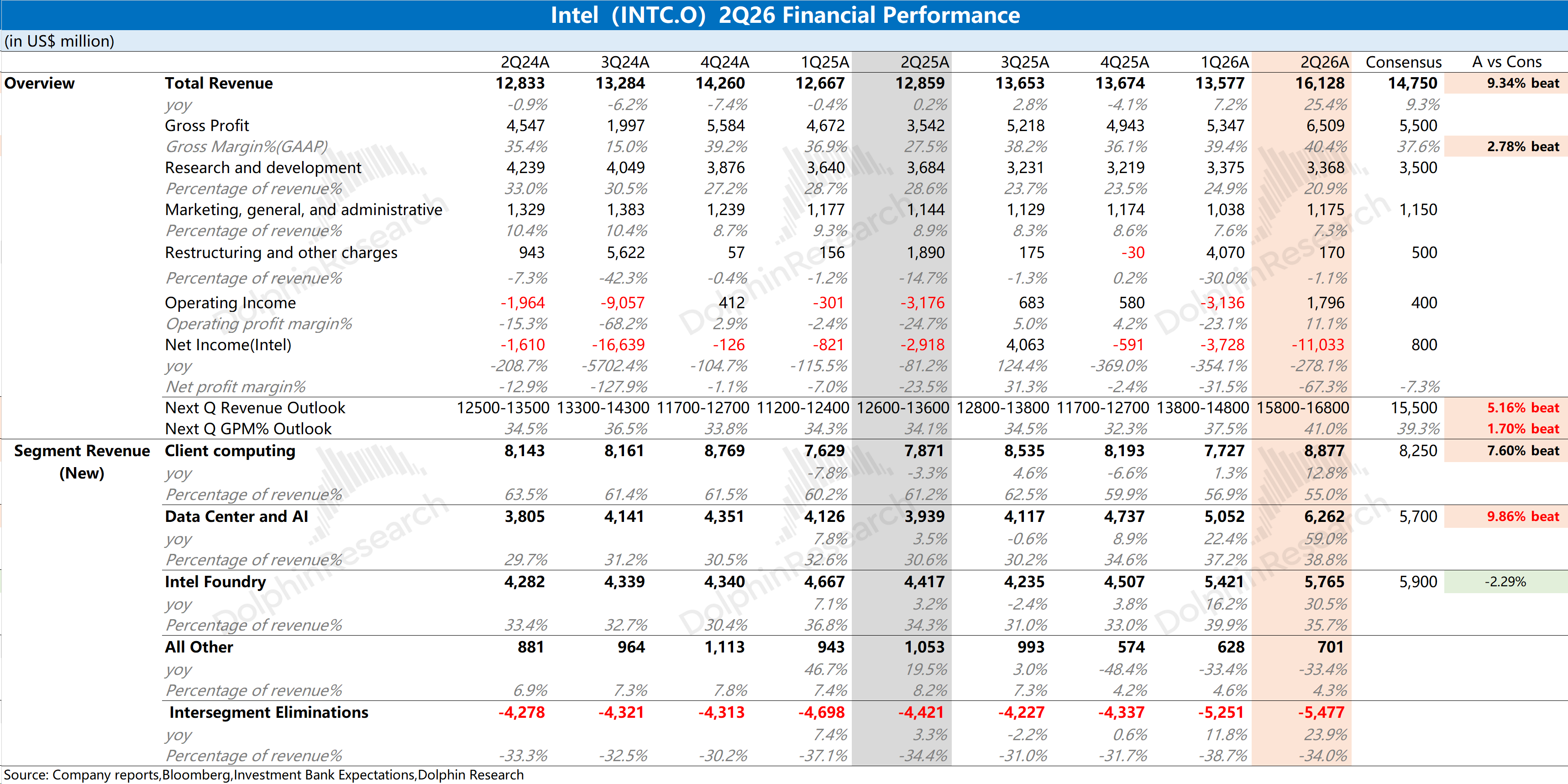

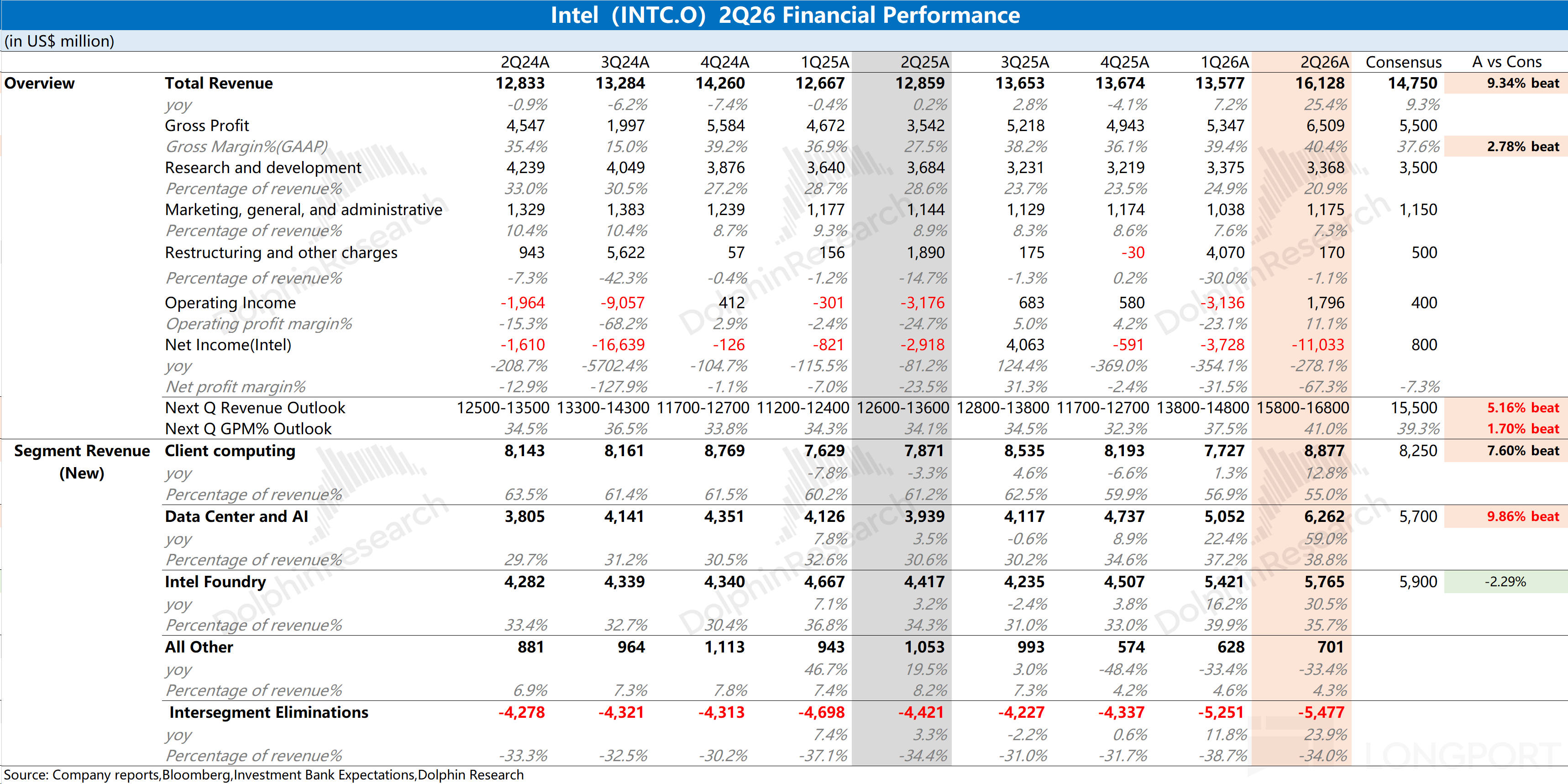

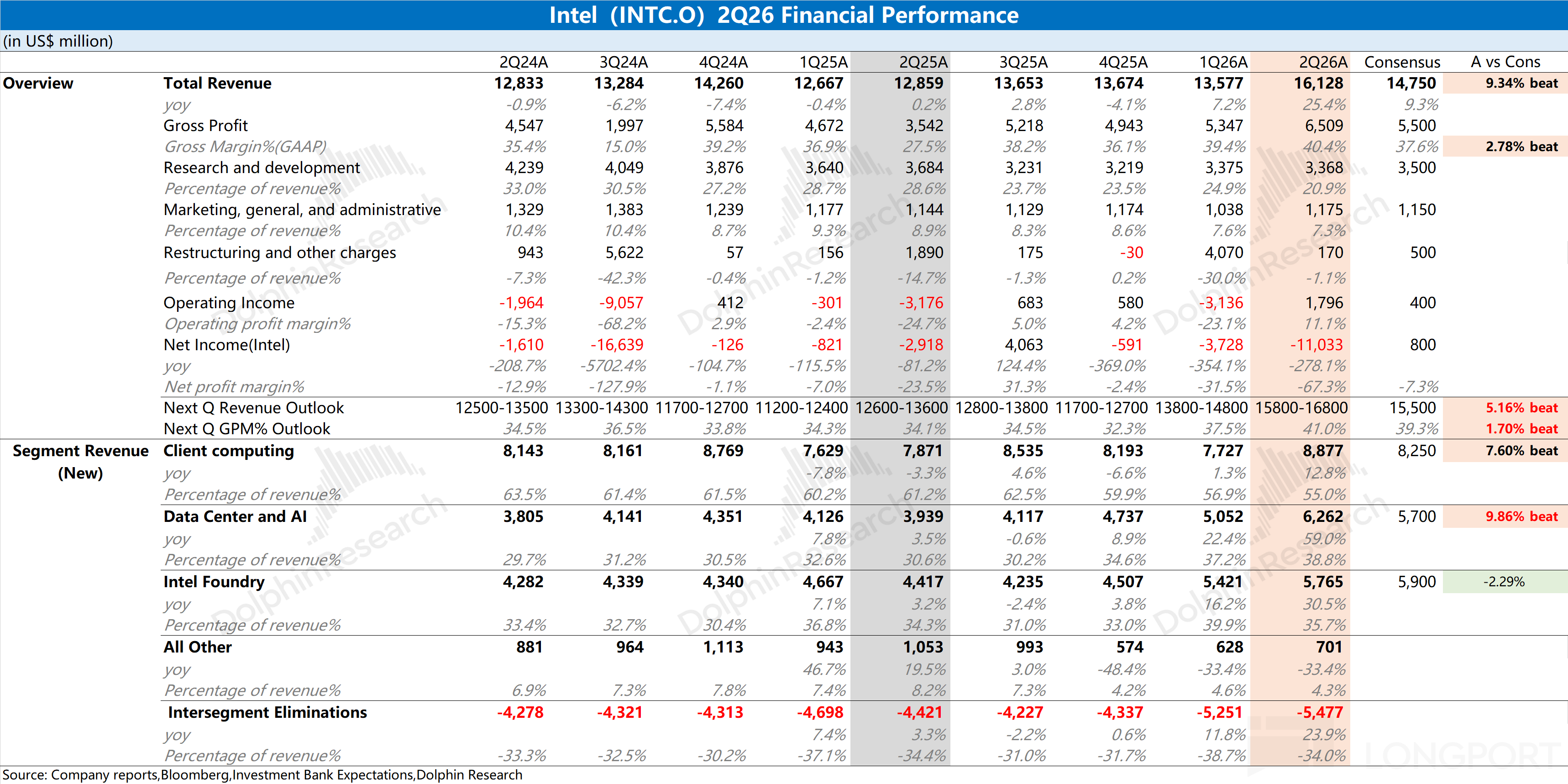

INTC 2Q26 First Take: another beat this quarter.Revenue growth accelerated, driven by Client Computing and Data Center & AI, with CPU price increases the biggest swing factor.GPM continued to expand as pricing tailwinds offset dilution from the 18A ramp.

