Mu has once again saved the world

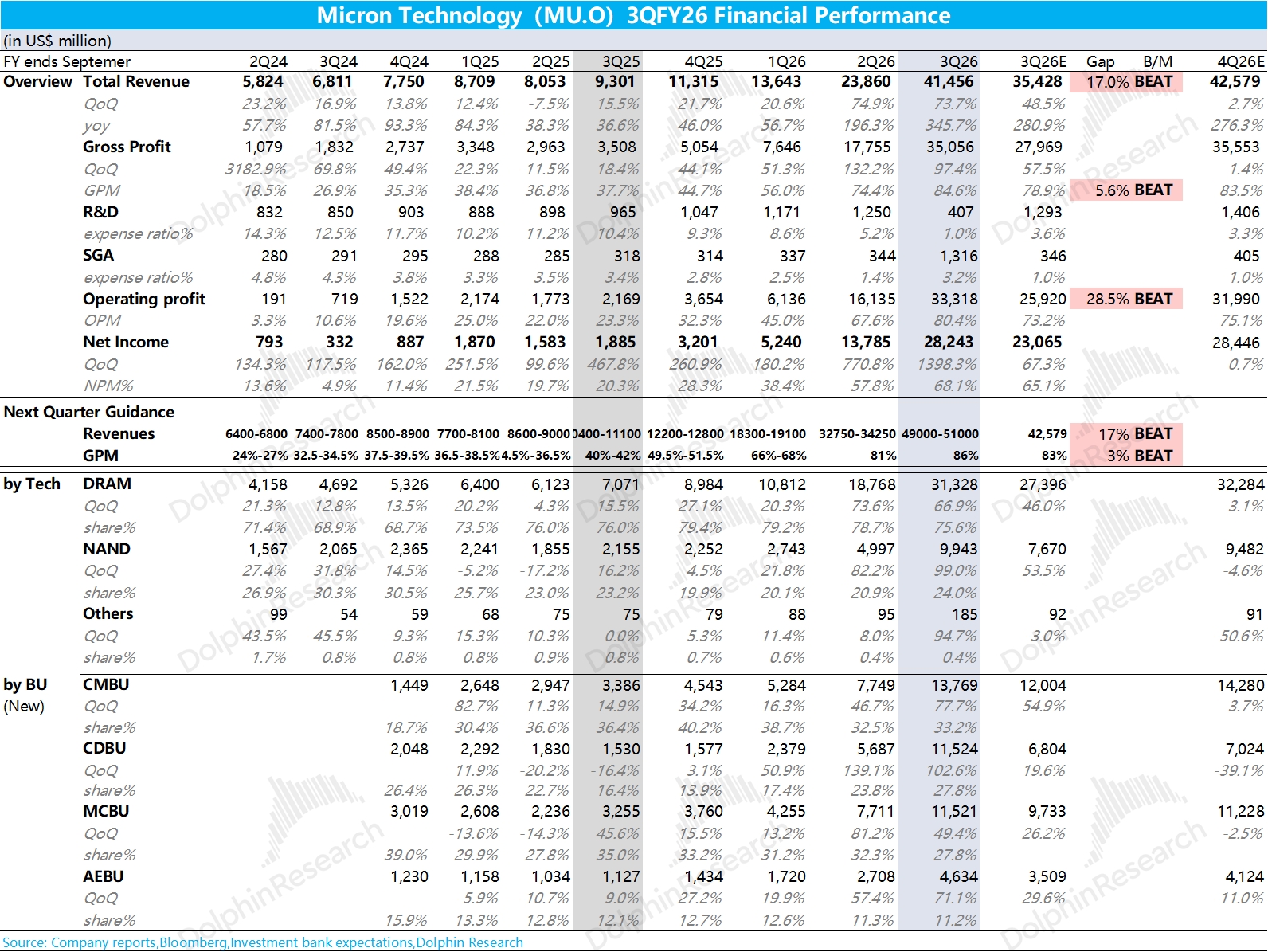

MU 3Q26 First Take: in a word, stellar. Revenue, profit, and next-quarter guide all beat across the board.

Revenue jumped 74% QoQ, roughly matching last quarter's pace. Volumes contributed only low-to-mid single digits, with growth driven mainly by pricing.

GPM surged to 85%, well ahead of the Street. With stable operating leverage, OPM topped 80%. $41.5bn of revenue converted into $33.3bn of profit.

More importantly, the company guided to around $50.0bn for next quarter. That is well above the $42.6bn consensus.

The guide implies ~20% QoQ growth, broadly in line with expectations. Given shipment timing, pricing for the new quarter was not fully locked when the guide was set, so management typically builds in a buffer. Post-guide, bullish expectations moved higher.

EPS guidance essentially matches the most bullish buyside view at around $30. The 86% GPM guide (vs. the Street's 83%) reinforces that in this unprecedented supercycle, price-led revenue gains are flowing through to profit. With OPM approaching ~75%, the Agentic AI boom shows compute and memory matter equally.$Micron Tech(MU.US)

The copyright of this article belongs to the original author/organization.

The views expressed herein are solely those of the author and do not reflect the stance of the platform. The content is intended for investment reference purposes only and shall not be considered as investment advice. Please contact us if you have any questions or suggestions regarding the content services provided by the platform.