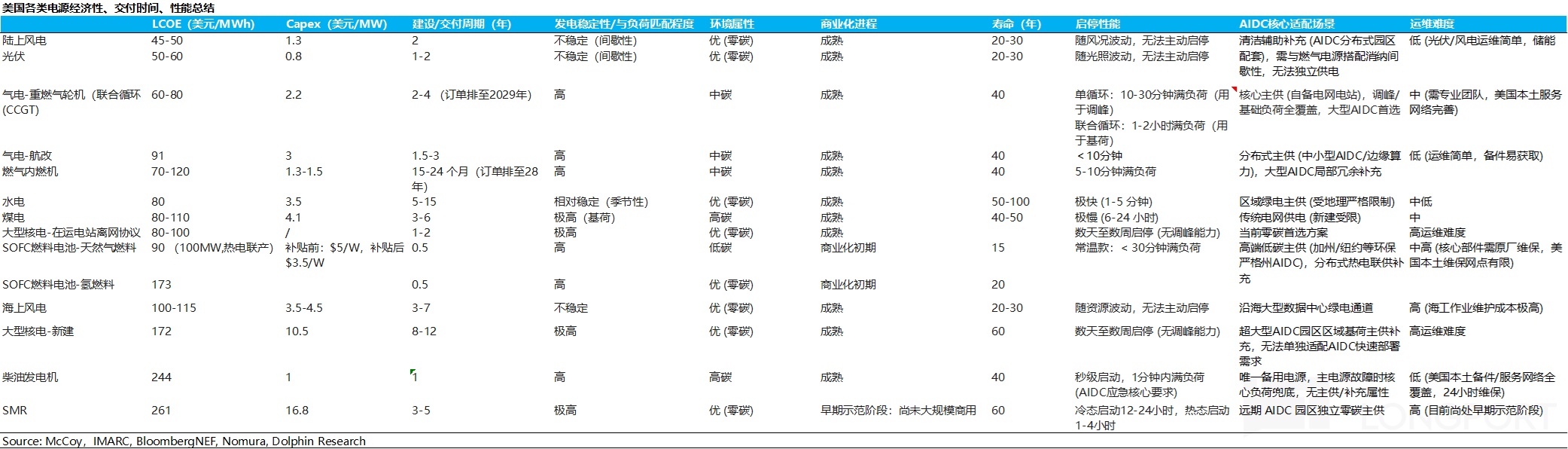

3) Economics (core over the long run): While speed matters near‑term, long‑run economics boil down to LCOE, which blends upfront capex, fuel, O&M, utilization and life. Lowest‑LCOE options have the strongest staying power.

4) ESG: The Big Four clouds (Amazon AWS, Microsoft Azure, Google Cloud, Meta) drive ~half of North America’s new DC builds and have pledged 100% renewables. They increasingly prefer 'certificate + electrons aligned' physical green power over buying certificates alone.

However, given hard constraints around performance, delivery and cost, ESG is often monetized in decisions. In PJM, RECs trade around $10–20/MWh, so buyers may choose 'RECs + non‑green power', translating ESG into an incremental economic cost; over time, regulation and brand pressure will strengthen the tilt to physical green power. This preference should only grow.

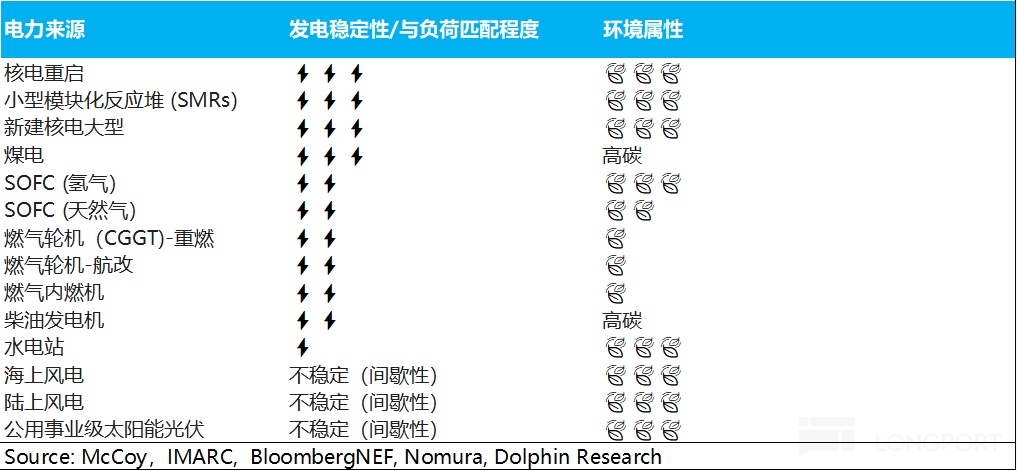

Main on‑site options include: (i) gas turbines; (ii) fuel cells; (iii) reciprocating engines; (iv) PV; (v) geothermal; (vi) SMRs. Applying the above principles, we screen the mainstream paths:

1) New energy (wind/solar) excluded as primary: Despite best‑in‑class LCOE ($40–50/MWh) and green credentials, intermittency and volatility fail the 7x24 stability test. Given today’s poor economics of 'wind/solar + long‑duration storage', these can only supplement baseload, not serve off‑grid primaries.

