$Opendoor Tech(OPEN.US)

Opendoor 26Q1 Earnings Report: Revenue Plunges 38%, Gross Margin at 10%

Key Takeaways:

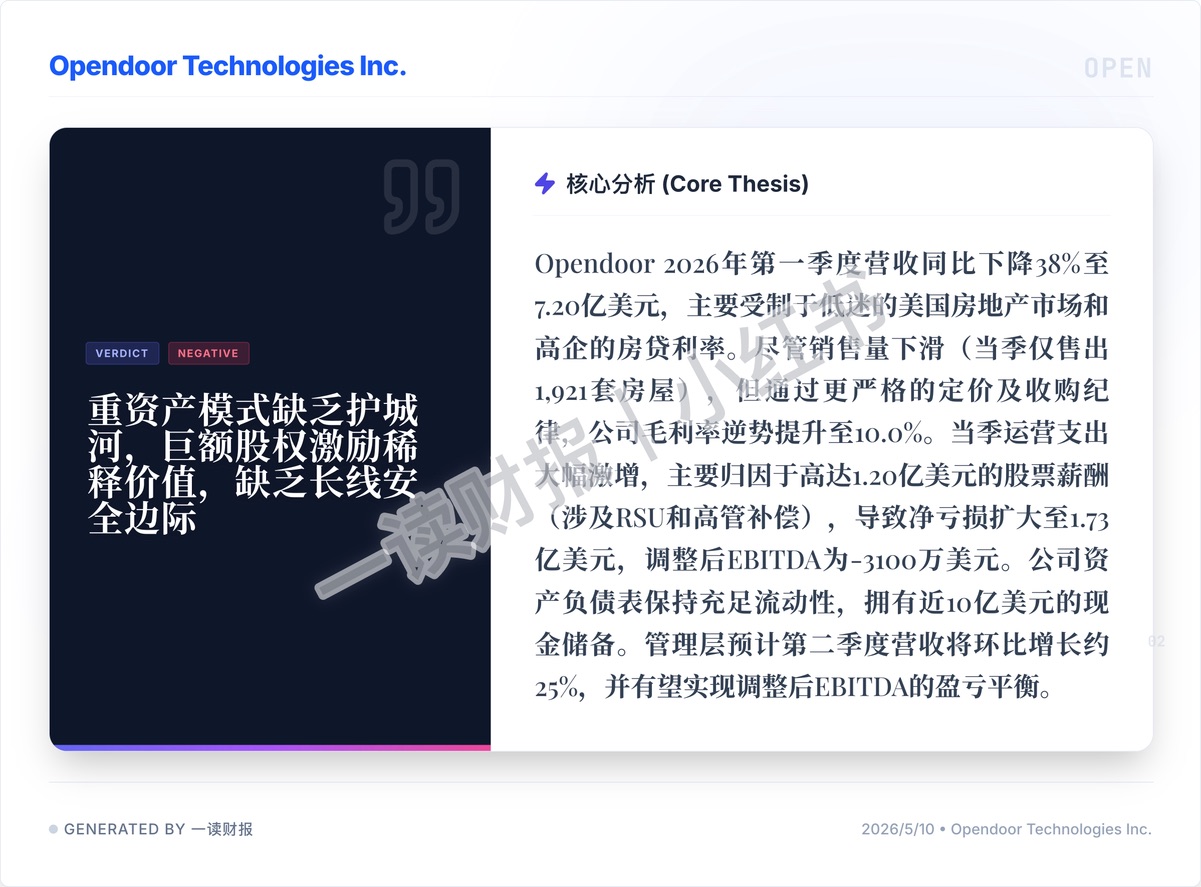

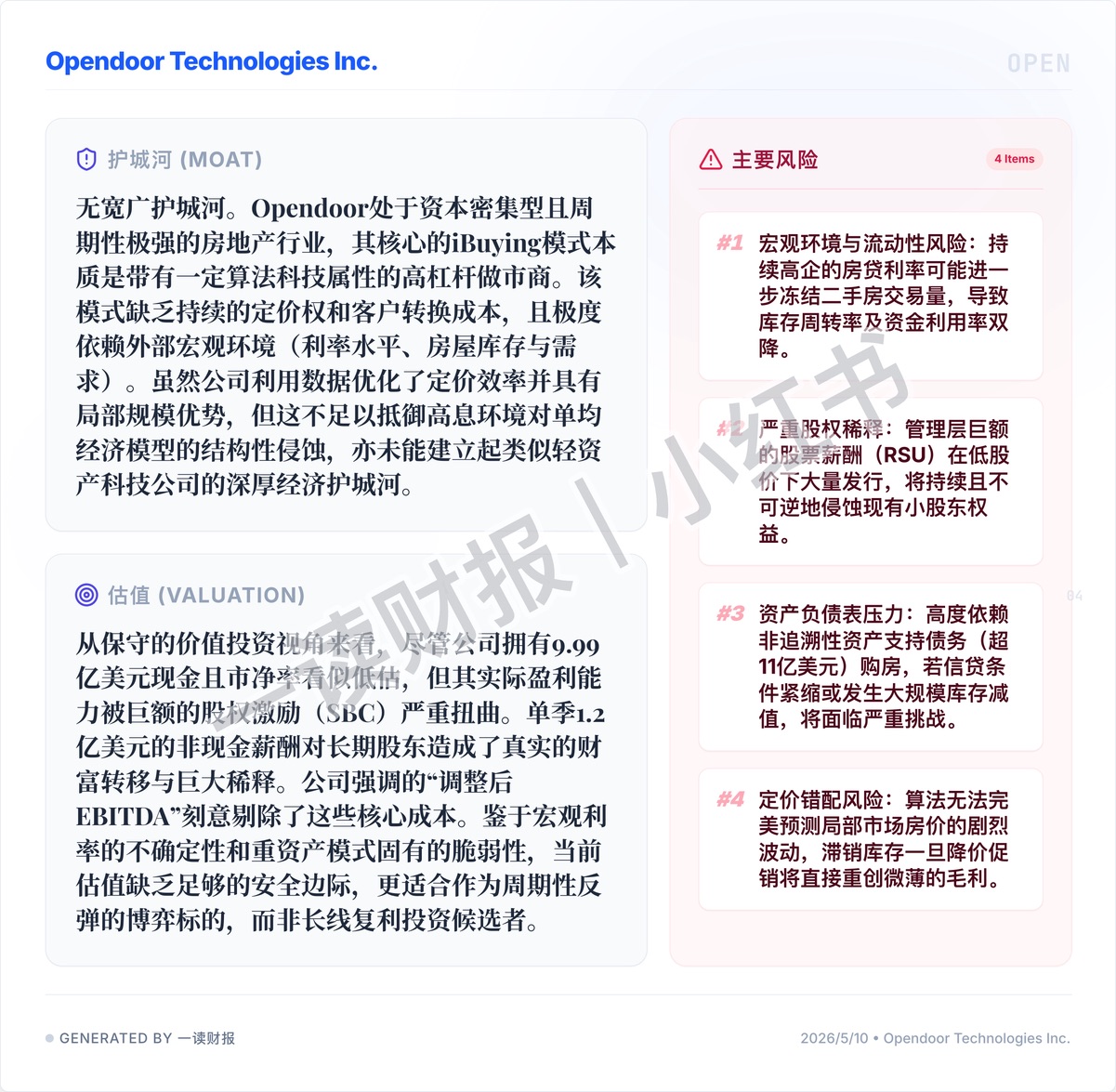

1. Structural Flaws of the iBuying Business Model: Opendoor is essentially a highly leveraged "secondary housing market maker" with algorithmic attributes. During a real estate downturn or high-interest-rate cycle, it is forced to bear the massive holding costs and book value impairment of heavy-asset inventory. In an upcycle, the thin buy-sell spread it earns is easily consumed by high operating and customer acquisition costs. Algorithms do not confer pricing power. As long as long-term mortgage rates remain above 5%, this model will be mired in "thin profits or structural losses."

2. SBC "Bleeding" and Real Wealth Transfer: In a quarter of extreme headwinds with only 1,921 homes sold and revenue plunging 38% year-over-year to $720 million, quarterly operating expenses surged significantly. A whopping $120 million in stock-based compensation shifted the high compensation burden to shareholders. The "Adjusted EBITDA" emphasized by management deliberately excludes these core costs, a severe distortion of true profitability.

3. Heavy Debt Burden and Macroeconomic Fragility: Despite having cash on the books, its balance sheet heavily relies on recourse asset-backed debt (over $1.1 billion) to purchase homes. Against the backdrop of persistently high mortgage rates further freezing secondary home transaction volume, once credit conditions tighten or large-scale inventory impairment occurs, the company faces a very high risk of a funding chain break.

