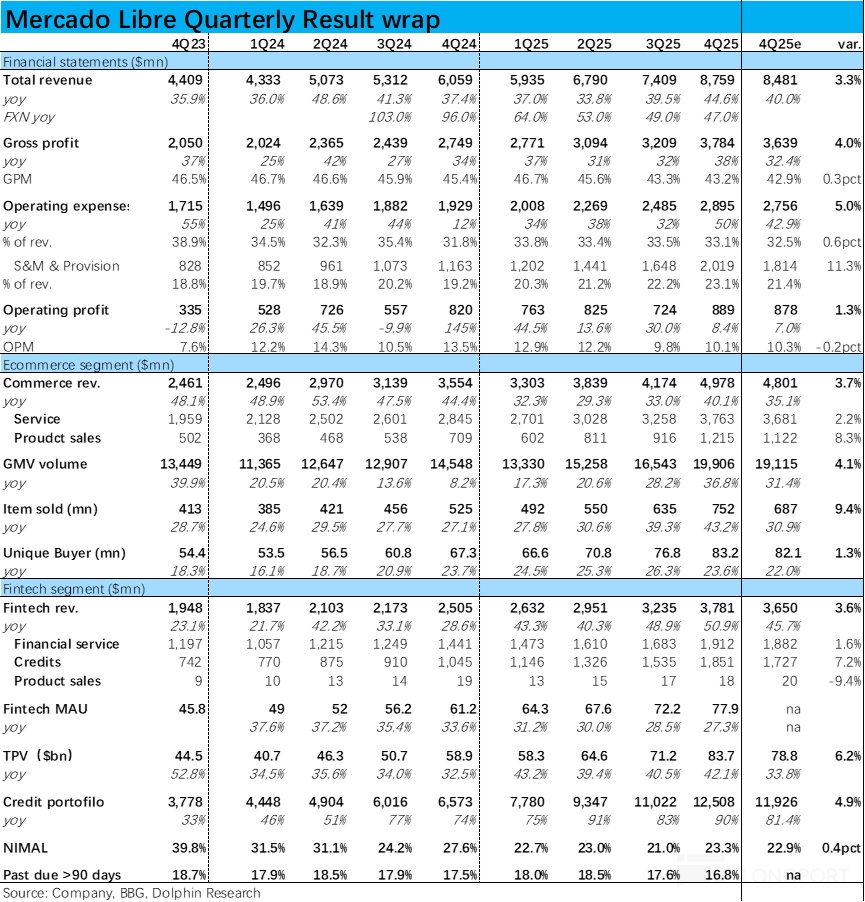

MELI: LatAm's 'Alibaba' with a split personality — a rev. giant, profit minnow---

Latin America's 'Alibaba' — Mercado Libre (hereafter 'MELI') saw its shares spike post-earnings and then reverse. Overall, the quarter was solid. The after-hours drop likely reflects negative commentary on the call; we will publish the call transcript next.

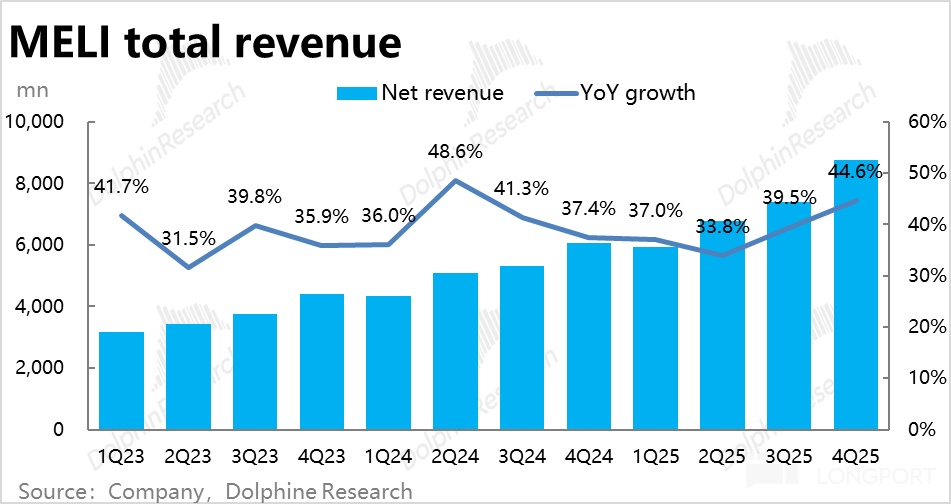

1) Strong topline, margins under pressure: Total revenue rose nearly 45% YoY, a clear acceleration vs. last quarter. The uplift was largely FX-driven, as constant-currency revenue growth was 47% and modestly slower vs. last quarter.Despite healthy growth, margins remained pressured by elevated logistics infrastructure, customer acquisition, and credit provisioning.

