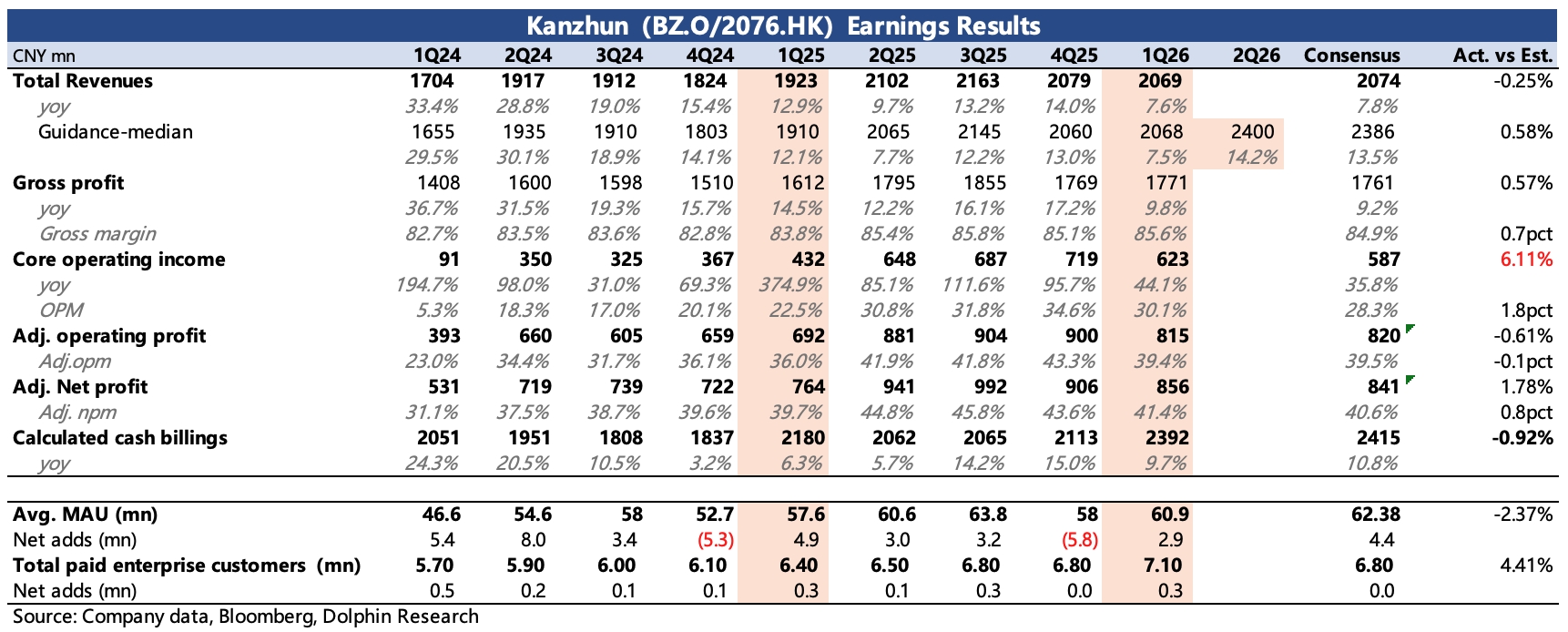

Kanzhun 1Q26 First Take: Q1 results were broadly in line, with a small profit beat on tighter G&A. Core OP was approx. RMB 600 mn (+44% YoY).

Mgmt guides Q2 revenue growth of 14%, an acceleration vs. Q1. Some demand shifted from Q1 to Q2 due to an extended CNY and timing effects, and Sensor Tower data show a sharp rebound post-holiday return to work.

Looking at Q1 and Q2 together, 1H growth is about 11%, roughly flat vs. the same period last year. While not slowing, last year’s base was low, so momentum is best described as stable.

Mgmt has guided ~10% growth over the next two years, constrained by the domestic environment, so more upside on the top line hinges on market expansion. In Hong Kong, penetration is progressing well: the OfferToday platform ranks No.1 by DAU among mainstream recruiting apps and No.2 by MAU. On current trends, it is closing in on JobsDB.

That said, Hong Kong is a small market, so the fastest way to sustain earnings is self-help via cost discipline. With R&D already small, cuts in S&M deliver more leverage. However, the joint sponsorship fee for the World Cup this year (approx. RMB 200 mn) and last year’s ongoing S&M reductions mean near-term tightening will mainly come from G&A, which also drove the Q1 profit beat.

The company still expects adj. OPM to improve this year, albeit by less than the step-up in 2025. Beyond maintaining growth, mgmt also raised the buyback authorization last quarter to support the stock. $Kanzhun(BZ.US) $BOSS ZHIPIN-W(02076.HK)

The copyright of this article belongs to the original author/organization.

The views expressed herein are solely those of the author and do not reflect the stance of the platform. The content is intended for investment reference purposes only and shall not be considered as investment advice. Please contact us if you have any questions or suggestions regarding the content services provided by the platform.