4. Clearing Historical Inventory Baggage and the Difficult Repair of Gross Margin: The most difficult destocking phase may be over, with the proportion of "toxic inventory" held for over 120 days significantly reduced to a healthy level of 10%. Through strict pricing and acquisition discipline, the company's gross margin improved against the trend to 10.0% in the quarter. Management expects Q2 revenue to grow approximately 25% sequentially (to $900 million) and anticipates achieving breakeven Adjusted EBITDA.

5. The Narrative of a Rate-Cut Cycle and the Nearly $1 Billion Cash Cushion: The company currently holds $999 million in cash reserves, providing life-sustaining liquidity in the current real estate winter. Additionally, with the potential start of a Fed rate-cut cycle, the severely suppressed home-buying demand, once released, will drive a recovery in transaction volume. At that point, Opendoor, with its nationwide inventory footprint, could leverage significant operating leverage during the industry recovery, leading to a dual rebound in performance and valuation.

Opendoor (OPEN) delivered a dismal report card that laid bare "agency risk." It proved the impotence of real estate tech against the cycle with plunging revenue and massive losses. At its core, it remains a company lacking a true moat.

Source: Yidu Caibao, providing original earnings report downloads

#USStockEarnings #ValueInvesting #Opendoor #OPEN #RealEstateTech #BusinessModel #FundamentalAnalysis #YiduCaibao

The copyright of this article belongs to the original author/organization.

The views expressed herein are solely those of the author and do not reflect the stance of the platform. The content is intended for investment reference purposes only and shall not be considered as investment advice. Please contact us if you have any questions or suggestions regarding the content services provided by the platform.