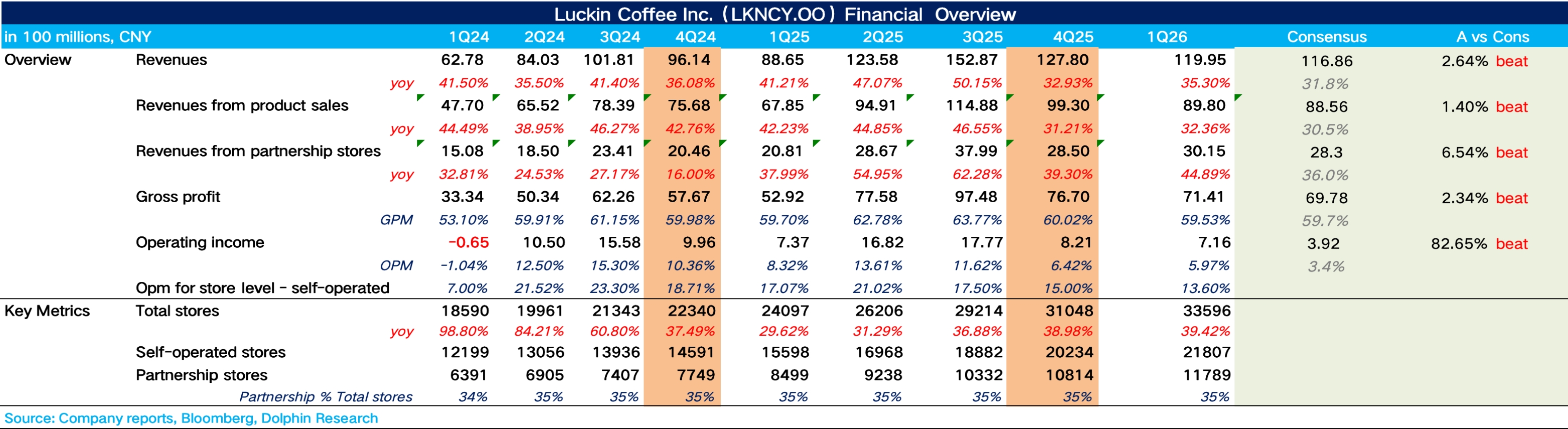

Luckin Coffee 1Q26 First Take: Despite rapid store adds, revenue held up well and slightly beat. The drag remains the old issue: a higher delivery mix kept pushing up fulfillment costs, delaying margin release.

1) Q1 revenue grew 35.3%. On SSSG, same-store sales were roughly flat YoY and decelerated slightly vs. Q4. Dolphin Research believes reduced delivery subsidies led to a modest dip in same-store cup volume.

2) Store expansion remained aggressive, with 2,548 net new stores in Q1, including 17 overseas (Singapore 1, Malaysia 13, U.S. 3). The expansion pace hit a Q1 record. Penetration into lower-tier markets accelerated, reaffirming management's 'share before profit' strategy.

3) Although global coffee bean prices stayed elevated, Luckin partially hedged input pressure via origin direct sourcing and long-term procurement agreements. A higher mix of non-coffee beverages also diluted bean-cost exposure. As a result, GPM was flat YoY.

By expense line, delivery remained the biggest drag, up 48% YoY, with its sales ratio jumping from 7.8% to 10.9%. While lower than 25Q4's 12.8%, it is still well above the pre-delivery-war norm of 7–9%. Non-GAAP OPM came in at 7.5%, down 220bps YoY. $Luckin Coffee(LKNCY.US)

The copyright of this article belongs to the original author/organization.

The views expressed herein are solely those of the author and do not reflect the stance of the platform. The content is intended for investment reference purposes only and shall not be considered as investment advice. Please contact us if you have any questions or suggestions regarding the content services provided by the platform.