$XIAOMI-W(01810.HK)

Xiaomi's Q1 2026 Earnings Report: Revenue and Net Profit Both Decline, Auto Business Loses 3.1 Billion in a Single Quarter

Key Takeaways:

1. Double-digit declines in both revenue and profit: Q1 total revenue fell 10.9% to RMB 99.14 billion, with adjusted net profit plunging 43.1% year-on-year to RMB 6.07 billion. The core smartphone business saw a significant drop in shipments, compounded by soaring costs for key components like memory, putting its hardware foundation under pressure from macro headwinds and intense industry competition.

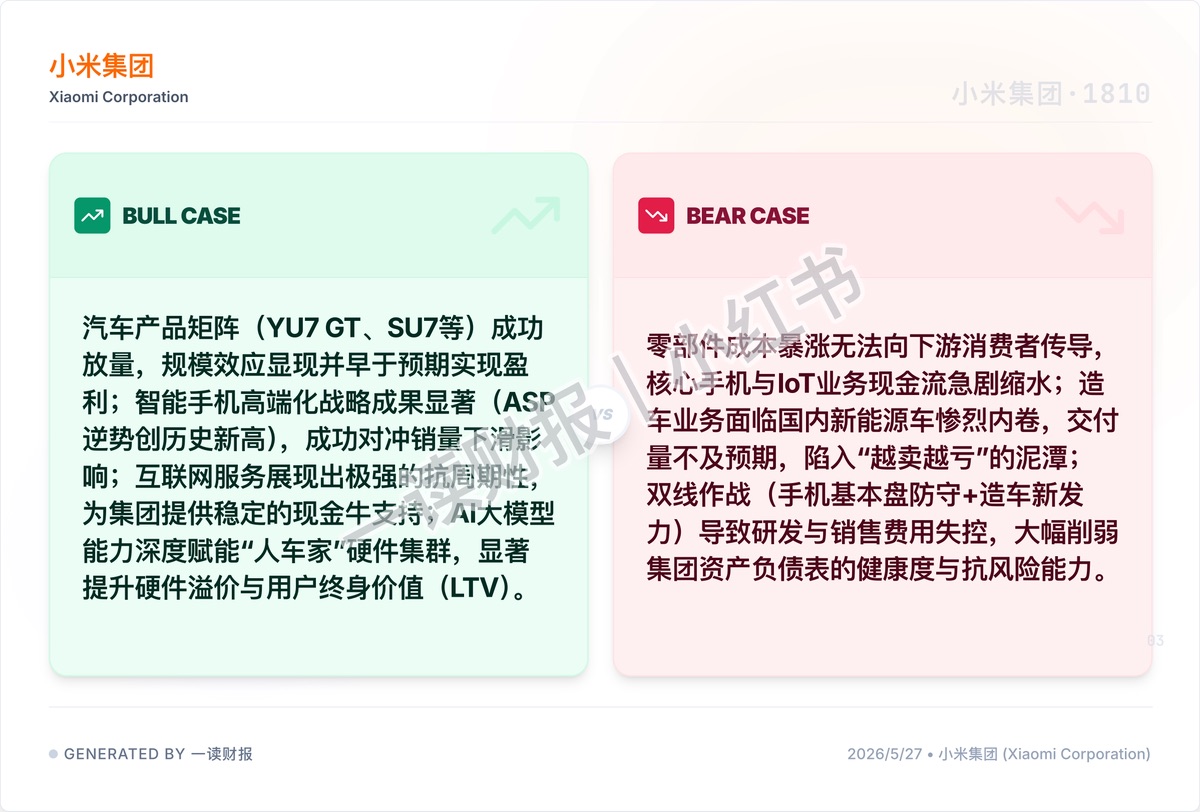

2. Auto business stuck in a "sell more, lose more" quagmire: While smart electric vehicles (EVs) and innovation businesses contributed RMB 19.9 billion in revenue (delivering 80,800 units), the segment's quarterly operating loss reached a staggering RMB 3.1 billion. Amid a brutal domestic new energy price war, a 20.1% gross margin cannot cover the massive fixed costs, making it a heavy-asset beast that continues to devour group profits in the short term.

3. Massive R&D expenditure of RMB 9 billion: Free cash flow turned negative to -RMB 506 million. To support the "Human x Car x Home" ecosystem and underlying AI technology, R&D spending surged 33.4% year-on-year to RMB 9 billion. Xiaomi is forced to use the shrinking cash flow from its phone and IoT businesses to fund investments in auto manufacturing and AI infrastructure.

