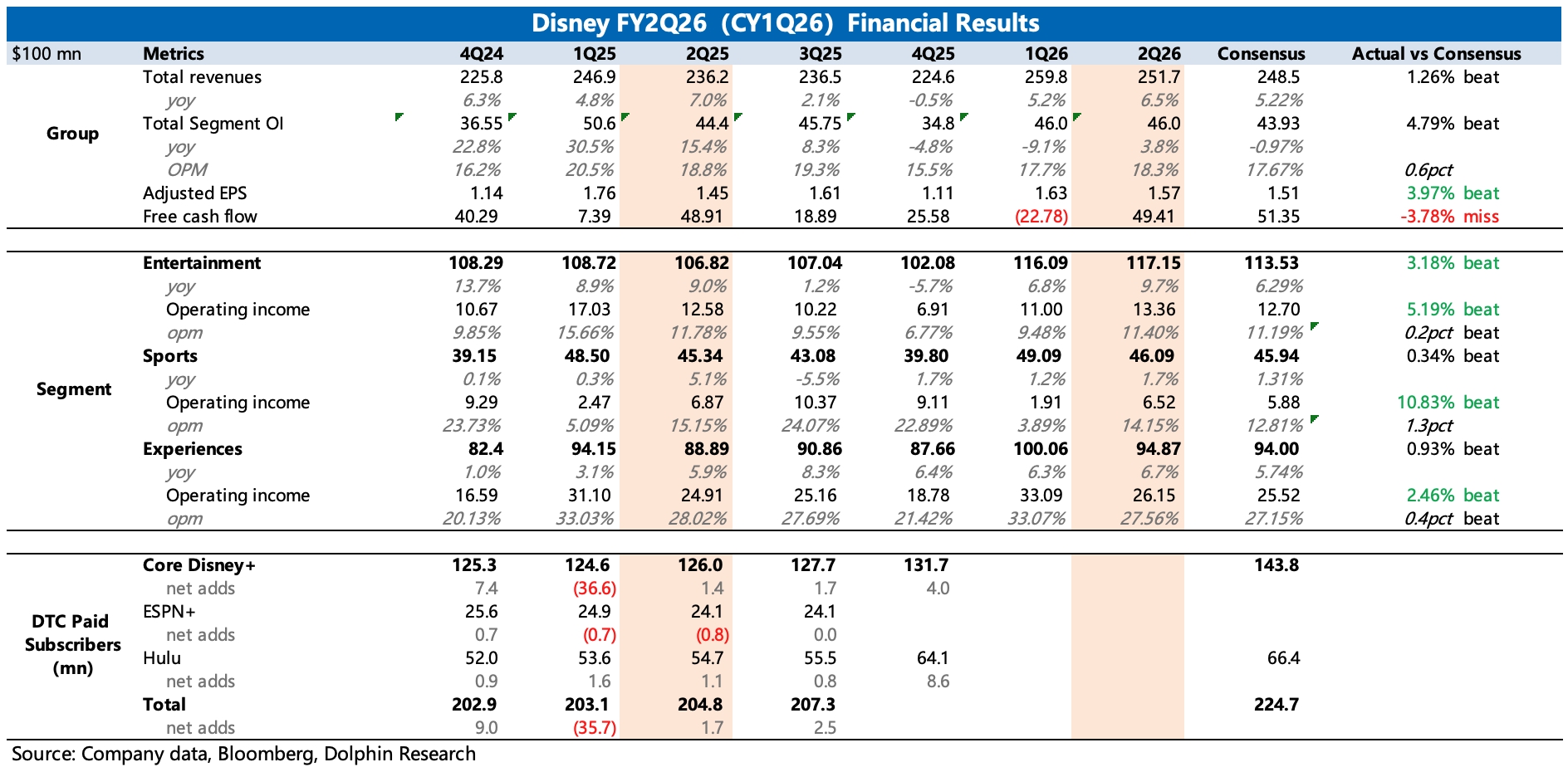

DIS 2Q26 FY First Take: The quarter slightly beat estimates. Management offered solid FY26 guidance and raised buybacks, easing market jitters around macro volatility and the new CEO transition.

1) Guidance beat: 2Q26 aligns with calendar Q1 and faced short-term headwinds from Middle East tensions and higher sports rights costs. Elevated oil prices can dampen travel demand and park revenue, while rights inflation pressured sports profitability.

While Parks and Sports were affected, Disney's resilience delivered a better-than-expected print. Total revenue rose 7%, with a slight QoQ acceleration. OPM was roughly flat YoY and improved 60bps vs. Q1.

Despite macro uncertainty, management guided constructively for Q3 and the full year, with tailwinds from a H2 film slate, new cruise itineraries, and post-integration streaming efficiencies.

1) Q3 segment OP is guided at ~$5.3bn, up 16% YoY, a sharp acceleration vs. 4% in Q2.2) Full-year Adj. EPS growth guidance remains ~12% (vs. ~11% consensus); including the 53rd week, FY26 EPS would be up 16% YoY.

2) Streaming held up well: Q2 Entertainment revenue grew nearly 10%, with momentum accelerating QoQ. SVOD benefited from price increases and the release of premium titles such as 'Zootopia,' driving faster growth.

Meanwhile, OPM improved by 200bps vs. Q1. Streaming margin exceeded 10%, hitting the previously set full-year profitability target, and Disney plans to unify Disney+ and Hulu into a single platform this year to further enhance efficiency.

3) Parks show blue-chip resilience: Experiences revenue rose 7%, holding growth despite a tougher base. U.S. attendance fell 1% YoY amid the drag from Middle East tensions via higher oil prices, but expanded attractions and new cruise routes underpinned resilience.

4) Sports still in integration: Q2 Sports revenue was flattish, with margin down 100bps YoY. As one of the three strategic pillars highlighted by the new CEO, ESPN has been reshaping since H2 last year.

Initiatives include a flagship new platform and a cross-shareholding arrangement with the NFL. Disney also signed new content procurement/carriage agreements with WWE, MLB, and other providers.

Rights renewals for college football and the NBA came at higher costs, and WWE represents incremental content, weighing on near-term profitability. The company expects Q3 segment OP to decline 14% YoY.

5) Buyback raised: The full-year buyback budget was lifted to $8bn from $7bn. H1 repurchases totaled $5.5bn ($3.5bn in Q2), and dividends were $1.3bn.

On an annualized basis, buybacks plus dividends of ~$10.6bn imply a ~6% shareholder yield on a ~$178bn market cap. $Disney(DIS.US)

The copyright of this article belongs to the original author/organization.

The views expressed herein are solely those of the author and do not reflect the stance of the platform. The content is intended for investment reference purposes only and shall not be considered as investment advice. Please contact us if you have any questions or suggestions regarding the content services provided by the platform.