Memory storage is undergoing a frenzied production expansion, ushering semiconductor equipment into a 'super cycle'!

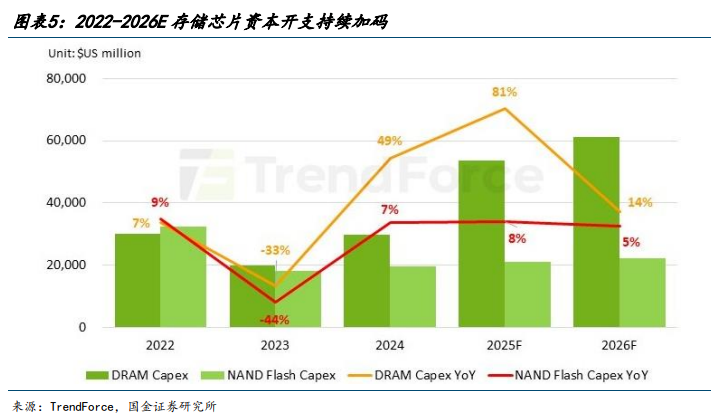

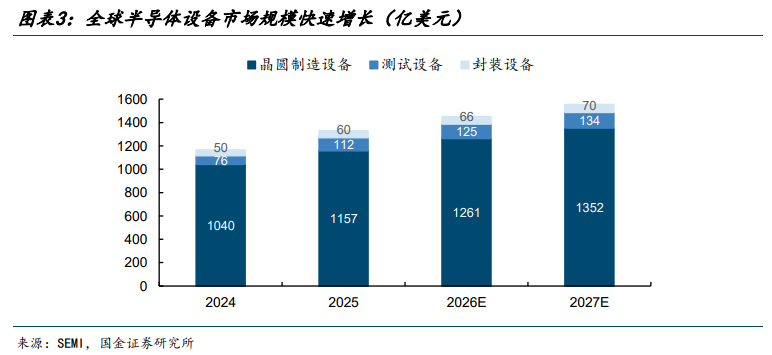

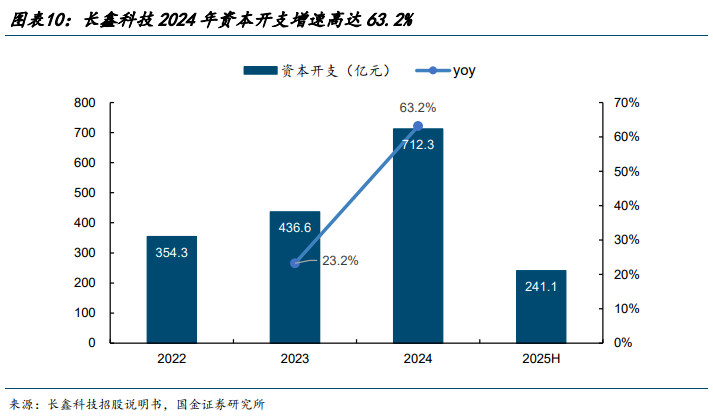

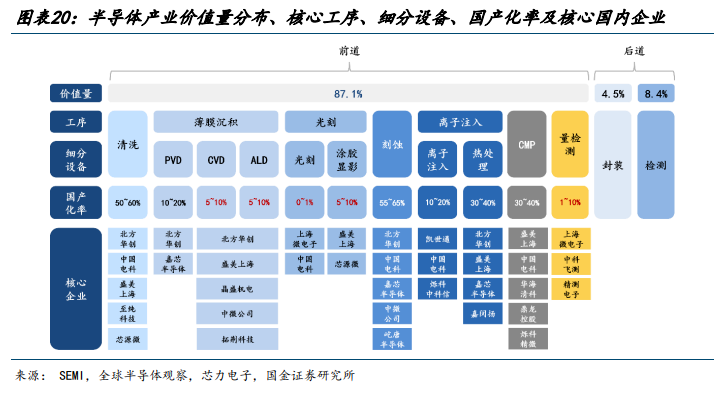

Data from SEMI reveals a strong upward trajectory for the semiconductor sector. The overall global market for semiconductor equipment is projected to climb from USD 116.6 billion in 2024 to USD 155.6 billion by 2027, growing at a steady compound annual growth rate (CAGR) of 10.1%. Within this broader expansion, testing equipment stands out for its high market elasticity. The specialized testing segment is expected to nearly double, jumping from USD 7.6 billion in 2024 to USD 13.4 billion in 2027. This rapid surge represents a much sharper CAGR of 21.1%, outpacing the wider equipment market. Supply-side constraints are intensifying the cyclical swings of the market. Global equipment manufacturers are facing a severe squeeze from critical component shortages and maxed-out production capacity. As a result, lead times for key front-end and memory-support hardware have stretched to a massive 12 to 24 months, alongside rising prices. These shipment bottlenecks are directly delaying the expansion plans of industry giants like Samsung, SK Hynix, and Micron. However, this backlog is creating an ideal strategic window for domestic Chinese equipment suppliers. It gives them a prime opportunity to accelerate local import substitution while simultaneously diversifying and expanding their global customer base. AI servers drive up memory consumption, widening the supply-demand gap The root cause of this equipment cycle lies in the significantly higher memory consumption of AI servers compared to traditional servers. Estimates indicate that a single AI server uses 8 to 10 times more DRAM and approximately 3 times more NAND than a conventional server. While demand is rising, supply of general-purpose memory has not expanded in parallel. Samsung and SK Hynix have allocated 80% to 90% of their advanced-node capacity to HBM production, while Micron has redirected around 70% of its capacity toward HBM and high-end DDR5. Inventory levels at the three major memory manufacturers stand at approximately four weeks, well below the healthy safety stock range of 8 to 12 weeks. Prices have already responded accordingly. According to TrendForce, Q2 2026 contract prices for DDR5 are forecast to rise 58% to 63% quarter-over-quarter, while NAND Flash contract prices are expected to increase 70% to 75% sequentially. The HBM capacity shortfall is estimated at 50% to 60%. The memory market is also expanding. The global memory chip market was valued at USD 192.9 billion in 2024, rising to USD 289.0 billion in 2025, and is projected to reach USD 377.5 billion in 2026, with potential growth to USD 723.7 billion by 2030—a compound annual growth rate of 17.7% from 2025 to 2030.Memory manufacturers are ramping up capacity, providing a solid foundation for equipment order fulfillmentAccording to TrendForce data, global DRAM capital expenditure is projected to rise from USD 53.7 billion in 2025 to USD 61.3 billion in 2026, an increase of 14% year-over-year; NAND capital expenditure is expected to grow from USD 21.1 billion in 2025 to USD 22.2 billion in 2026, up 5% year-over-year. Combined capital expenditure by Samsung, SK Hynix, and Micron in 2026 is forecast to reach USD 53.5 billion, a 16% increase compared to 2025.Micron is leading in