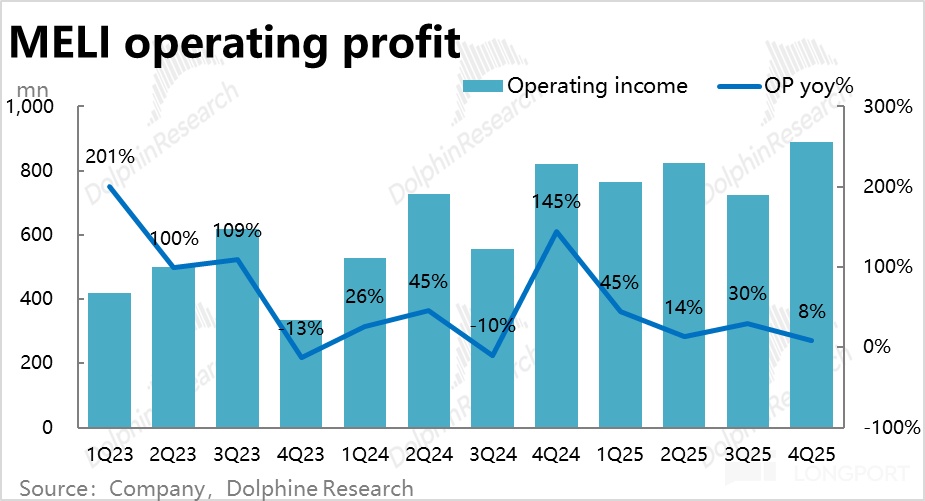

OPM was 10.1%, down over 3pct YoY and slightly below Bloomberg consensus. With revenue materially beating estimates, OP came in at approx. $890mn (+~8% YoY).

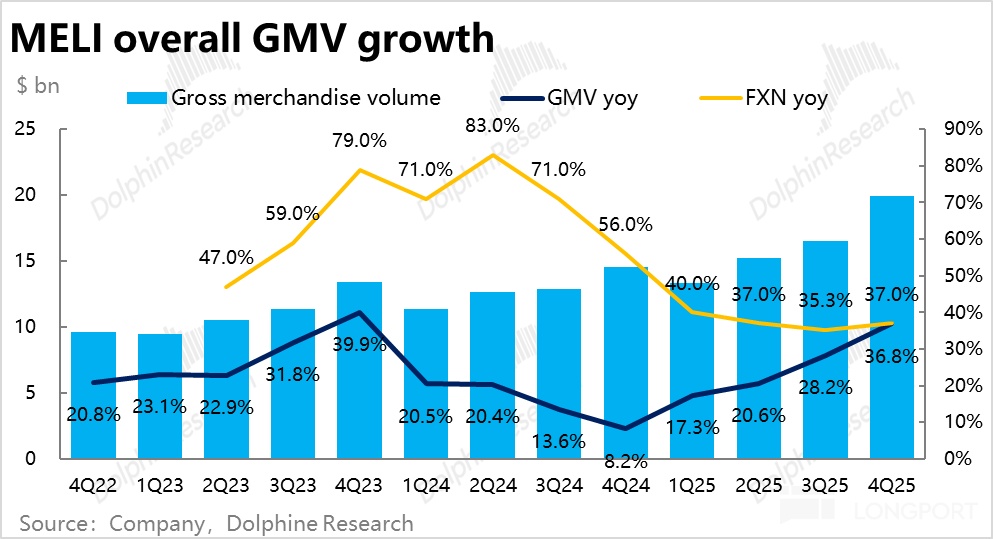

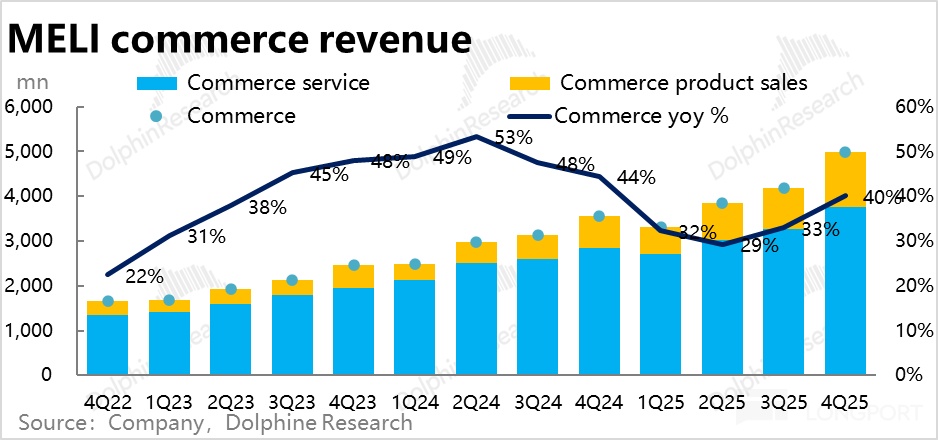

2) Logistics efficiency up, ecommerce momentum strong: In the core commerce business, GMV grew nearly 37% YoY, a sharp acceleration from 28% last quarter.While the faster pace was also largely FX-aided, constant-currency GMV growth still accelerated by roughly 2pct.

