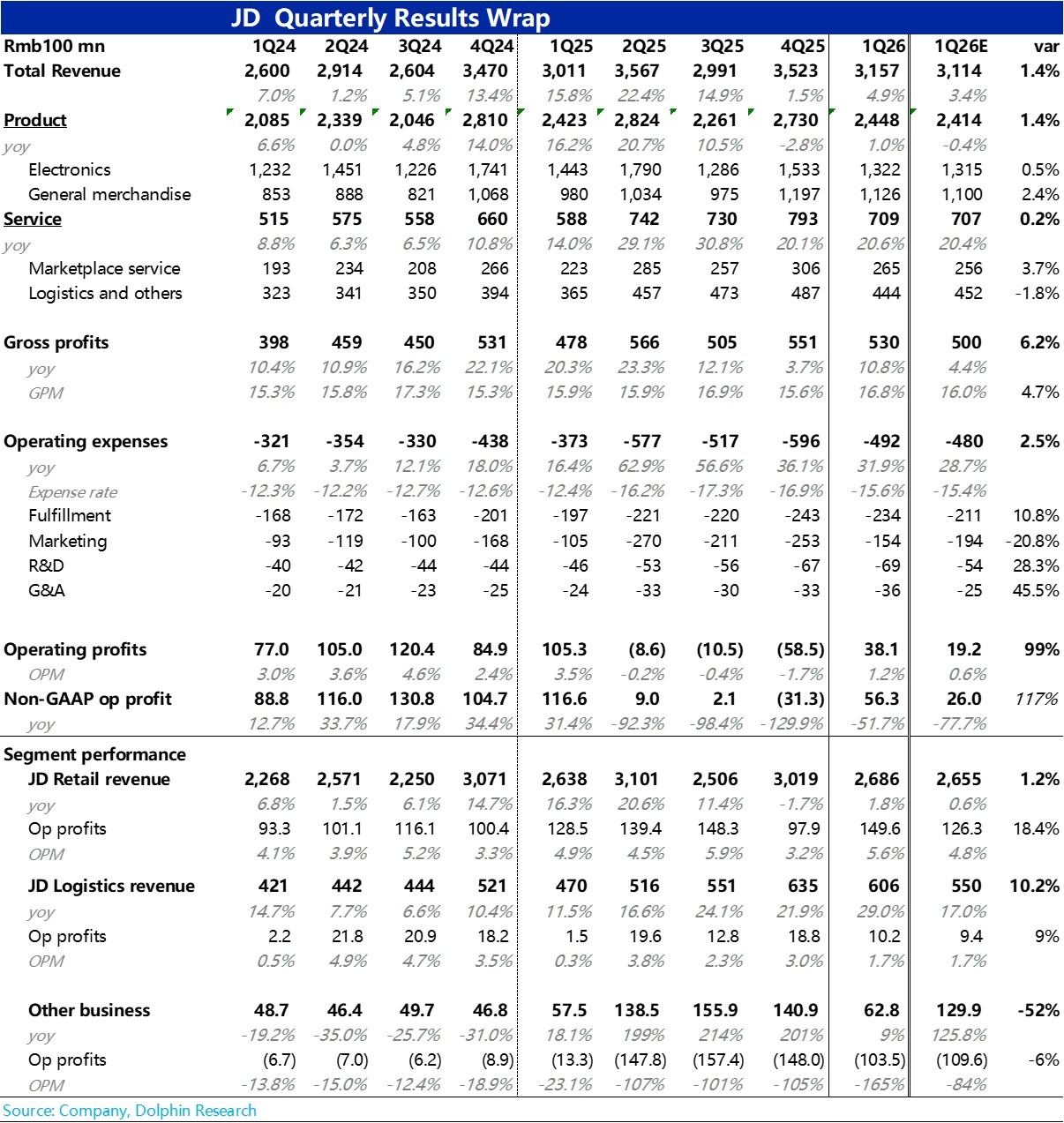

JD 1Q26 First Take: a brief note first, with a fuller review to follow when time permits. Overall, results beat market expectations and align with prior guidance that performance has bottomed and is turning up.At the headline level, revenue growth reaccelerated to ~5%, ahead of the 3.4% consensus. Adj. OP came in at RMB 5.6bn; with a sharp reduction in food-delivery losses, profit improved markedly vs. Q2–Q4 2025, though it was still down by more than half YoY.

By segment, core Mall revenue growth recovered to 1.8%. Within that, appliances and electronics revenue fell nearly 9% YoY as state subsidies faded, while general merchandise and 3P services posted solid growth, driving a slightly better-than-expected recovery for the Mall segment.Mall profit materially beat as well, returning to growth at +16.5% YoY vs. Bloomberg cons. expecting a decline. Despite opex rising ~11% YoY, the key driver was a significant GPM expansion of 180bps.Beyond mix shifts, JD likely secured better supplier terms, partially offsetting the drag from lower state subsidies.

Other businesses, including food delivery, posted a loss of ~RMB 10.4bn this quarter, narrowing by ~RMB 4.5bn QoQ. This clearly reflects sharply lower losses after JD largely exited head-on competition in food delivery.

With Mall profitability beating, food delivery losses narrowing as expected, and logistics performing well, JD delivered a solid quarter. That said, the rebound had been well telegraphed, so the surprise vs. expectations is limited.$JD.com(JD.US) $JD-SW(09618.HK)

The copyright of this article belongs to the original author/organization.

The views expressed herein are solely those of the author and do not reflect the stance of the platform. The content is intended for investment reference purposes only and shall not be considered as investment advice. Please contact us if you have any questions or suggestions regarding the content services provided by the platform.