Goldman Sachs & FactSet: U.S. Stock Earnings Expectations Accelerating Upward Revisions

Recent data from Goldman Sachs and FactSet provides a crucial signal: the driving force behind U.S. stock gains is gradually shifting from pure valuation expansion to earnings expectation revisions.

In a high-valuation environment, the market fears most the "lack of fundamental support." If earnings expectations continue to be revised upward, then even with high index valuations, EPS growth on the denominator side can partially absorb valuation pressure.

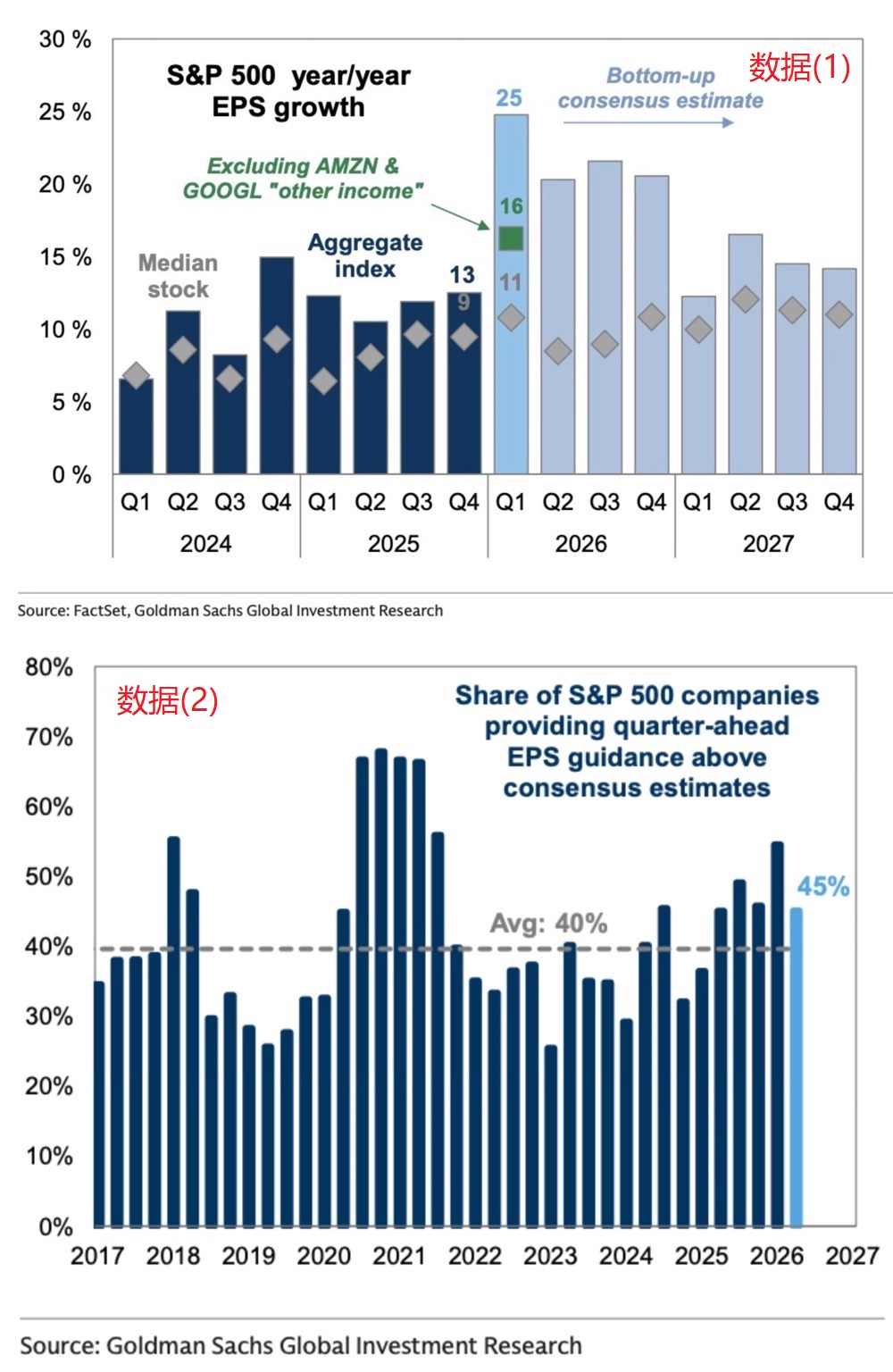

① Four sets of data on earnings expectations for major U.S. stock indices

· The year-over-year EPS growth rate for the S&P 500 mostly remains in the mid-to-high single-digit to low double-digit range for 2024 and 2025. Entering 2026, the market consensus expectation has significantly increased.

· In Q1 2026, the expected year-over-year EPS growth rate for the S&P 500 as a whole reaches about 25%. Even after excluding Amazon and Google's "other income," there is still about 16% growth.

The earnings improvement does not rely entirely on a single accounting disturbance, nor is it just the short-term contribution of a few giants.

② One detail cannot be ignored

Data (1) The "median company" is significantly lower than the overall index. The current earnings recovery of the S&P 500 still exhibits a clear concentration effect at the top, and the internal structure is not balanced.

Data (2) further verifies positive signals from the corporate side.

The proportion of S&P 500 companies providing next-quarter EPS guidance that is higher than the market consensus expectation has reached 45%, above the long-term average of 40%. The earnings upward revision is not just analysts unilaterally raising their models.

· However, 45% is not an extreme high:

During the 2020-2021 recovery phase, this proportion approached or even exceeded 60%. The current situation is more like a moderately strong earnings recovery.