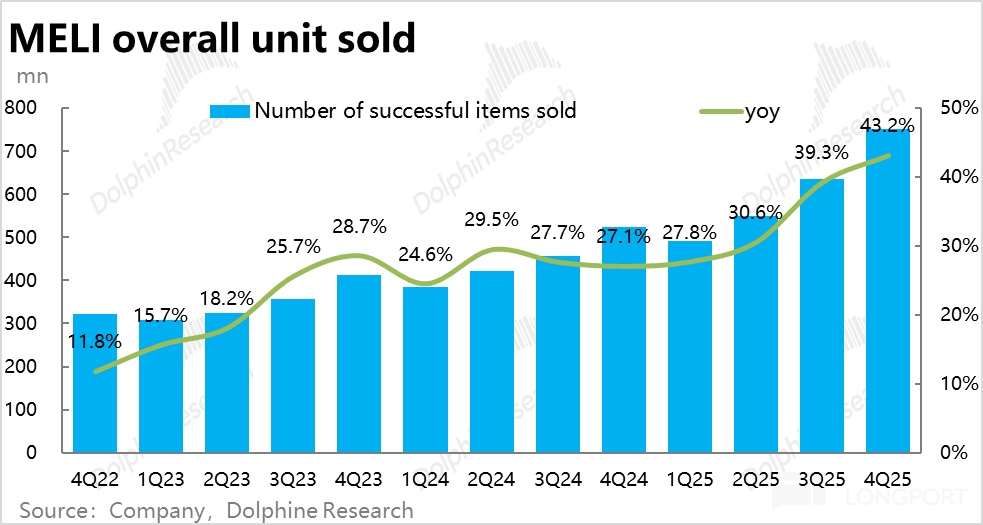

Moreover, order volume rose 43% YoY, up about 4pct vs. last quarter. This clearly signals faster organic growth driven by logistics improvements and user-base expansion.

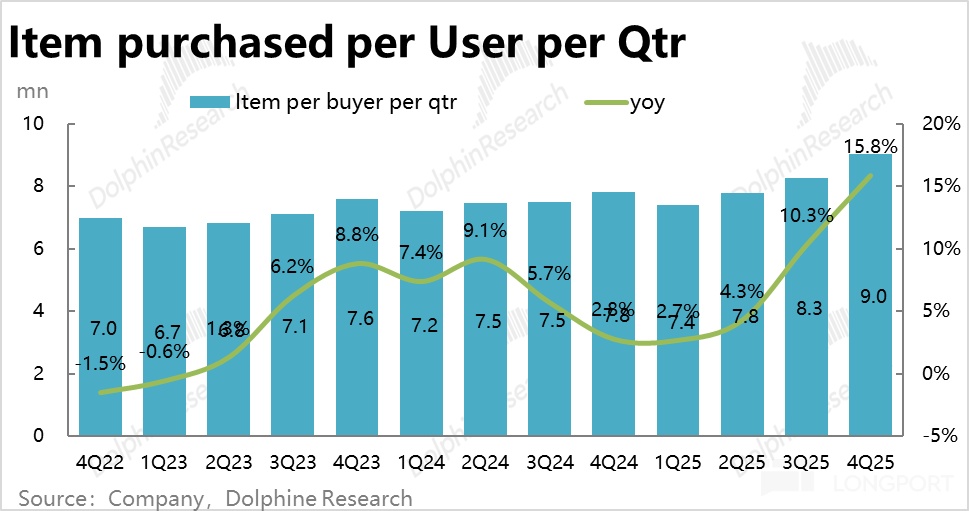

Digging deeper, orders per buyer reached 9 this quarter, up 16% YoY. This is the key driver of acceleration, reflecting higher purchase intent after lowering the free-shipping threshold.