Intel’s wafer capacity still primarily serves its own products.External foundry revenue was approx. $300mn this quarter, about 2% of the company’s overall Foundry Mfg. Dept. revenue.

Guidance for next quarter is solid.The company expects revenue of $15.8–16.8bn (+15% to +23% YoY), ahead of the Street at $15.5bn.Strength is led by demand for server CPUs.

GPM (GAAP) is guided to approx. 41% next quarter, up QoQ and above the Street at 39.3%.Management reaffirmed that keeping GPM sustainably above 40% remains the top priority.

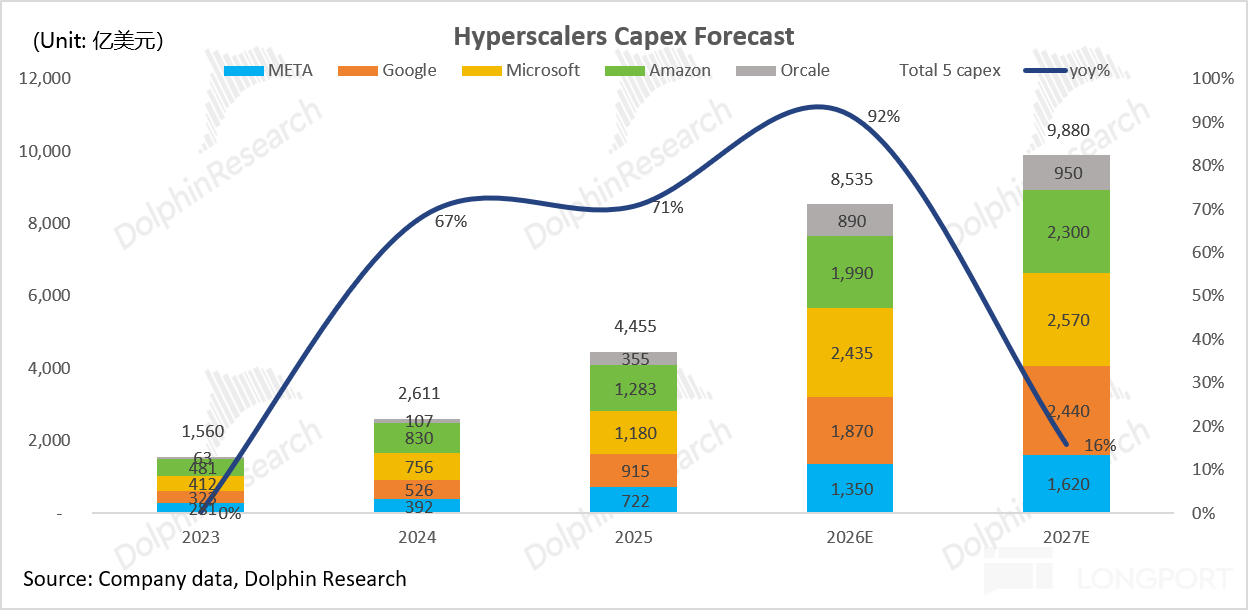

The recent pullback in the stock reflects headlines around Meta’s compute leasing and the K3 model, which stoked concerns about the durability of big tech Capex.That pressured the broader sector, especially the price-hike beneficiaries.

This print underscores resilient CPU momentum, with the upside again largely price-driven.Compared with other semi names, INTC still trades at a premium, which also embeds expectations for the foundry business.

The current CPU price-hike cycle is a transitory tailwind, helping stabilize confidence in a fragile market.A meaningful external foundry order/revenue contribution is needed to unlock greater upside, and that is what investors most want to see.For more, follow Dolphin Research. $Intel(INTC.US)