$SMIC(00981.HK)$Taiwan Semiconductor(TSM.US)

This is why I don't like the second-place players. As latecomers trying to catch up, their revenue growth can't match the leader, and their gross margin is several orders of magnitude behind.

The same goes for Alibaba's cloud business—growth is too slow, gross margin is still declining, and the gap with Azure/AWS/GCP is widening.

Actually, AMD is the same, but at least it's a U.S. company with a liquidity premium. As a China concept stock, don't even think about replicating the "hero vs. dragon" narrative.

SMIC (Minutes): Demand slows in the fourth quarter, currently not considering accelerating capacity expansion.

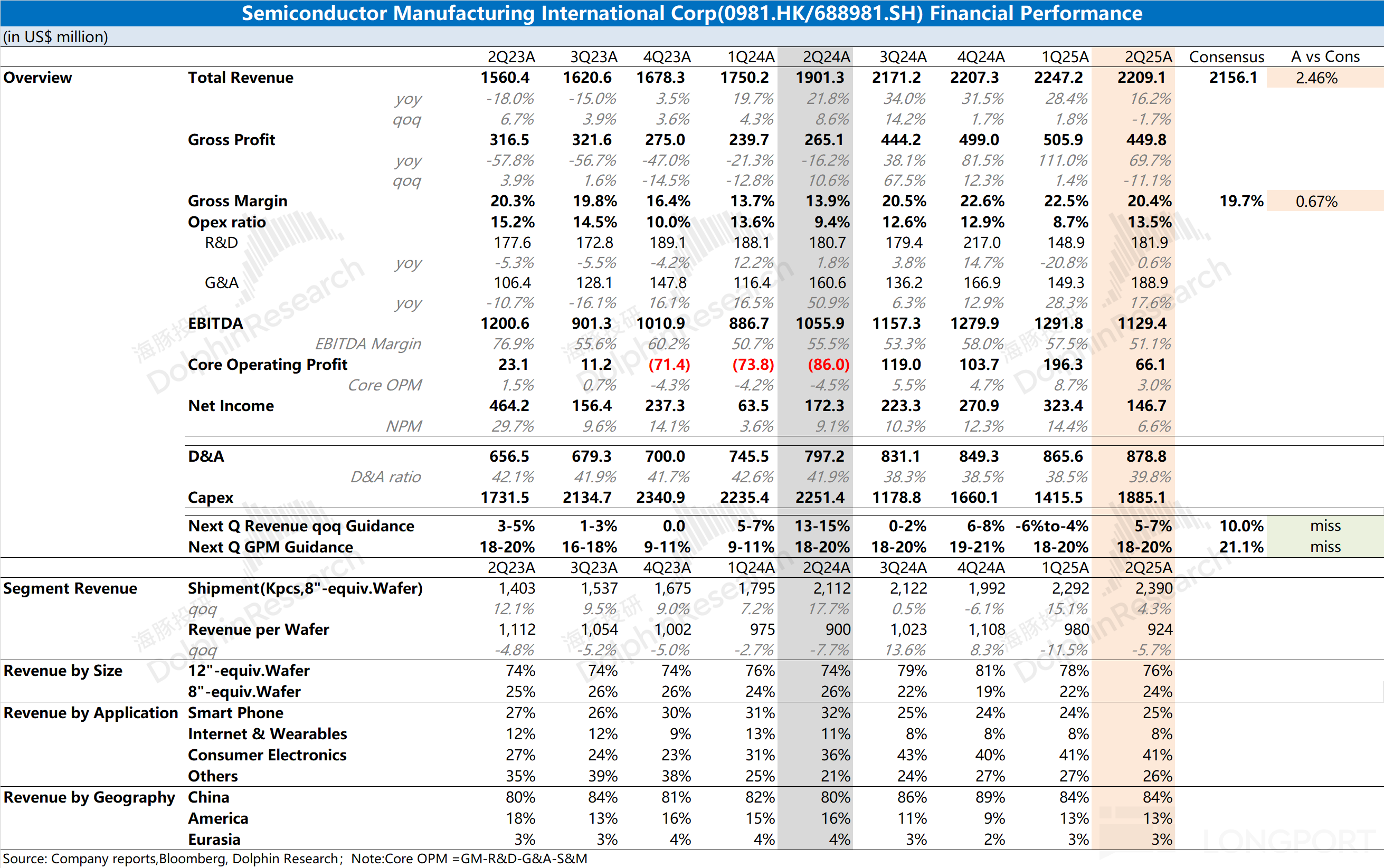

The following are the minutes of the Q2 2025 earnings call for $SMIC(00981.HK) organized by Dolphin Research. For an interpretation of the earnings report, please refer to "SMIC: 'Hot' Valuation Meets 'Cold' Answers, Is the Revaluation Road Suspended?". I. $SMIC(688981.SH) Review of Core Financial Information 1. Q3 2025 Performance Guidance: Revenue is expected to grow by 5% to 7% quarter-on-quarter. Gross margin: Expected to be in the range of 18% to 20%...

The copyright of this article belongs to the original author/organization.

The views expressed herein are solely those of the author and do not reflect the stance of the platform. The content is intended for investment reference purposes only and shall not be considered as investment advice. Please contact us if you have any questions or suggestions regarding the content services provided by the platform.