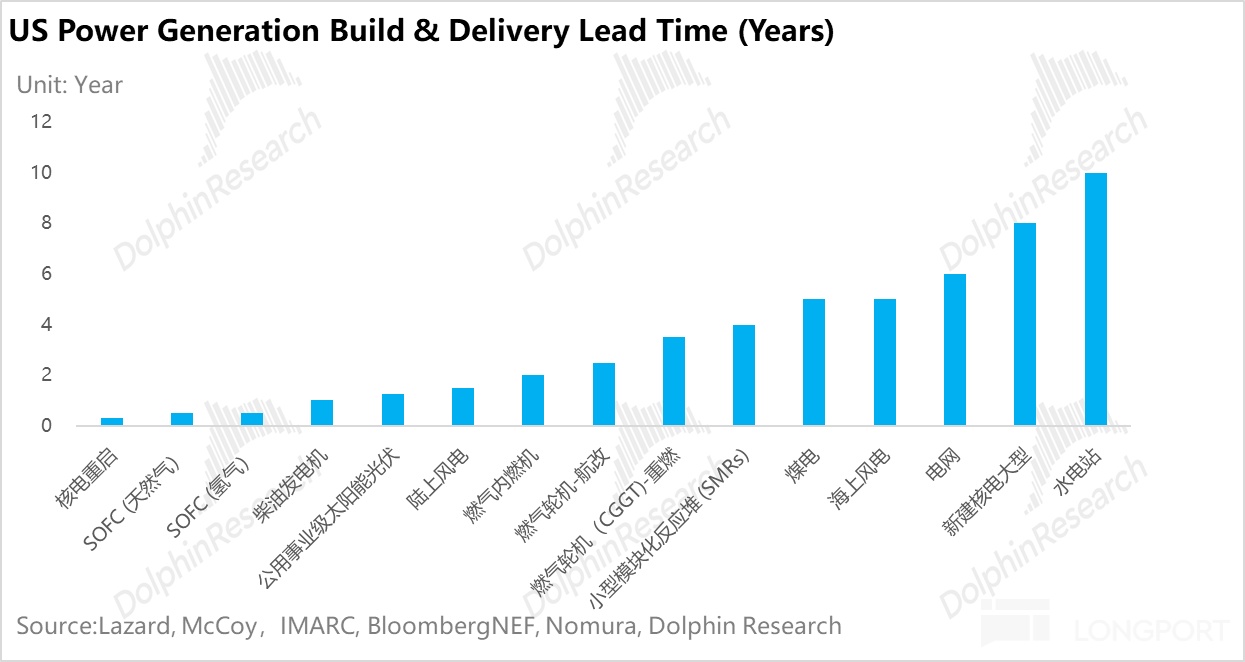

2) Nuclear/SMR/hydro have long delivery cycles: Traditional nuclear, SMRs and hydro take 5–15 years to build. Big Tech is committing capital to SMRs (e.g., Oklo targets 2028), but current projects are mostly long‑dated VC‑type bets, mismatched with AIDC’s 2–3 year expansion window. Near‑term penetration logic is thin.

That said, under persistent geopolitical risks in traditional energy, global nuclear and SMR long‑dated value may be re‑rated.

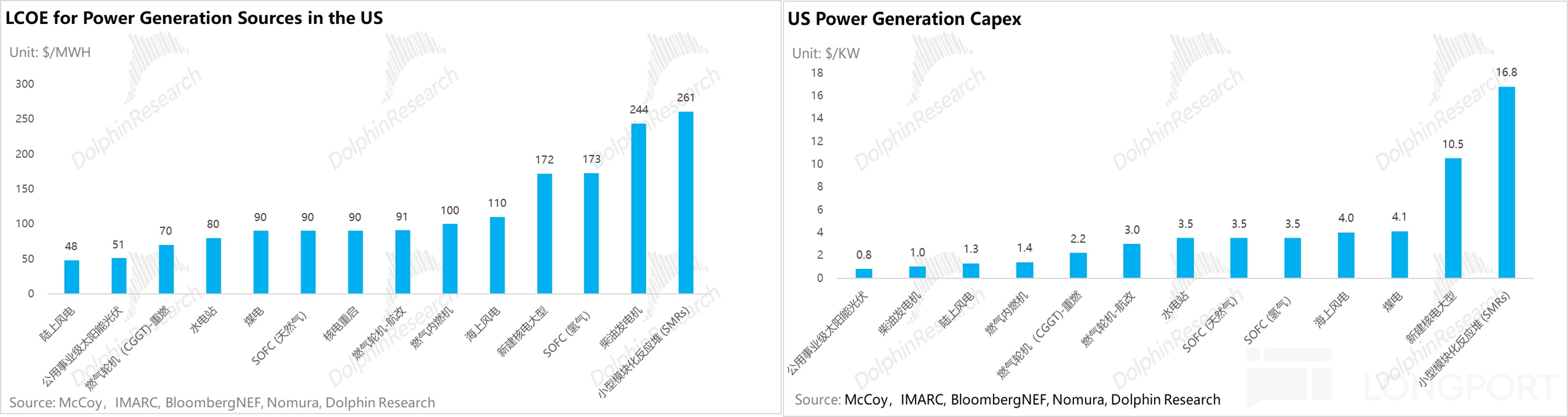

3) Mainstream options with mid‑range economics and reasonable delivery: Under current tech and supply chains, scalable solutions cluster at $70–100/MWh LCOE.

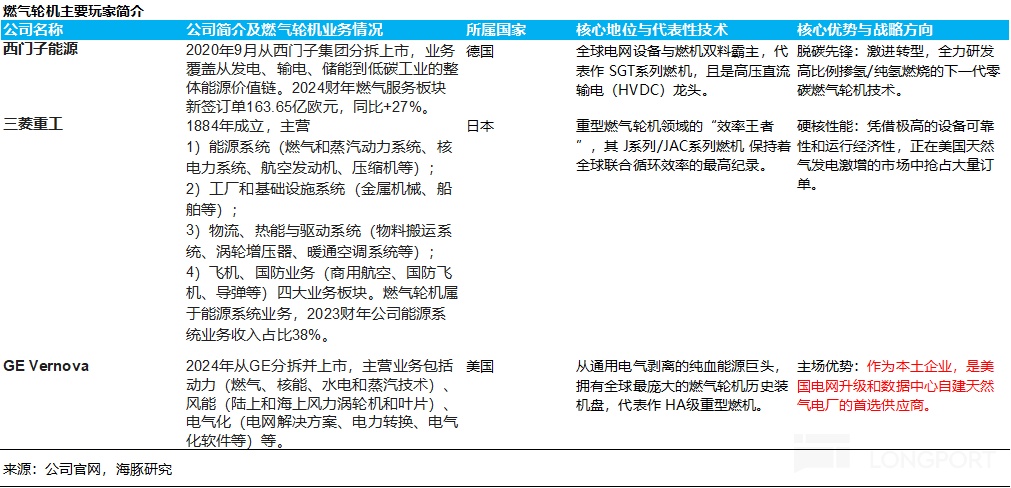

Heavy‑duty gas turbines (combined cycle): lowest LCOE (~$70/MWh), most mature and efficient, the theoretical optimum. But supply is extremely tight; major OEMs (GE Vernova, Siemens, Mitsubishi) are booked out to 2028–2030.

SOFCs (natural‑gas fuel cells): ~ $90/MWh LCOE, with ultra‑fast deployment (as quick as 90 days), high conversion efficiency and low CO2. Drawbacks are higher upfront capex (~$3.5/W after ITC) and early‑stage commercialization.

Aero‑derivative gas turbines: ~ $91/MWh LCOE, with 1.5–2.5 year delivery and flexible starts/stops, a compromise between efficiency and time, but at higher unit capex (~$3/W). Good for fast ramp and modularity.

Gas reciprocating engines: higher LCOE (~$90–120+ /MWh) and lower cycle efficiency, but the lowest capex (~$1.4/W) and 1–2 year delivery. They track volatile loads well, reaching full power in 5–10 minutes.