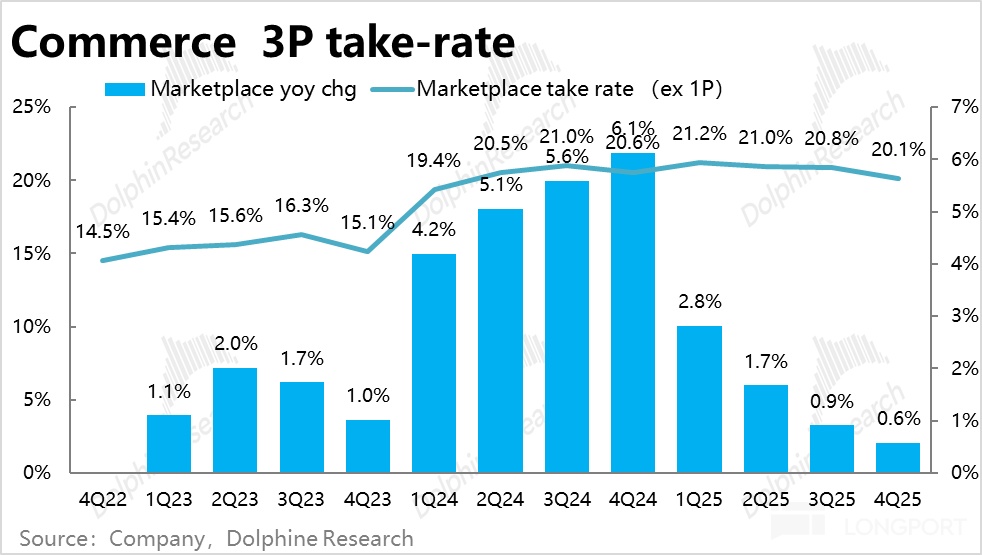

3) Monetization uplift slowed amid subsidies; 1P outgrowing: On revenue, 1P product sales grew over 70% YoY, outpacing the overall commerce business. Management reiterated that 1P is a strategic investment focus, with efforts in order automation, merchandise supply, and supermarket category margin improvement.3P service revenue rose ~32% YoY, and the 3P take rate was 20.1%. YoY take-rate expansion slowed to just 0.6pct (a new low), reflecting lower free-shipping thresholds and profit-sharing with merchants/consumers to drive growth and capture share.

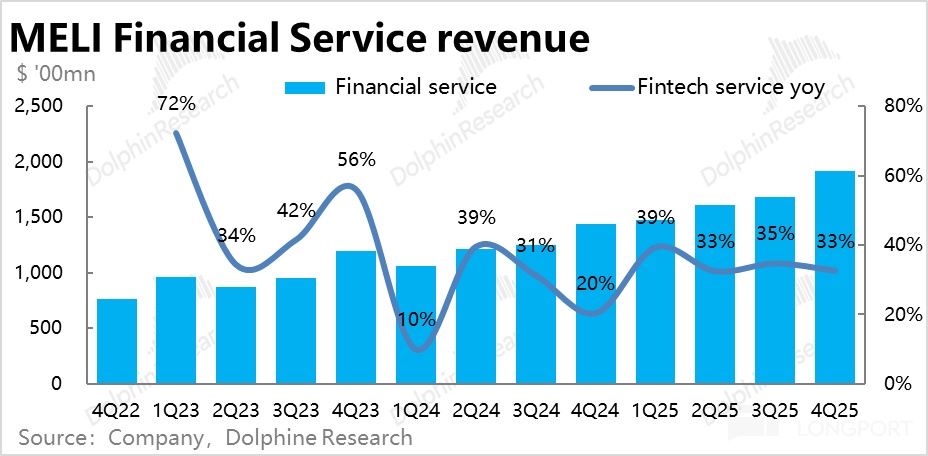

4) Payments steady: In the financial segment’s payments business, TPV rose 42% YoY, faster than last quarter but mainly FX-driven. Payment order count grew about 35.5% YoY, slightly slower vs. last quarter.

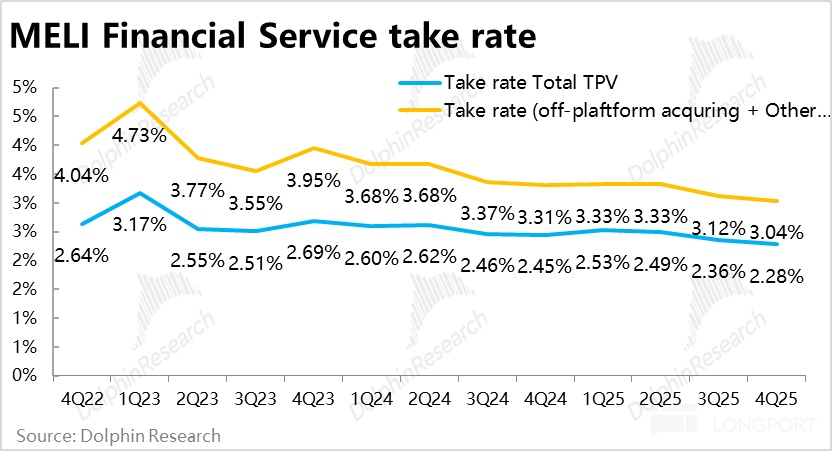

By component, non-acquiring payments (e.g., digital wallet) grew faster at ~64%, while acquiring TPV grew ~33%. Within acquiring, on-platform TPV rose 36% YoY, outpacing off-platform at 32% due to stronger ecommerce growth in USD terms.As we have noted, fee rates continue to trend down, and financial services revenue rose 33% YoY, with growth decelerating.

5) Credit lending remains strong: Loans outstanding reached $11.0bn (+90% YoY), sustaining rapid growth.All four loan categories accelerated vs. last quarter, with credit cards remaining the strongest. Despite already being the largest book, credit cards still grew ~115% YoY.

Avg. loan size rose ~47% YoY, while loan accounts increased ~30% YoY. The primary driver is larger average balances, with account growth steady.

