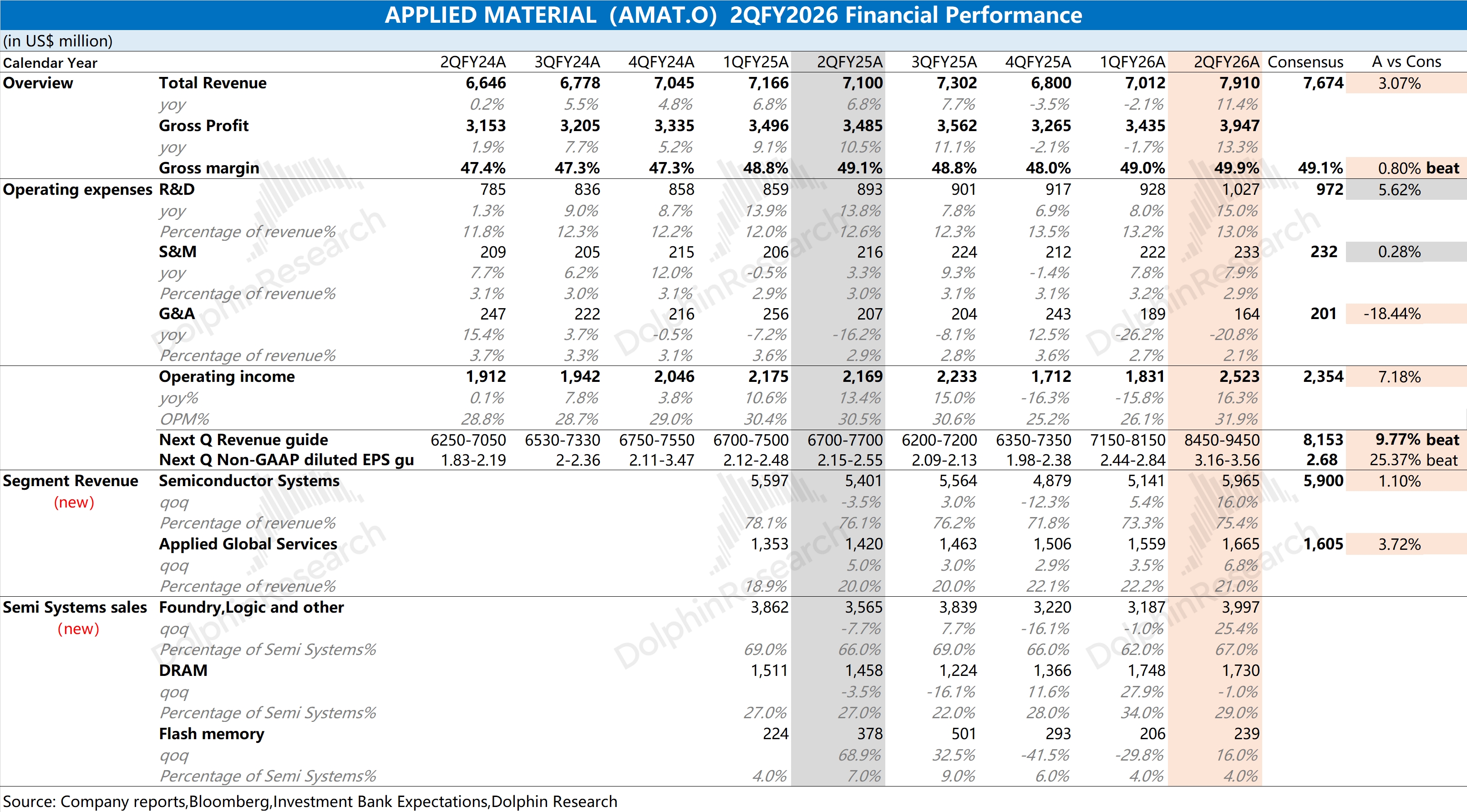

AMAT First Take: Revenue and GPM were solid, both beating estimates, as growth was driven by the AI compute buildout, which lifted demand for advanced logic, DRAM and advanced packaging tools.

Guidance for next quarter looks even stronger than the print. Mgmt guides revenue of $8.45-9.45bn, midpoint +13% QoQ, well above the Street at $8.15bn. EPS is guided at $3.16-3.56, also ahead of the $2.68 consensus.

As downstream customers raise capex, AMAT is set to enter a revenue expansion phase. Demand is particularly strong for tools in advanced logic, memory and advanced packaging.

On the other hand, new product iterations should lift GPM and further improve operating metrics. After the blowout guide, the stock rose as much as 7% after hours.

However, on the subsequent call, mgmt struck a relatively cautious full-year tone. Mgmt expects semi equipment revenue to grow over 30% YoY in CY2026.

Breaking down the next-quarter guide, semi equipment growth is already near ~30% in the upcoming quarter. In other words, with capex still rising, the full-year outlook implies limited acceleration thereafter, which poured cold water on sentiment.

Overall, after a sustained rally, mgmt's conservative full-year stance cooled near-term enthusiasm. Still, upstream semi equipment remains a high-conviction leg in this upcycle. As chip pricing and capacity additions pick up, fundamentals should inflect from a clear bottom for $Applied Materials(AMAT.US).

The copyright of this article belongs to the original author/organization.

The views expressed herein are solely those of the author and do not reflect the stance of the platform. The content is intended for investment reference purposes only and shall not be considered as investment advice. Please contact us if you have any questions or suggestions regarding the content services provided by the platform.