Balancing stability, delivery speed and lifecycle cost, Dolphin Research sees gas turbines, gas engines and SOFCs as the three pillars of self‑built power for data centers, with complementary roles: 1) Gas engines: with the lowest capex (~$1.4/W) and fast deployment, they will capture 'race‑against‑time' demand spilling over from heavy‑duty turbine shortages, dominating mid‑small projects, peaking and distributed use. 2) Gas turbines (combined cycle): as OEM capacity frees up over the next few years, their low LCOE and high efficiency will reassert dominance in large AIDC baseload.3) SOFCs: as scale drives capex down, their 'speed + efficient low‑carbon' profile will shine for sites with strict ESG, footprint and deployment needs.

Given North America’s structural tightness, the trio should co‑exist: 'turbines for baseload, engines for peaking/distribution, SOFCs for rapid roll‑out'. Cases from Amazon and Google using turbines as core primaries validate gas turbines as 'the current optimum for AIDC power', with engines and SOFCs as essential complements.

3. Where are the investable opportunities under the effective supply solutions?

1). Gas turbines: the optimal AIDC power solution, but capacity is tight

a. Beyond delivery and economics, gas turbines fit AIDC requirements exceptionally well:

① Performance fit (steady baseload, agile peaking): Stability: combined‑cycle availability exceeds 95%, with lower forced‑outage rates than coal, delivering weather‑independent 7x24 high‑quality baseload to keep AI training uninterrupted. Flexibility: rapid start and ramp (heavy‑duty to full load in ~30 min; aero‑derivatives in ~10 min) lets turbines smooth intermittent wind/solar and, with storage, handle minute‑level AI load swings.

② Spatial fit (extreme power density): Single‑unit output ranges from 5–500MW in compact footprints. Versus land‑intensive wind/solar or bulky diesel fleets, turbines deliver GW‑scale power on minimal land, especially aero‑derivatives, ideal for space‑constrained AIDC campuses.

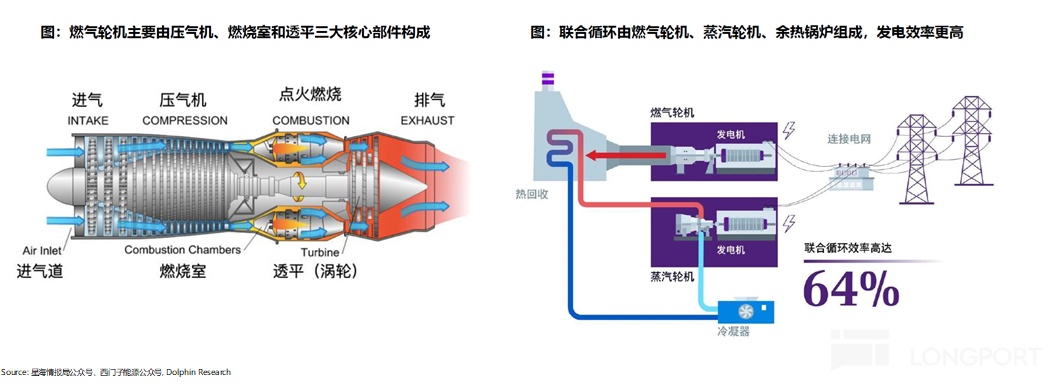

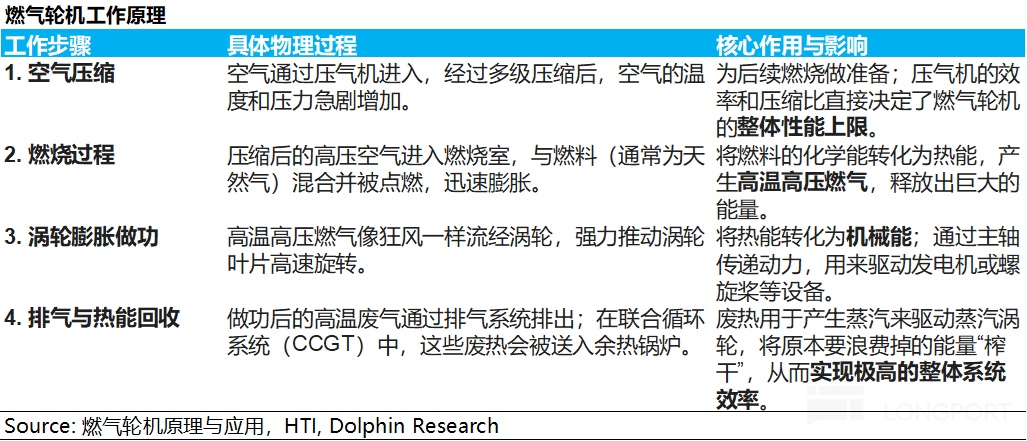

b. What is a gas turbine? It combusts natural gas to generate high‑temperature, high‑pressure gas that spins a turbine to drive a generator, closing the chain from chemical to thermal to mechanical to electrical energy. The physical cycle is intake/compression, combustion/heating, expansion/work and exhaust/heat release, executed by three core modules: compressor, combustor and turbine.

Depending on how exhaust heat is handled, two mainstream generation modes address different use cases: ① Simple cycle: ultra‑fast starts for flexible peaking

Mechanism: compressed air mixes with fuel and burns, directly driving the turbine and generator; hot exhaust is vented. Without heat recovery, efficiency is lower (~35%–40%), but with a streamlined system it offers small footprints and very fast response. In AIDC, it suits rapid interim deployment and sharp peaking during compute surges.

② Combined cycle: cascade utilization for efficient baseload Mechanism: add HRSG and a steam turbine to harvest ~500–600°C exhaust to produce steam for a second‑stage turbine. The 'GT + ST' tandem lifts overall efficiency above 60% without extra fuel, the most efficient gas‑fired mode today and the ideal choice for large‑scale baseload.