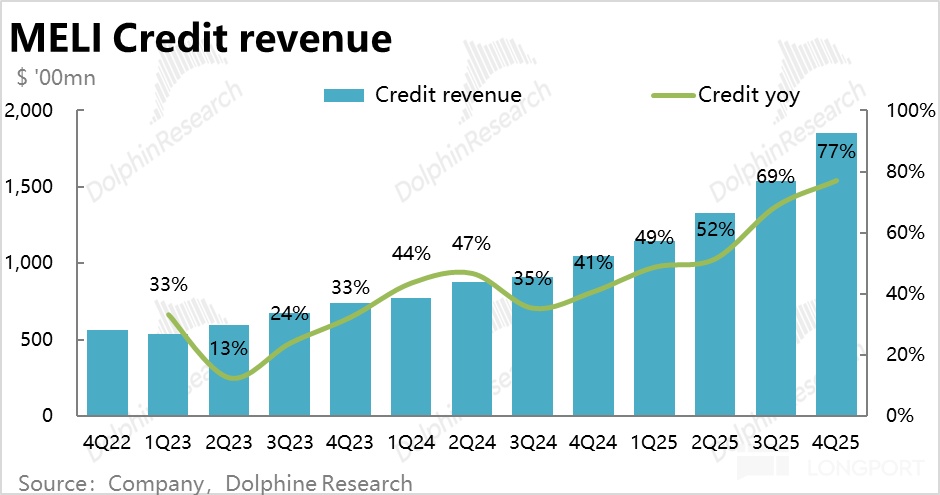

6) NIMAL improved at the margin: Credit-related revenue was $1.85bn (+77% YoY), with acceleration vs. last quarter. Beyond loan balance growth, avg. loan GP margin ticked up to ~63%.

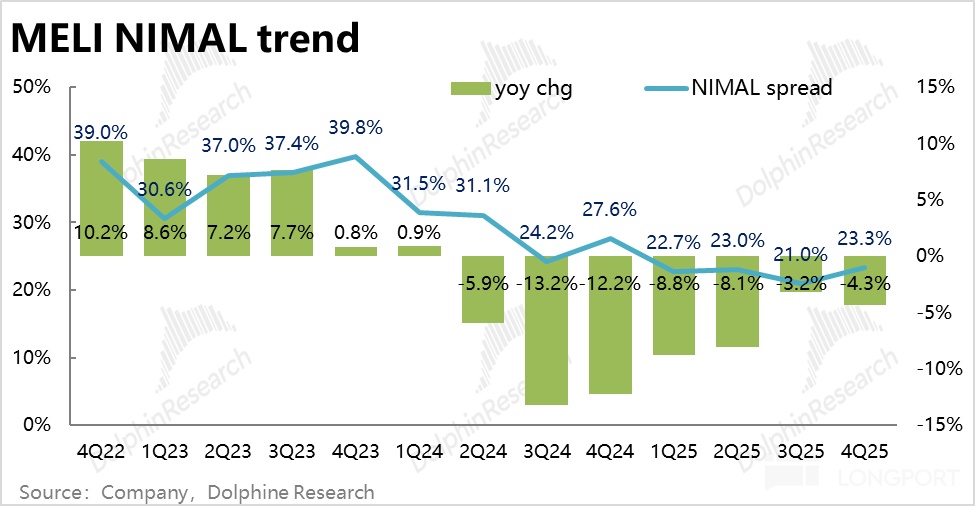

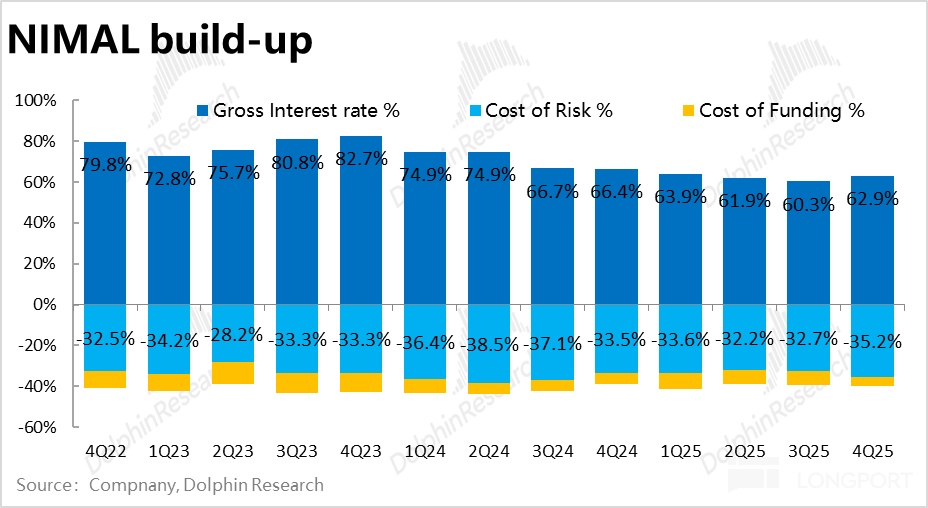

Correspondingly, NIMAL improved to 23.3% from 21% last quarter. This was supported by higher GP margin and a >2pct QoQ decline in funding costs, partially offset by higher provisions.On a YoY basis, NIMAL still fell by over 4pct, driven by mix shift toward lower-NIMAL credit cards.

