Leapmotor 1Q26 First Take: Overall, the first quarter of FY26 did not carry forward the company's usual operational discipline. The print is concerning.

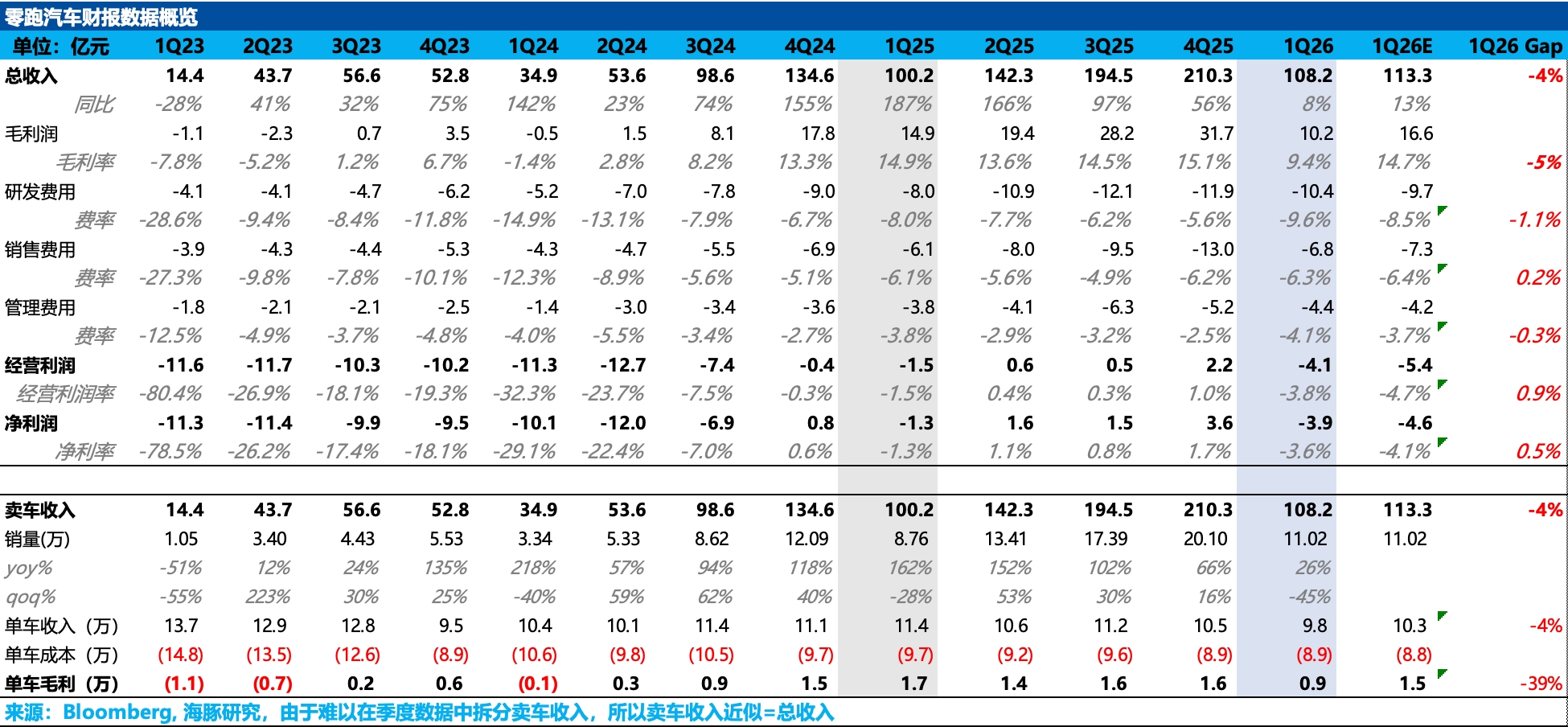

Despite a decent delivery print for an industry off-season and reasonable cost control, both revenue and GP fell short. Revenue was RMB 10.82bn, a slight miss vs. market. GP missed by about 40%, which weighed on sentiment.

On margins, GPM fell 550bps YoY; even stripping out roughly RMB 200mn of GP uplift from strategic partnerships, GPM was still down 390bps YoY. Management added that lower output increased per-unit manufacturing costs.

The market has largely priced in several factors.

1) Management had guided to a sequential decline for Q1 due to seasonality on the Q4 call. This was flagged in advance.

2) Mix shifted down-market as T03 rose from 11% in Q4 to 22% in Q1, while the lower-price A10 started to ramp in Mar, pressuring ASP. This further diluted the model mix.

On opex: selling expenses were RMB 680mn, seasonally softer and broadly in line. R&D was RMB 1.04bn, a slight miss tied to project timing. G&A came in at RMB 440mn vs. the market’s RMB 420mn, essentially in line and largely seasonal.

OP was -RMB 410mn, better than the market’s -RMB 540mn, implying sizable non-recurring items this quarter. More color should come on the call.

a) Management’s explanation for the per-vehicle margin decline. Details will help quantify the impact.

b) Q2 guidance. It will frame the near-term recovery trajectory.

c) Sustainability of the strategic partnership uplift. This affects visibility on GP support. Dolphin Research will publish a follow-up note; stay tuned. $LEAPMOTOR(09863.HK)

The copyright of this article belongs to the original author/organization.

The views expressed herein are solely those of the author and do not reflect the stance of the platform. The content is intended for investment reference purposes only and shall not be considered as investment advice. Please contact us if you have any questions or suggestions regarding the content services provided by the platform.