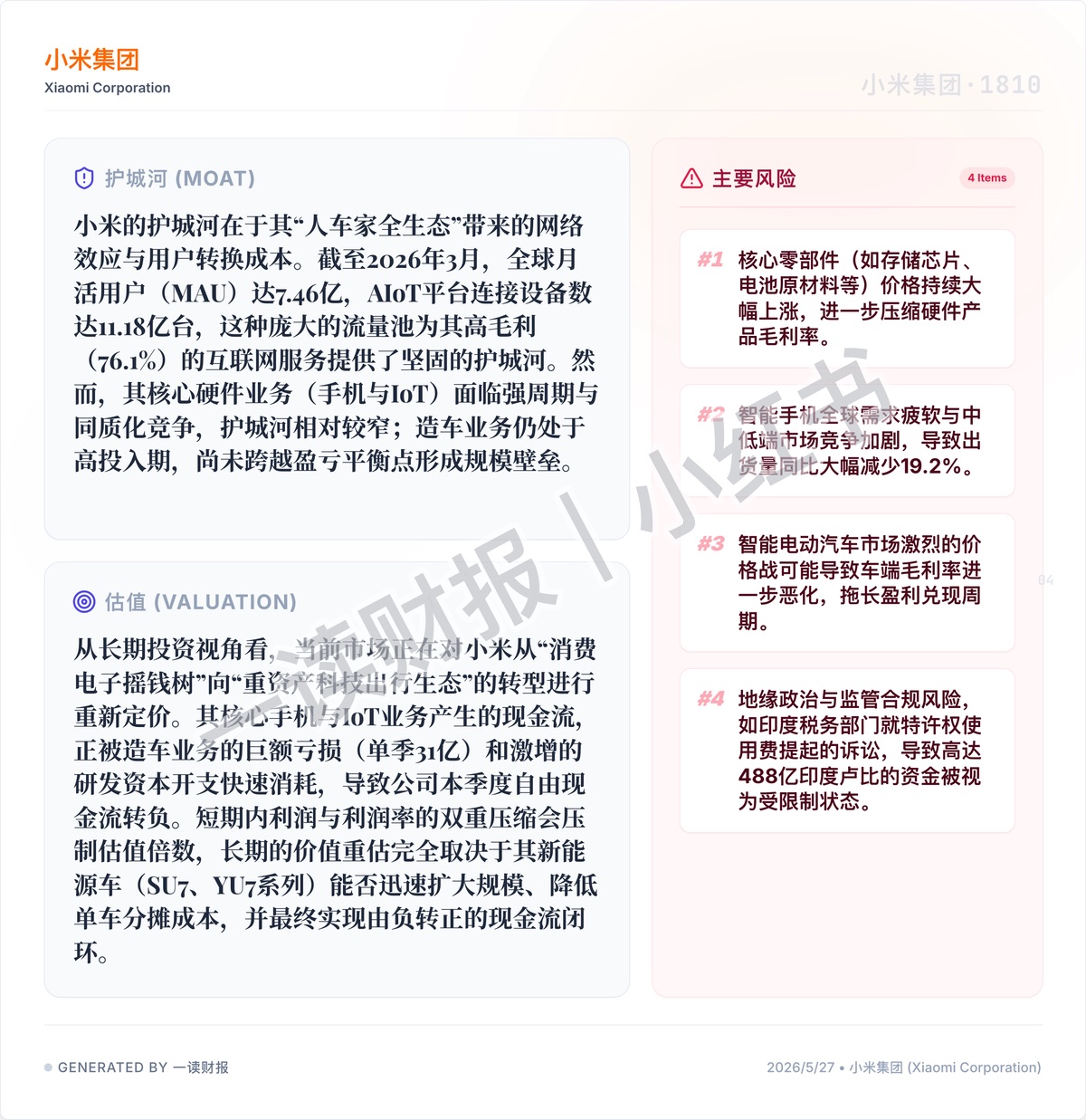

4. High-margin internet services act as a "breakwater": At a time when hardware is under full pressure, the internet services business, with its high gross margin of 76.1% and deep network effects from a massive global MAU of 746 million, provides crucial counter-cyclical profit support, preventing a collapse of the group's overall financial statements.

5. Valuation logic rift and the test of heavy-asset transformation: The capital market is painfully re-pricing Xiaomi from a "light-asset consumer electronics" company to a "heavy-asset tech manufacturing" one. Although the "Human x Car x Home" ecosystem creates high user switching costs, heavy capital expenditures will continue to suppress its valuation ceiling until core models like the SU7 cross the breakeven point and generate positive free cash flow.

Xiaomi is in a transitional period of "the old throne shaking, the new crown unsteady." The bleeding of its core smartphone business and the massive losses from its auto venture have breached its cash flow defenses. This is an all-in bet, wagering the entire group's foundation on the "Human x Car x Home" ecosystem and the future of AI.

Source: Yidu Caibao, providing original earnings report download.

#HKStockEarnings #XiaomiCorporation #SmartCarEcosystem #ConsumerElectronics #HardTechBusiness #BusinessModel #EarningsInfographic #DataVisualization #ResearchReportAnalysis #YiduCaibao

The copyright of this article belongs to the original author/organization.

The views expressed herein are solely those of the author and do not reflect the stance of the platform. The content is intended for investment reference purposes only and shall not be considered as investment advice. Please contact us if you have any questions or suggestions regarding the content services provided by the platform.