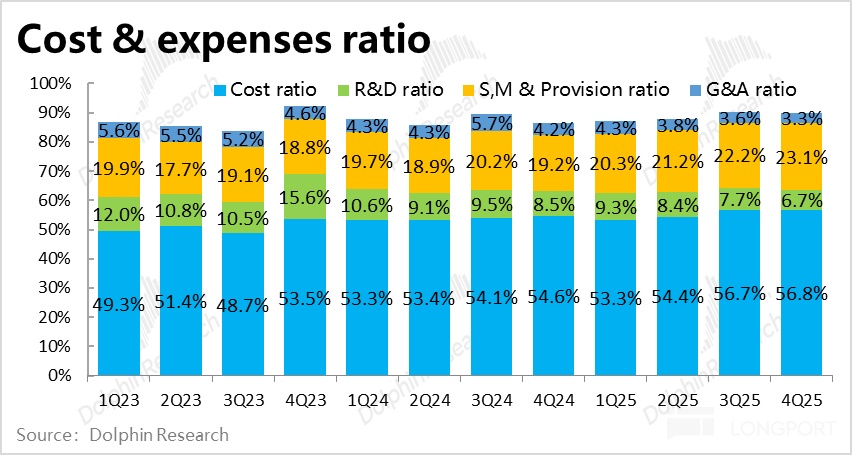

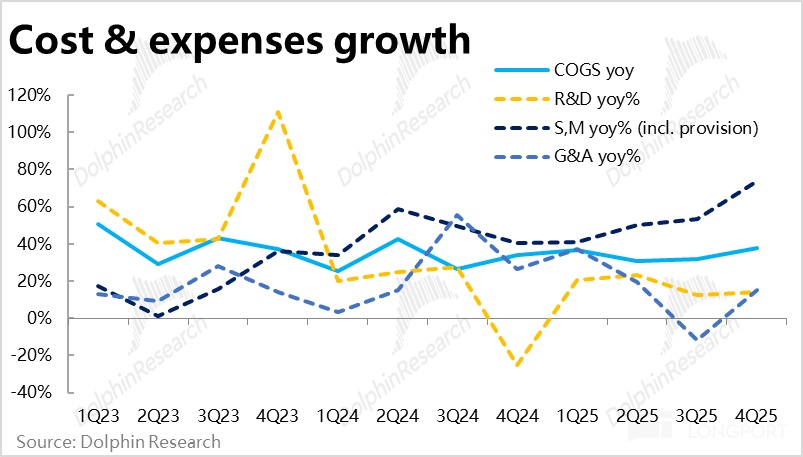

7) Why margins compressed: cost and opex: GPM was 43.2%, down over 2pct YoY. Lower free-shipping thresholds and weaker monetization in payments and credit are consistent with GPM pressure.Total operating expenses jumped ~50% YoY, accelerating vs. last quarter, outpacing revenue and running about 5% above Bloomberg estimates (partly due to a low base last year). The expense ratio rose by 1.2pct YoY.

Specifically, marketing and credit losses were the main drivers, up 55% YoY and ~97% YoY respectively, in line with loan growth. G&A and R&D remained disciplined, both growing around ~15% YoY.

Dolphin Research view:

1) MELI continues to prioritize long-term growth and competitive positioning, accepting near- to mid-term margin pressure.Execution appears effective: lowering free-shipping thresholds and improving fulfillment speed clearly lifted order growth and orders per buyer, enhancing ecommerce penetration and stickiness.

In credit, momentum remains strong with credit cards. Loan balances still grew about 90% YoY, and while NIMAL is lower YoY due to mix, GP margin and NIMAL show signs of stabilization QoQ.

Management noted credit cards typically reach NIMAL breakeven after the initial 12–18 months, and about 75% of card business in Brazil has achieved breakeven. As the card portfolio matures, NIMAL should recover further, unlocking credit profitability.Combining both legs, the strategy of sacrificing near-term profits for long-term growth remains validated, supporting growth and share gains.

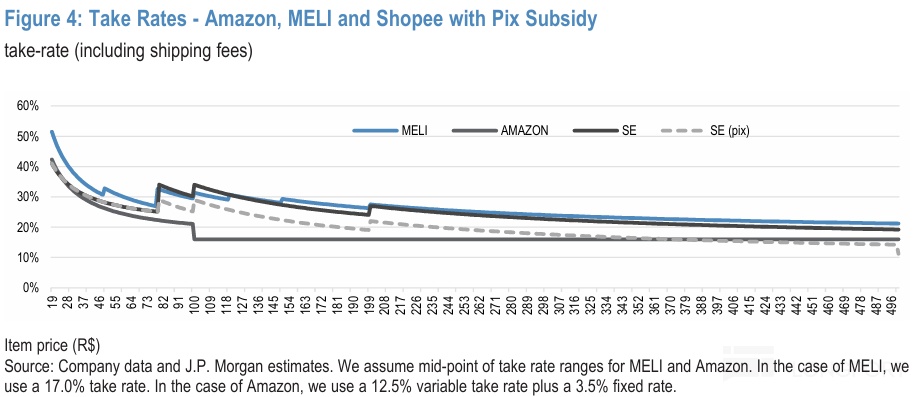

2) Competition remains intense in Brazil, MELI’s largest market, with Shopee, Temu, Shein, and AMZN all viewing LatAm — especially Brazil — as key growth markets. Recent moves suggest marginal easing in competitive intensity.