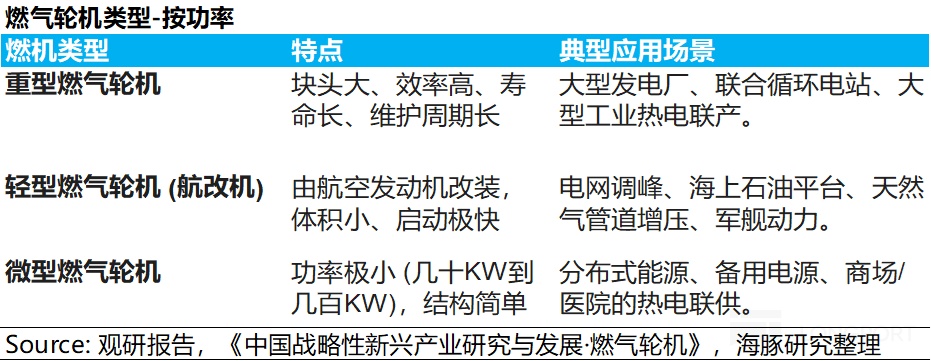

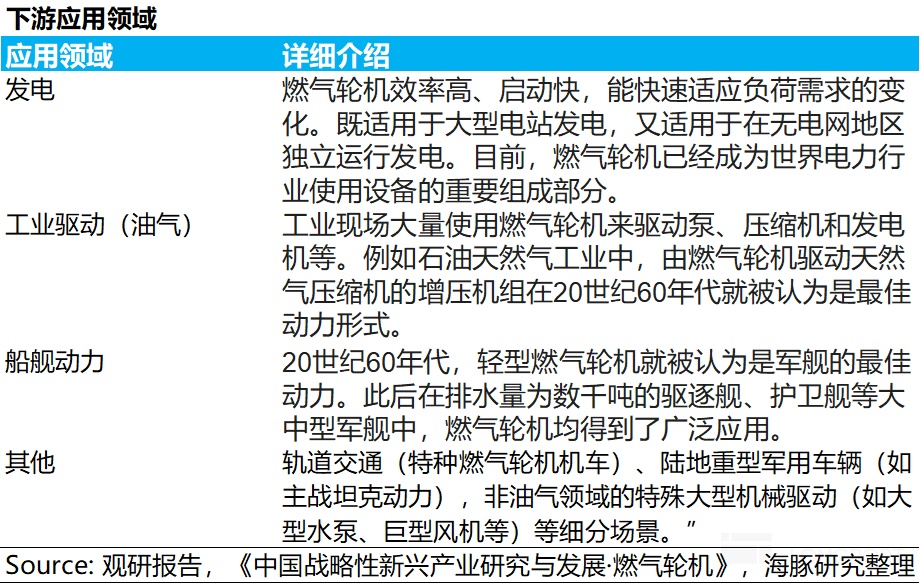

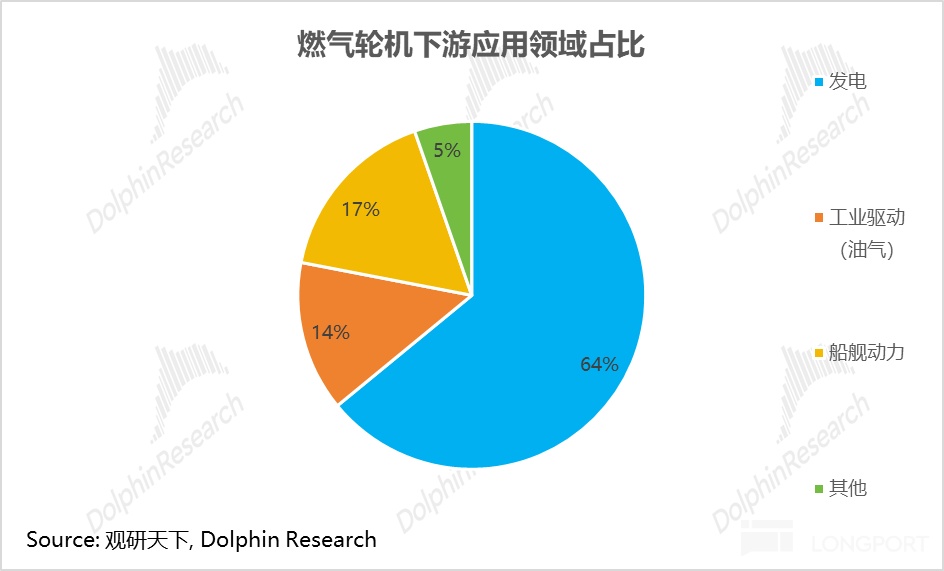

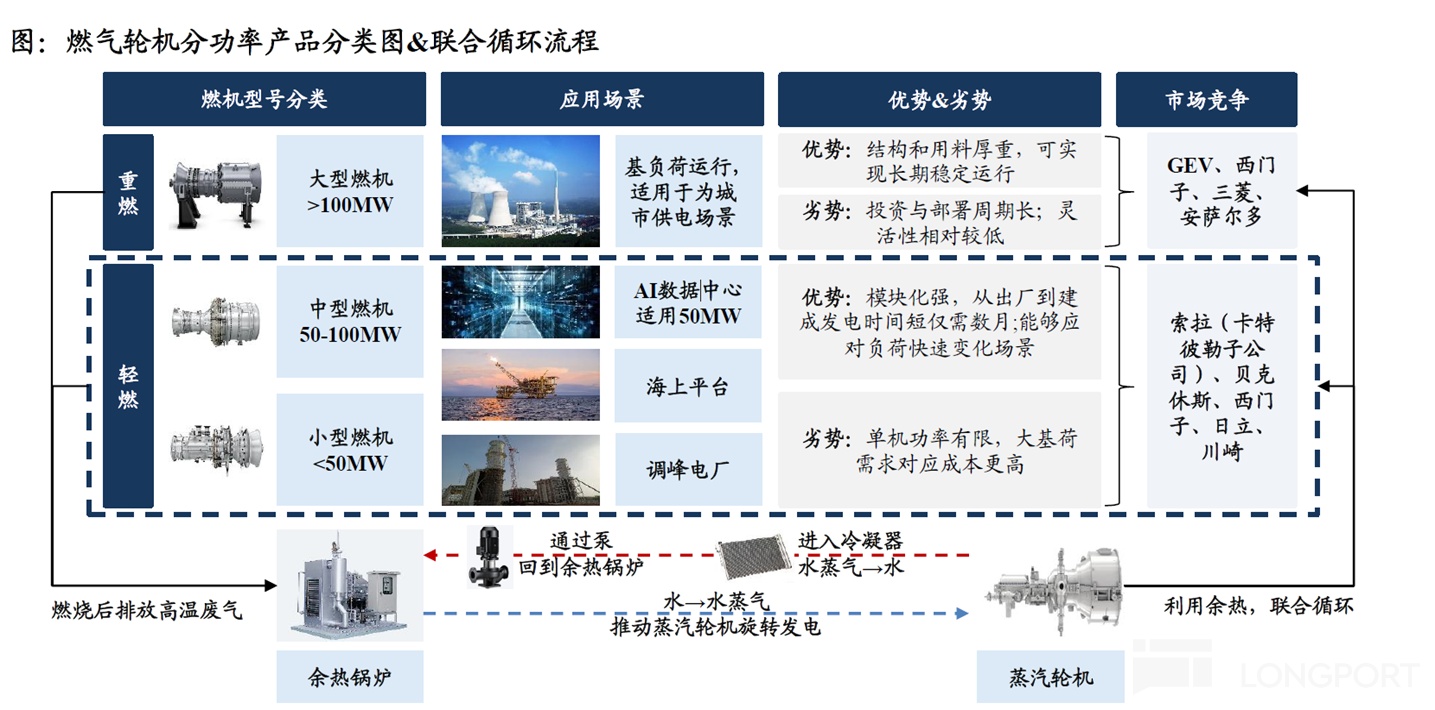

Downstream uses span power generation, industrial drives and marine propulsion, with power generation commanding ~64% of demand. By power class, tech route and application, the industry clusters into three camps:

① Heavy‑duty GTs (>100MW): the backbone of large baseload and grids They deliver extreme scale economics and top‑tier combined‑cycle efficiency (64%+), achieving the lowest LCOE. They dominate large grid‑connected generation as city/grid baseload and are the preferred choice for hyperscale data centers thanks to superior efficiency and economics.