capacity expansion efforts. Its planned capital expenditure for 2026 amounts to USD 27 billion, representing a 70.3% year-over-year increase. SK Hynix reported year-over-year capital expenditure growth rates of 65.8% in 2024 and 75.5% in 2025. Domestic memory manufacturers are also ramping up investments. ChangXin Technology reported revenue of RMB 24.18 billion in 2024, up 166.1% year-over-year; for the first three quarters of 2025, revenue reached RMB 32.08 billion, a 97.8% year-over-year increase. In terms of capital expenditure, ChangXin Technology invested RMB 71.23 billion in 2024, a 63.2% year-over-year increase.Capacity expansions by ChangXin Technology and Yangtze Memory Technologies (YMTC) are driving more direct demand for domestic equipment. ChangXin Technology plans to add 50,000 to 60,000 wafers per month in monthly production capacity by 2026, corresponding to equipment procurement expenditures of approximately RMB 35–43 billion. YMTC’s Phase III project has entered the equipment installation and commissioning stage and is expected to commence large-scale mass production in the second half of 2026, with associated equipment procurement valued at around RMB 20 billion.Extended overseas delivery timelines create a dual opportunity window for domestic equipment suppliers.Global semiconductor component lead times have significantly lengthened in 2026. Automotive-grade 32-bit MCUs now have lead times exceeding 52 weeks, SiC components range from 25 to 40 weeks, and analog ICs range from 20 to 48 weeks. Component shortages are now adversely impacting equipment delivery schedules. Leading overseas equipment manufacturers such as Applied Materials and Tokyo Electron face constraints due to shortages of critical components and saturated production capacity, extending delivery lead times for certain equipment to 12–24 months. This presents a window of opportunity for domestic equipment vendors. Chinese manufacturers have already established product portfolios in etching, thin-film deposition, cleaning, and testing, offering clearer advantages in delivery efficiency and cost. Overseas wafer fabs, under pressure to expand capacity, are beginning to engage with domestic suppliers, with markets in South Korea and Southeast Asia emerging as potential sources of incremental demand. However, opportunities are not evenly distributed. Success in securing overseas qualifications and repeat orders ultimately depends on process stability, customer validation timelines, and delivery capability.Domestic supply chain gaps determine where equipment flexibility lies.The localization rate for cleaning equipment has reached 50% to 60%, while etching equipment stands at 55% to 65%. For CMP and thermal processing, the rate is between 30% and 40%. However, it remains low in high-barrier segments: PVD at 10% to 20%, CVD/ALD and coat-develop systems each at 5% to 10%, metrology and inspection at only 1% to 10%, and lithography equipment at just 0% to 1%.This is also why front-end metrology and back-end testing have been prioritized. Although they do not represent the largest segments by equipment volume, they constitute clearer bottlenecks with greater potential for domestic substitution.Front-end metrology and inspection represent one of the most critical bottlenecks for domestic equipment.Metrology and inspection equipment is used throughout the front-end wafer fabrication process to measure parameters such as film thickness, critical dimensions, and wafer surface defects. It is not merely a