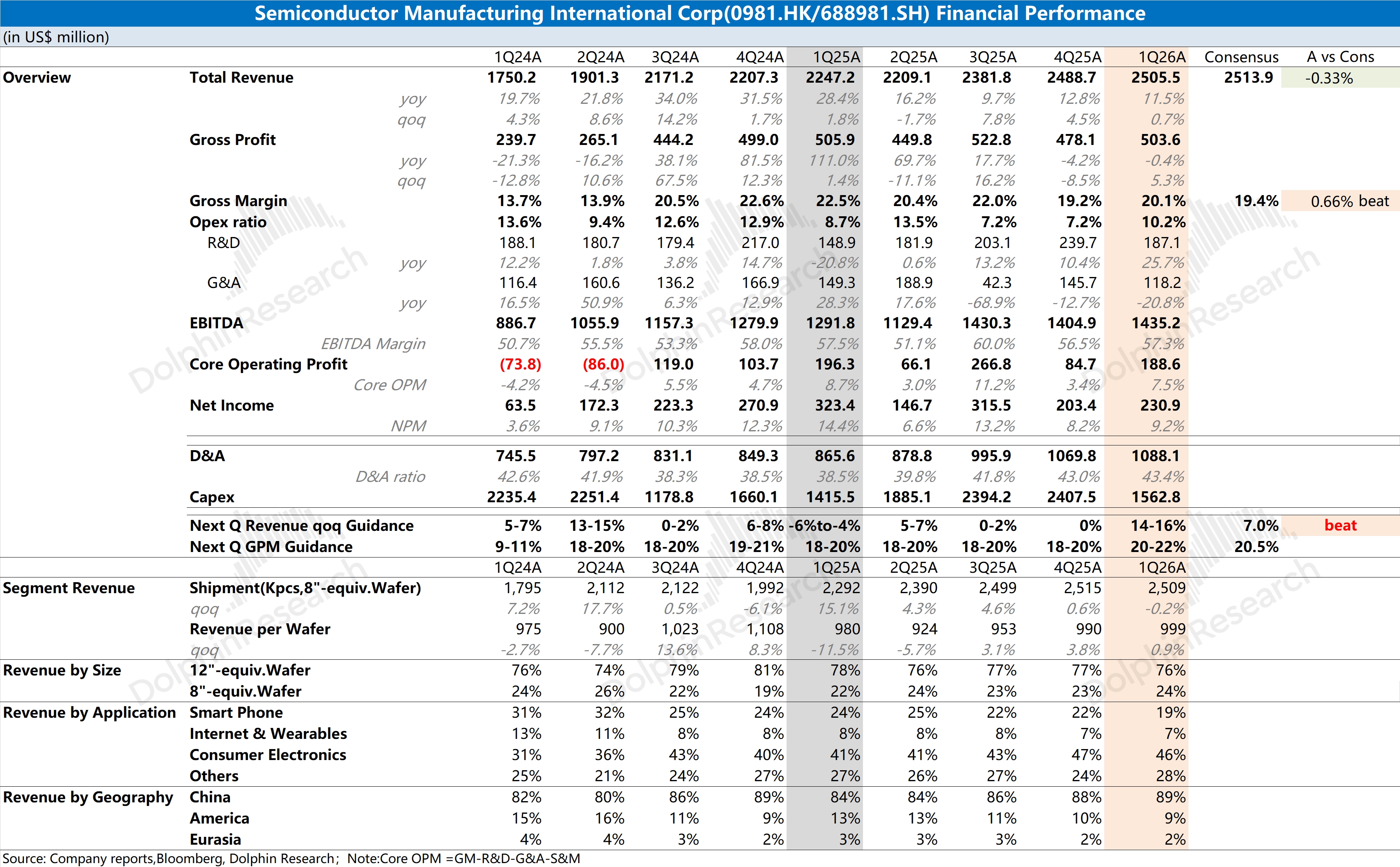

SMIC 1Q26 First Take: Results were solid. Revenue was roughly in line with the Street, while GPM beat meaningfully.

On margin drivers, ASP rose by approx. $9/wafer QoQ, while unit cost fell by $2/wafer, lifting GPM this quarter. Recent demand recovery in power-related products is driving price increases at mature nodes, which should support further margin expansion.

Versus the print, next quarter guidance matters more, and management expects it to be 'quite good'.

The company guides revenue up 14%–16% QoQ, well ahead of the Street at +7%. GPM is guided to 20%–22%, with the midpoint above the Street's 20.5%.

For next quarter, Dolphin Research sees both volume and price lifting results. Demand recovery at mature nodes should support pricing, while ongoing capacity additions and higher utilization should also help.

While margins and earnings remain at a relatively low base, guidance suggests the company is turning up from the trough.

Among second-tier foundries, SMIC still carries expectations for China's push into advanced nodes. That has been the key reason it enjoyed a valuation premium in the past.

However, with recent price hikes in some mature-node categories, rallies in UMC and GlobalFoundries have largely erased SMIC (H)'s relative valuation advantage.

SMIC's recent share-price underperformance vs. peers stems from two factors: first, power and other mature-node products account for a relatively small mix; second, the market worries about a MATCH Act-driven escalation of sanctions on immersion DUV. Dolphin Research remains relatively confident in 2H growth. Smartphone demand should bottom in Q2 (per Qualcomm management), and the Ascend 950DT is moving into mass production.

Price increases now seen in some mature-node categories could broaden into an upcycle for the wider semiconductor industry. With demand from Chinese AI customers (e.g., Cambricon), as long as advanced nodes can ship smoothly, valuation upside remains for the company.$SMIC(00981.HK) $SMIC(688981.SH)

The copyright of this article belongs to the original author/organization.

The views expressed herein are solely those of the author and do not reflect the stance of the platform. The content is intended for investment reference purposes only and shall not be considered as investment advice. Please contact us if you have any questions or suggestions regarding the content services provided by the platform.