② Medium/industrial GTs (50–100MW): flexible power and industrial drives They balance output, efficiency and flexibility, spanning traditional industrial GTs and some high‑power aero‑derivatives. Use cases include CHP, large industrial captive plants, oilfield power and pipeline compression.

Given long heavy‑duty lead times, some hyperscale DCs now parallel multiple medium GTs as a bridge, balancing scale and time. Examples include Siemens SGT‑800 and GE LM series.

③ Light/aero‑derivative GTs (<50MW): distributed builds and ultra‑fast response Derived from aircraft engines, they offer modularity, second‑level start/stop and 12–18 month delivery. Traditionally used on offshore rigs, small remote plants and mechanical drives, their growth engine is now AIDC microgrids and distributed power.

With fast siting, elastic expansion and high reliability, light aero‑derivatives are Big Tech’s go‑to 'power‑first' solution when grid constraints bite. They enable compute to lead deployment.

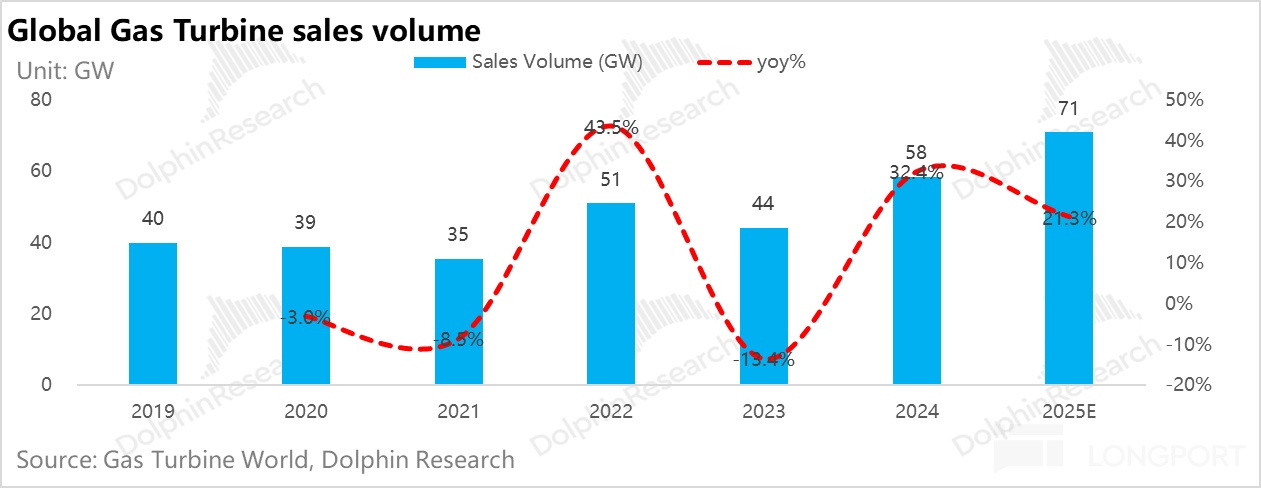

AIDC is catalyzing a new upcycle in gas turbines

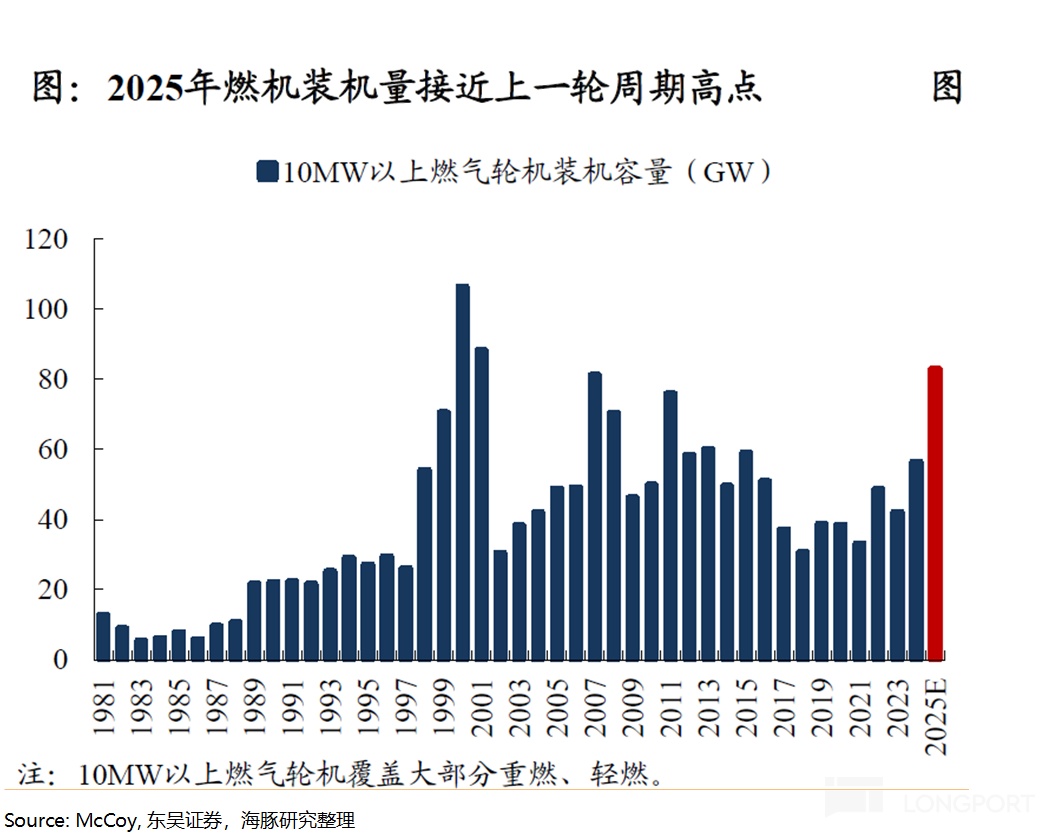

Installed capacity is accelerating: Global annual GT additions rose from 40GW (2019) to 58.4GW (2024), an 8% CAGR. Driven by compute demand, 2025 additions are projected at 70.84GW (+21% YoY), a steep upshift in industry momentum.

