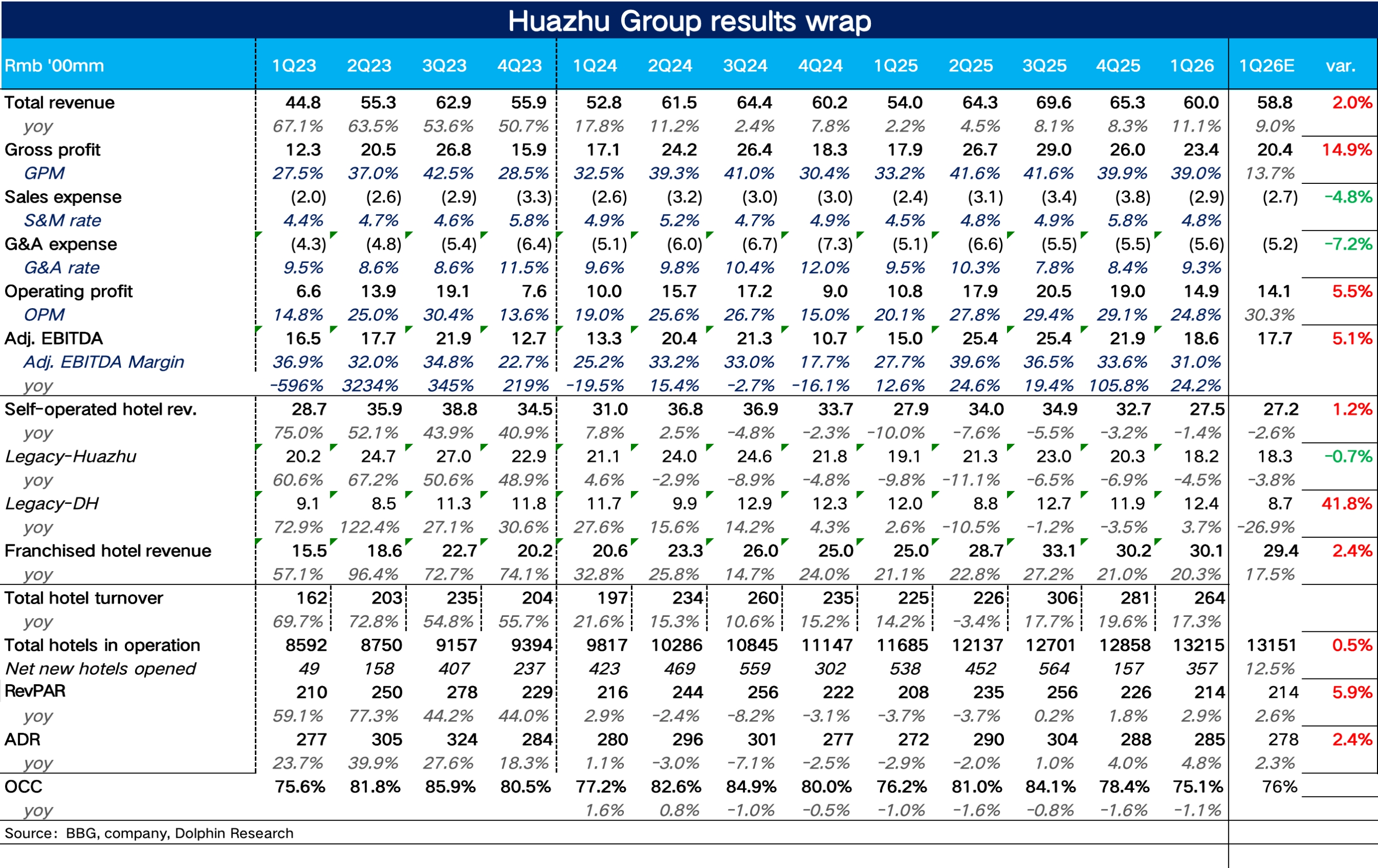

Huazhu 1Q26 First Take: Overall revenue held up well in Q1, and operating metrics kept recovering after turning positive in H2 last year.

That said, with a softer corporate travel rebound, Huazhu stepped up sales spend, which partially weighed on margin release.

1) Revenue growth ticked up QoQ. Total revenue was RMB 6.0bn, up 11% YoY, with a modest sequential acceleration vs. Q4.

Franchise revenue rose 20% YoY to RMB 3.0bn, driven by more rooms and RevPAR back in positive territory, lifting single-hotel GMV.

Self-operated revenue was ~RMB 2.8bn, down 1.4% YoY with a narrower decline QoQ. Dolphin Research estimates a pickup in Tier-1 city business travel, with premium self-operated brands (e.g., Xiyue, Huajiantang) performing better.

2) RevPAR expanded further YoY. RevPAR rose 2.9% YoY to RMB 214 per night.

ADR increased 4.8% YoY, the key driver, helped by mix upgrade from newer versions such as Hanting 3.5/4.0 and All Seasons 5.0. OCC was 75.1%, down 110bps YoY, suggesting robust leisure demand but still-weak corporate travel dragging occupancy.

3) Solid openings with higher-quality growth focus. Net adds were 357 hotels in Q1 (537 openings, 180 closures), keeping a fast pace.

Mid-to-upscale brands (Intercity, Orange Crystal, Mercure) remained the core growth engines, while economy brands focused more on refurbishments. Notably, Huazhu accelerated the cleanup of poorly located, aging, loss-making stores to pursue higher-quality growth.

4) Step-up in sales spend: With a higher franchise mix YoY, GPM expanded 580bps to 39%.

Amid soft corporate travel and intensifying competition, Huazhu appears to have increased placements on Douyin/Xiaohongshu, lifting the S&M ratio by 30bps to 4.8%, while G&A stayed broadly stable. Adj. EBITDA reached RMB 1.86bn, up 24% YoY. $HWORLD-S(01179.HK)

The copyright of this article belongs to the original author/organization.

The views expressed herein are solely those of the author and do not reflect the stance of the platform. The content is intended for investment reference purposes only and shall not be considered as investment advice. Please contact us if you have any questions or suggestions regarding the content services provided by the platform.