The notable change: Shopee has raised monetization in Brazil — a) personal seller service fees per order from R$5 to R$7 (+40%); b) commission curve for corporate sellers adjusted, with higher rates for R$80–R$300 price bands.Post-adjustment, Shopee’s blended commission in Brazil is roughly on par with MELI’s and both are among the higher in the industry. AMZN remains lower locally to chase share.

Strategically, Shopee’s successive monetization hikes imply shifting from aggressive share-grab toward profitability. This should alleviate pressure on MELI and help lift ecommerce margins in Brazil.That said, the landscape will also depend on Temu, Shein, and AMZN — each slightly behind in share but significant — so competition may not necessarily ease. (Per research, MELI holds ~40% share in Brazil, Shopee ~15%, with the other three around ~10% each.)

3) Valuation: per Dolphin Research’s prior deep-dive, under a conservative earnings path, applying 20x PE to 2030 profit and discounting back to 2025 yields a fair value range of ~$2,400–$2,500. That was ~30% upside vs. pre-earnings.

However, MELI’s valuation relies heavily on long-term growth. With ecommerce still investing in logistics and infrastructure, and credit in a rapid expansion phase, neither pillar is in a full profit-harvest. On current-year metrics, MELI trades at over 40x PE.We see durable long-term potential given MELI’s breadth in LatAm, but in a global market dominated by the AI narrative and a more conservative bias, MELI’s rich near-term valuation could remain under pressure.

Net-net, the quarter showed no unexpected fundamental weakness. The post-market drop likely ties to the call; stay tuned for our transcript.

Detailed review below:

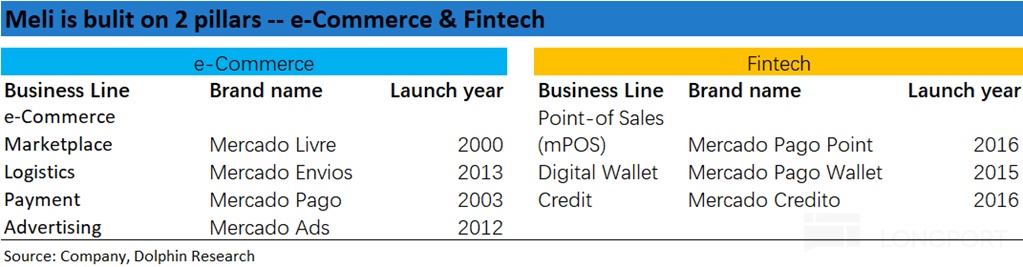

I. Mercado’s biz. mix

MercadoLibre, one of LatAm’s largest internet firms, operates two main segments: ecommerce and financial services. Based on reporting disclosures, we outline key components for context.

1) Ecommerce

Ecommerce revenue breaks into service revenue and product sales. Product sales reflect MELI’s 1P business, while service revenue reflects the 3P marketplace — merchant commissions, fulfillment, ads, payments, etc.

2) Financial

Financial revenue includes financial services, credit, and product sales. Financial product sales are small, mainly POS hardware.Financial services revenue reflects payments and digital wallet, monetized primarily via payment fees.Credit revenue is interest income from loans to consumers and merchants, currently driven by merchant loans, consumer loans, and credit cards.

II. Ecommerce: logistics efficiency drives growth

1) Shipping subsidies accelerate GMV

Core ecommerce GMV rose nearly 37% YoY in USD, up sharply from 28% last quarter and above market expectations.While FX was a major tailwind, constant-currency GMV growth still accelerated by ~2pct, indicating stronger organic momentum.

Ex-FX order metrics confirm this: total orders rose 43% YoY, about 4pct faster vs. last quarter. Since late 2022, order growth climbed from ~10% to 40%+, highlighting faster intrinsic growth on logistics improvements and user expansion.