final quality check but an integral part of process control during lithography, etching, and thin-film deposition steps, directly affecting yield.According to SEMI, metrology and inspection equipment accounts for approximately 13% of the global semiconductor equipment market. QYResearch data shows that the global semiconductor metrology and inspection market was valued at approximately USD 19.22 billion in 2025, is projected to reach USD 21.3 billion in 2026, and could grow to USD 32.1 billion by 2030, representing a compound annual growth rate (CAGR) of 10.8% from 2026 to 2030.With a localization rate of only 1% to 10%, the segment remains constrained by the fact that high-precision hardware and software are dominated by overseas leaders, wafer fabs require lengthy verification cycles, customers are reluctant to switch suppliers, and export controls have further amplified supply chain uncertainty.Once domestic manufacturers pass validation, the value of subsequent repeat orders increases. Demand for testing will rise with advancements in memory, advanced process nodes, increased 3D NAND layer counts, and advanced packaging.The value of back-end FT testing is being repriced upward.Testers are the core component of semiconductor test equipment. In the back-end testing equipment sector, testers account for approximately 63% of the total value, with memory testers representing about 21% of the overall tester market.The memory test equipment market is nearly monopolized by overseas industry leaders. In 2023, Advantest held a 56% share of the global memory tester market, while Teradyne accounted for 43%, together totaling 99%. Domestic vendors have primarily entered the mid-to-low-end memory testing and ancillary equipment segments, with high-end memory ATE systems remaining a key weakness.The importance of FT testing is increasing. CP testing occurs after wafer fabrication but before packaging and primarily screens basic electrical parameters. FT testing takes place after packaging and, in addition to verifying basic electrical parameters, also validates system-level functionality, dynamic parameters, timing characteristics, bandwidth speed, and signal integrity. FT testing imposes higher requirements on channel count, test frequency, high-speed signal processing capability, and timing precision.Pricing also reflects this gap. International high-end FT testers are priced above RMB 11 million per unit, compared to RMB 9 million per unit for high-end CP testers. According to QYResearch, the global FT final test equipment market is projected to reach USD 3.84 billion in 2025, USD 4.1 billion in 2026, and grow to USD 5.47 billion by 2030, representing a compound annual growth rate (CAGR) of 7.5% from 2026 to 2030.Huawei’s ‘Tao’s Law’ has further elevated the strategic value of back-end processes. Technologies such as 3D stacking, chiplets, hybrid bonding, and TSVs mean that chip performance no longer relies solely on front-end geometric scaling. As packaging and testing complexity increases, back-end equipment is no longer merely a supporting element.

The copyright of this article belongs to the original author/organization.

The views expressed herein are solely those of the author and do not reflect the stance of the platform. The content is intended for investment reference purposes only and shall not be considered as investment advice. Please contact us if you have any questions or suggestions regarding the content services provided by the platform.

Post your comment

No Comments