AI echoes the internet cycle: 2025 additions are approaching the last cycle’s peak. Back in 2001, the GT boom rode 'internet‑driven' power demand, later cooled by gas prices and overbuild. History rhymes as AIDC‑led demand now picks up the baton and opens a new supercycle.

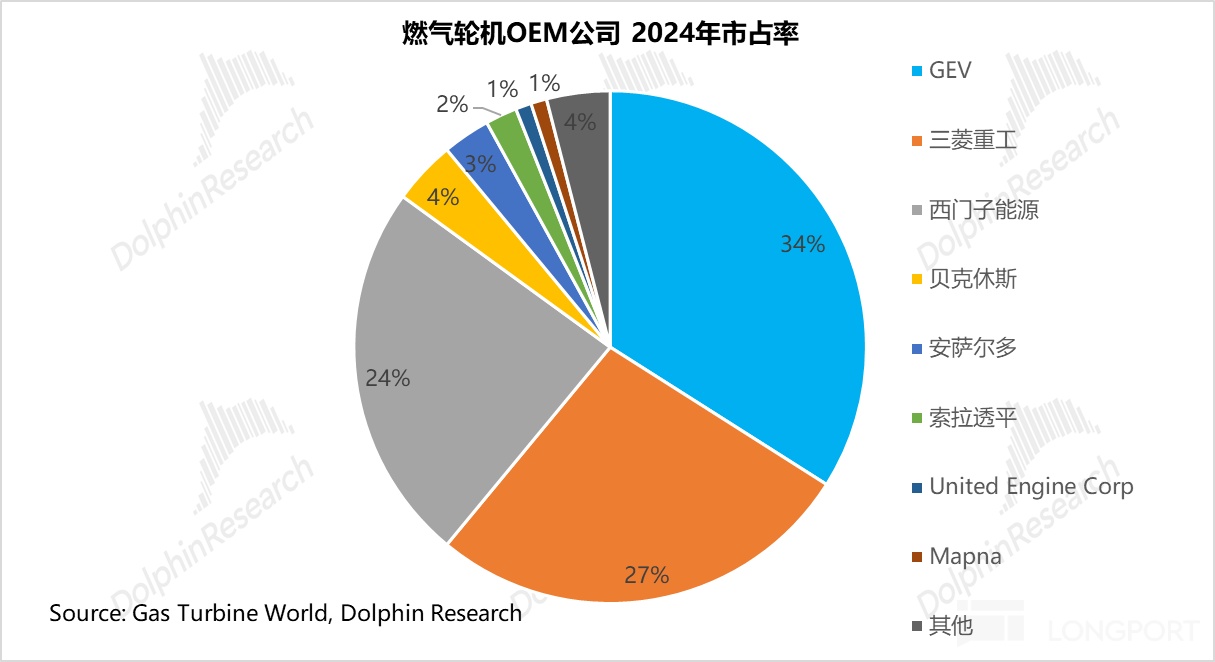

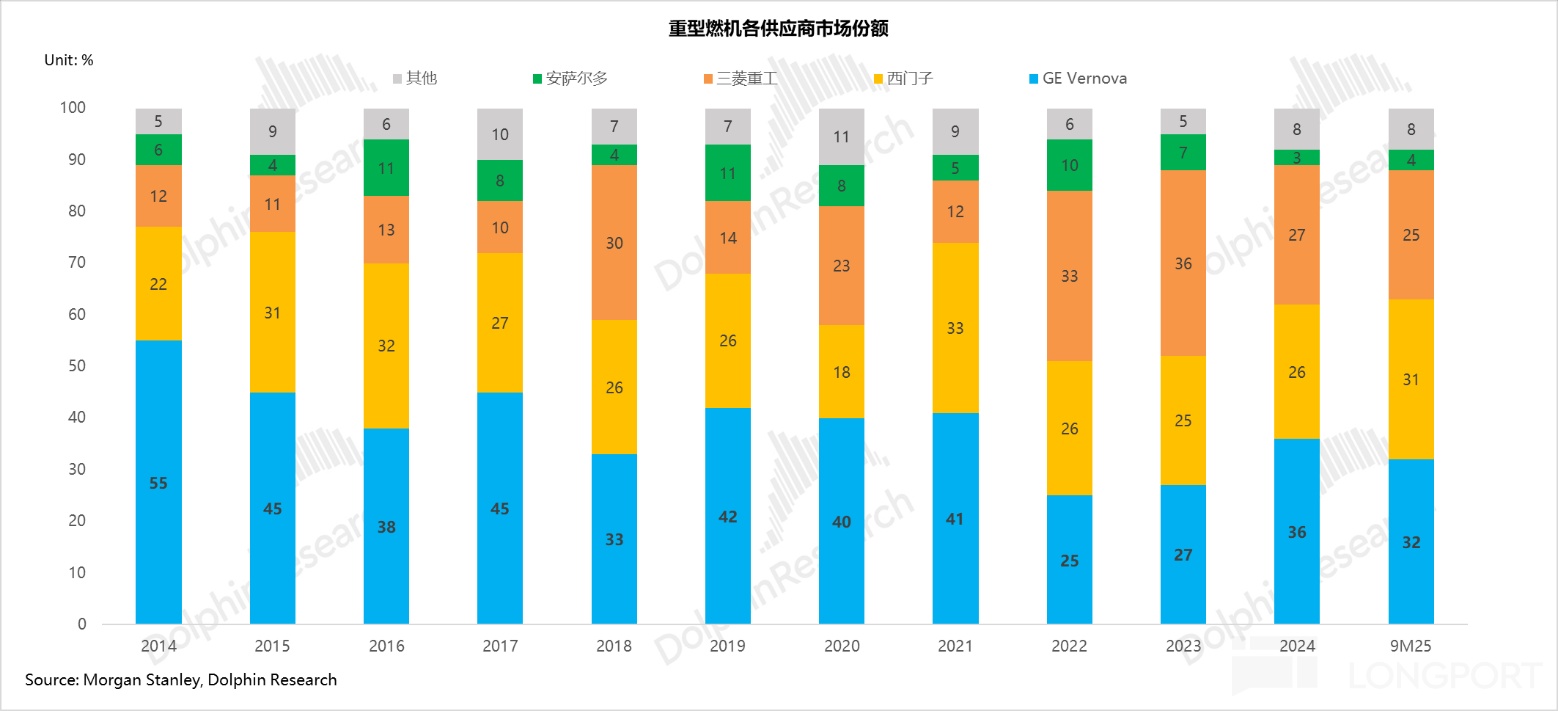

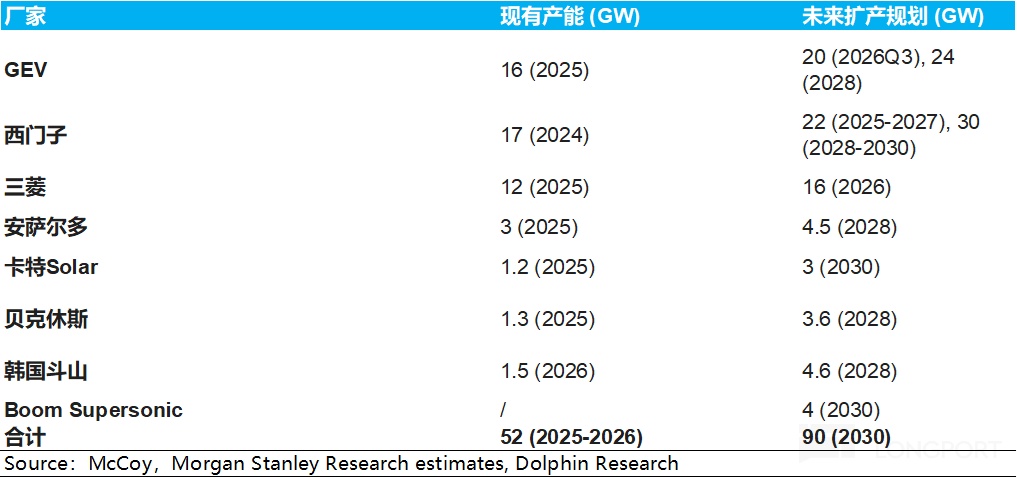

Competitive landscape: a stable triopoly Heavy‑duty GTs are an entrenched oligopoly. In 2024, GE Vernova (GEV), Siemens Energy and Mitsubishi Heavy Industries captured ~85% of global orders and ~90% share in heavy‑duty.

This stability reflects 'high‑tech, high‑capex, high‑ecosystem‑barrier' dynamics—why GTs are called 'the crown jewel of equipment manufacturing'. Moats span technology, capital scale, supply chain and service ecosystems.

① Tech barriers: peak systems engineering under extreme conditions GTs must run reliably for tens of thousands of hours at >1,400°C (above nickel‑alloy melting points), high pressure and high RPM. This demands:

Materials and processes at the limit: turbine blades endure centrifugal forces thousands of times their own weight, relying on single‑crystal superalloys, precision casting, complex air‑cooling channels and TBCs developed over decades; only a handful like PCC and Howmet can mass produce. Cross‑disciplinary systems engineering: aero‑thermo‑structural‑controls tightly coupled, with 10–15 year R&D and multi‑bn costs. Data‑driven control moats: millisecond combustion control algorithms built on proprietary decades‑long operating datasets.