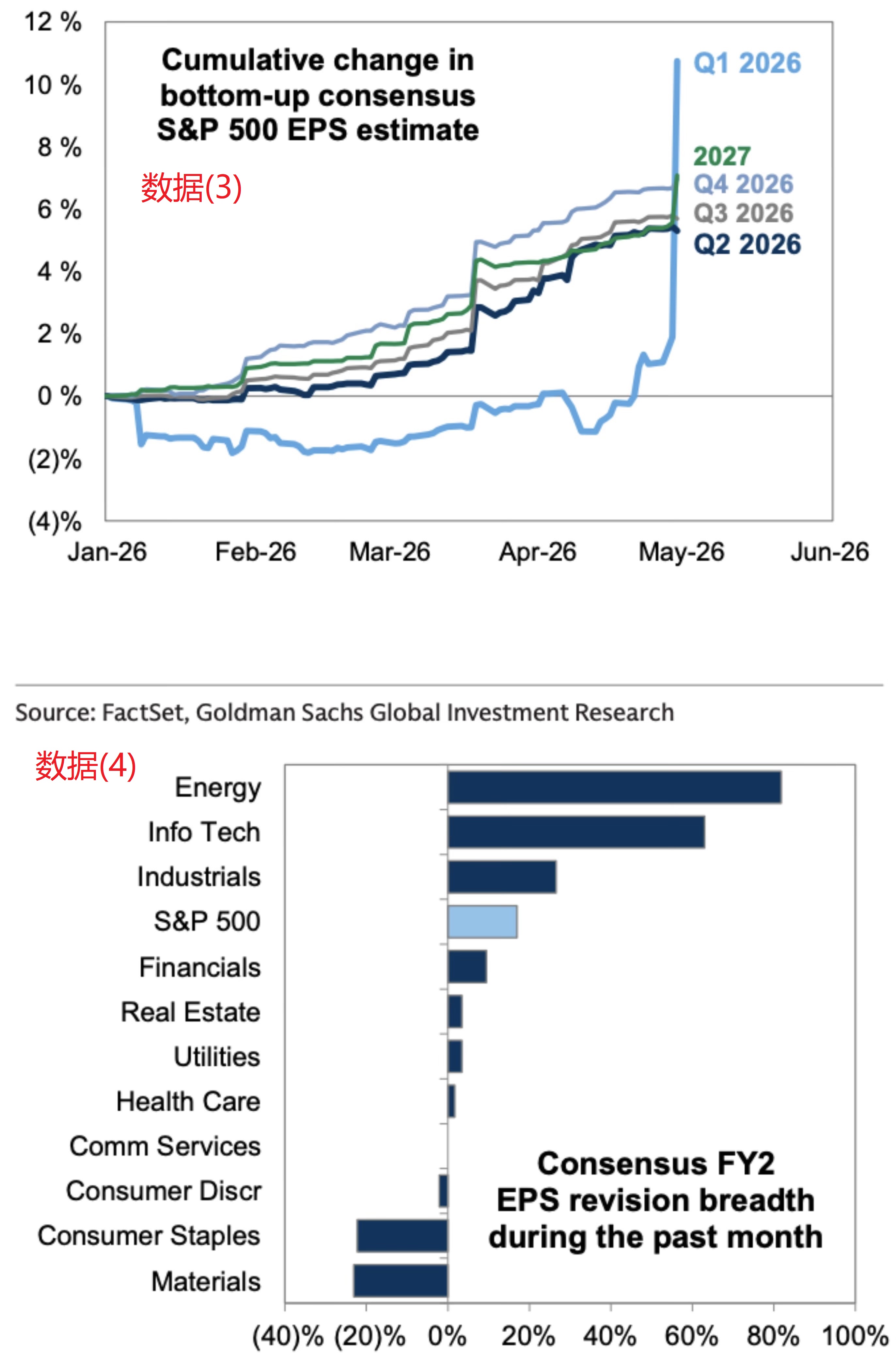

③ The market's continuous upward revisions of future EPS

According to data (3), from early 2026 to May, the S&P 500 EPS expectations for Q2, Q3, Q4 2026, and 2027 have generally been revised upward by about 5%-7%, while Q1 2026 even saw an almost vertical upward revision.

· The underlying signal is very clear:

The market is not trading on a single quarter's earnings beat, but is repricing the earnings path for the next several quarters. If this upward revision trend continues, the U.S. stock rally is entering a more solid phase of "earnings realization trading."

④ The sources of earnings upward revisions are not even

What's truly worth paying attention to is data (4):

Over the past month, the industries with the strongest FY2 EPS revision breadth have mainly been concentrated in Energy, Information Technology, and Industrials. Energy has the highest revision breadth, Information Technology is clearly leading the broader market, and Industrials also maintain positive improvement.

This indicates that the current U.S. economy is not in a broad-based expansion. This round of earnings revisions is more like a structural rally driven by AI capital expenditure, energy sector strength, and industrial order recovery.

Therefore, judging the U.S. stock market cannot rely solely on the index level.

The real risk lies in the fact that market expectations have already started to rise. The most important variable for the current market has shifted from "will interest rates be cut" to "can earnings continue to be revised upward."

⑤ Focus on three key things:

· Will S&P 500 EPS expectations continue to be revised upward;

· Will corporate earnings guidance remain strong;

· Can the earnings recovery spread from Technology and Energy to more sectors.

As long as these three points do not show a significant reversal, the high valuation of U.S. stocks still has some support.

Data source: Goldman Sachs, FactSet

$SPDR S&P 500(SPY.US) $Invesco QQQ Trust(QQQ.US)

The copyright of this article belongs to the original author/organization.

The views expressed herein are solely those of the author and do not reflect the stance of the platform. The content is intended for investment reference purposes only and shall not be considered as investment advice. Please contact us if you have any questions or suggestions regarding the content services provided by the platform.