② Capital and scale barriers: sunk costs and scale economics High capex thresholds: full‑chain capacity from melting to casting to full‑engine test requires tens of bn RMB in fixed assets; multi‑bn dollars of R&D is merely table stakes. Scale gap: incumbents have spread costs over global volumes; new entrants without scale cannot cover fixed costs and get stuck in a 'no scale–no profits–no expansion' loop.

③ Supply chain and certification barriers: trust built over long cycles Concentrated critical supply and slow expansions: key materials (rhenium, hafnium) and parts (blades, disks) are concentrated; ~70% of turbine blade capacity is controlled by PCC and Howmet, expanding cautiously and bottlenecking the chain. Long, stringent validation: the turbine is the plant’s heart with unit prices in the tens/hundreds of millions; utilities require multi‑year, tens‑of‑thousands‑hour field runs for new suppliers, making switch‑costs prohibitive.

④ Ecosystem and service barriers: aftermarket lock‑in and high switching costs Engine + LTSA model: initial sale is just the start; 20–30 years of maintenance, spares and upgrades (LTSA) are the profit core, with OEMs pre‑locking value via long‑term service deals. High switching costs: swapping OEMs entails technical risk, system re‑work and retraining, deeply binding operators to current ecosystems.

In today’s high‑cycle, the big three—GEV, Siemens Energy, MHI—show three common patterns from 'demand surge to supply bottleneck', validating the full‑chain upcycle:

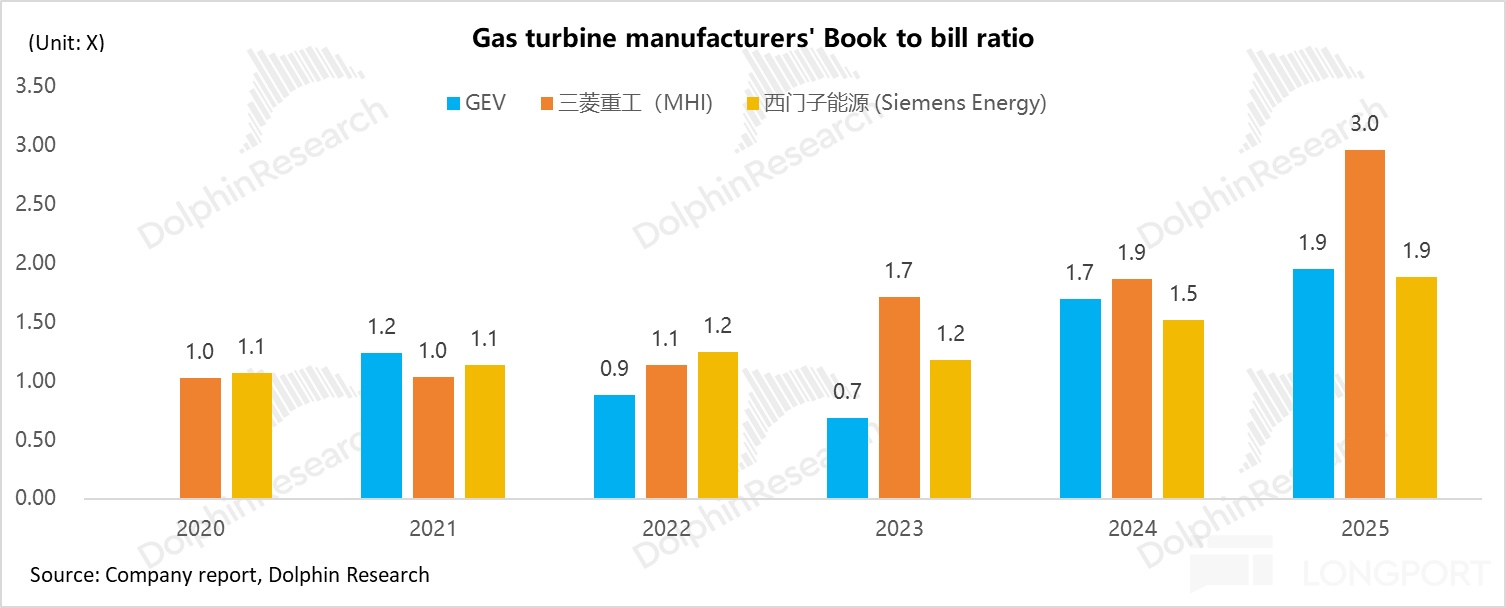

a. Explosive order intake; book‑to‑bill elevated Book‑to‑bill = new orders / revenue; a ratio >1 signals strong demand and expansion. Since 2024, all three hit multi‑year or record order highs; in FY25, book‑to‑bill is ~2 for Siemens Energy, GEV and MHI, with Mitsubishi near 3, driving rapid backlog build.

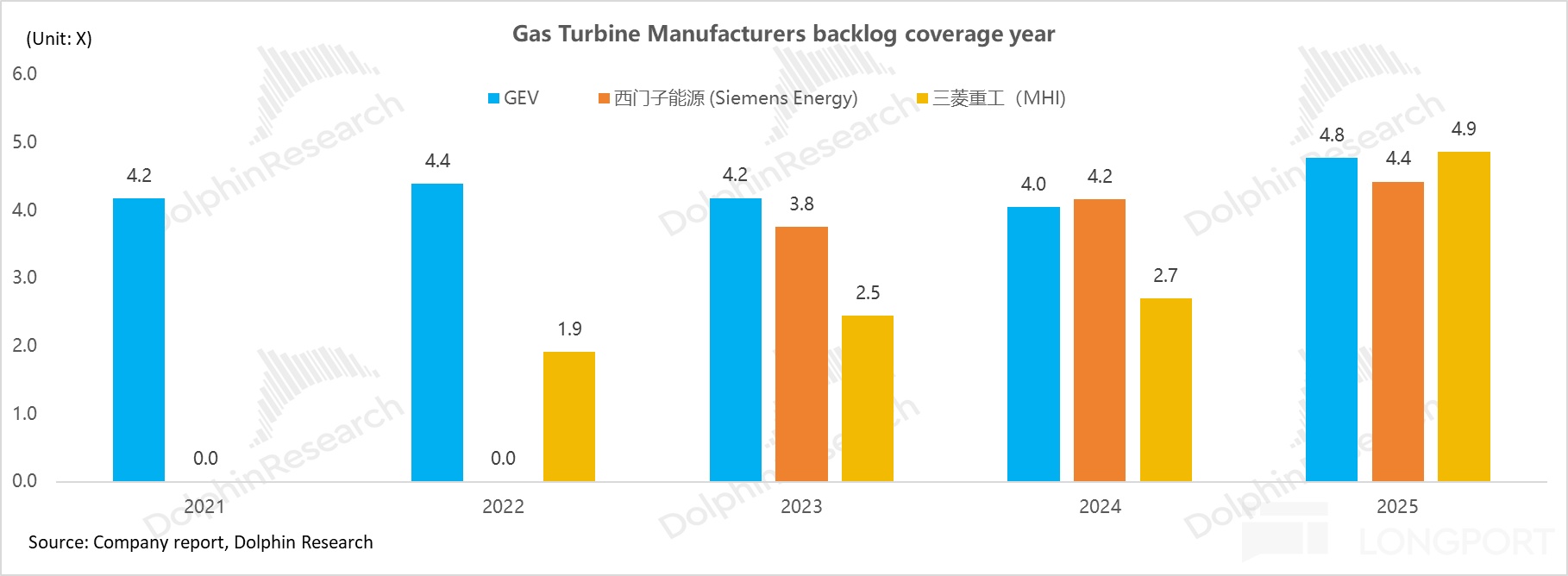

b. Long visibility; backlog coverage keeps rising Backlog coverage = ending backlog / annual revenue, signaling revenue certainty and capacity tightness. With orders outpacing deliveries, backlogs hit records; by end‑2025/early‑2026, coverage extends to 4.5–5.0+ years, with slots filled into 2029–2030, underpinning high certainty for the next 4–5 years.

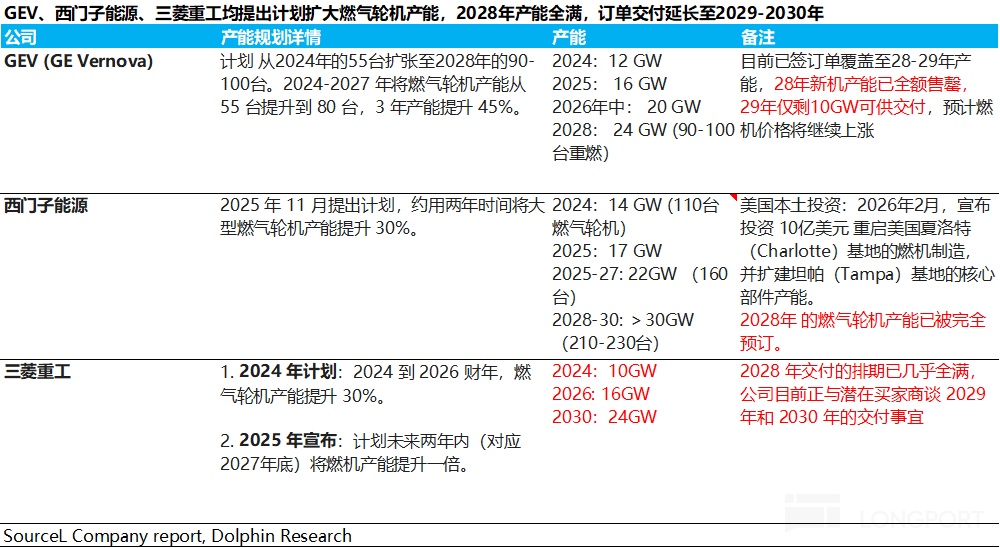

c. Aggressive expansion, but bottlenecks persist To meet demand, OEMs unveiled bold capacity plans (GEV to 24GW by 2028; Siemens 30GW+; MHI to double in two years). Even so, 2028 capacity is largely spoken for by existing orders; real ramps are constrained by upstream critical parts, especially turbine blades.

With blade and precision casting capacity concentrated in a duopoly (PCC, Howmet) and expansions cautious and slow, OEM plans face execution risk, tightening supply further. This keeps the entire chain constrained.

With heavy‑duty GTs 'one‑unit‑hard‑to‑get' and compute racing ahead, how will the giants break the bottleneck? In the next piece, Dolphin Research will dive into substitutes under extreme turbine scarcity—stay tuned. <End>

The copyright of this article belongs to the original author/organization.

The views expressed herein are solely those of the author and do not reflect the stance of the platform. The content is intended for investment reference purposes only and shall not be considered as investment advice. Please contact us if you have any questions or suggestions regarding the content services provided by the platform.