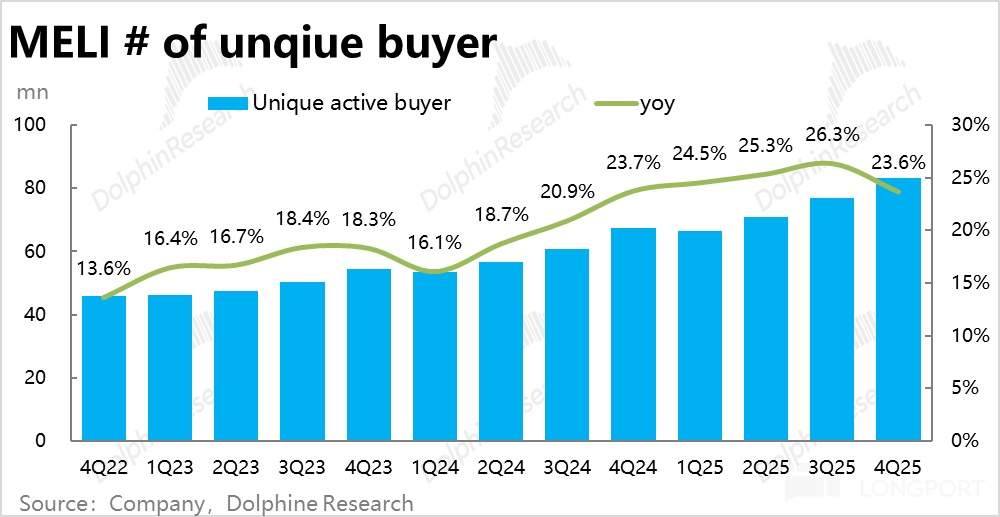

From a customer view, active buyers grew 23.6% YoY, still robust but marginally slower vs. last quarter.By contrast, orders per buyer hit 9, up 16% YoY — a new high since late 2022 — indicating that lower free-shipping thresholds and better fulfillment lifted purchase frequency more than user growth.

2) 1P outperforms; 3P monetization slows with subsidies

Commerce revenue reached ~$4.98bn (+40% YoY), accelerating alongside GMV but mainly FX-aided. Ex-FX, growth was 37%, down about 1pct vs. last quarter.

1P product sales grew over 70% YoY, outpacing the segment. Management emphasized 1P as a strategic focus, with investments in order automation, supply expansion, and supermarket margin improvement.3P service revenue rose ~32% YoY, with a 3P take rate of 20.1%. The YoY uplift further slowed to only 0.6pct (a new low), reflecting lower free-shipping thresholds and profit-sharing to drive growth and share gains.

III. Financial: payments steady, credit strong

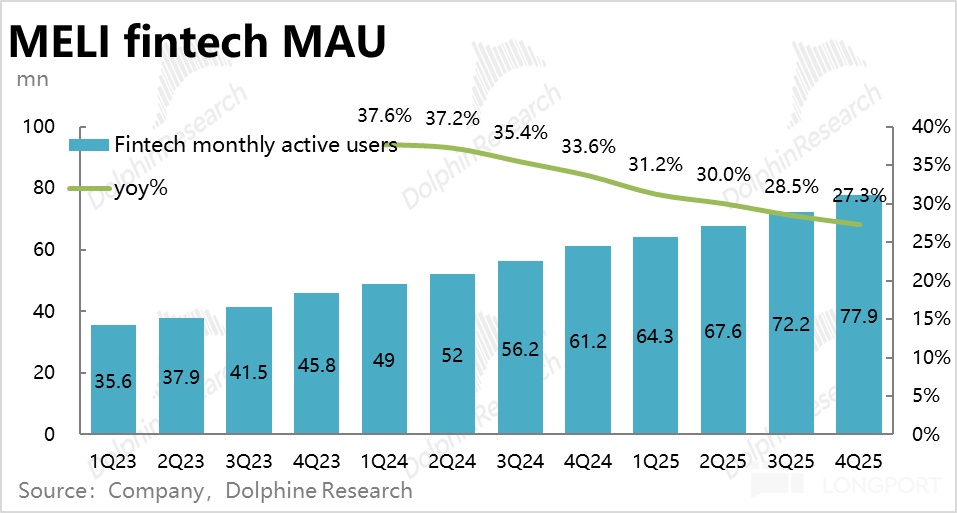

MELI's primary financial KPI, monthly active financial users, reached 77.9mn, net adds of 5.7mn QoQ, the highest single-quarter net adds on record.User expansion in the financial segment remained healthy.

1) Ecommerce ecosystem supports TPV growth

In payments, TPV rose 42% YoY, faster vs. last quarter but largely FX-driven. Payment order count grew about 35.5% YoY, slightly slower sequentially.

Non-acquiring TPV (e.g., digital wallet) grew ~64%, while acquiring TPV grew ~33%. Within acquiring, off-platform TPV rose 32% YoY, while on-platform accelerated to 36%, a rare inversion driven by stronger on-platform commerce growth.Financial services revenue rose 33% YoY, but growth decelerated as fee rates continued to trend down.

Overall, payments growth was broadly steady.

2) Credit remains strong; NIMAL warming

Loans outstanding reached $11.0bn (+90% YoY), maintaining rapid growth.Per the company’s breakdown, all four loan categories accelerated vs. last quarter, with credit cards still the strongest at ~115% YoY.

Avg. loan size rose ~47% YoY, while loan accounts rose ~30% YoY. The main driver is larger average balances rather than accounts.Credit-related revenue was $1.85bn (+77% YoY), with acceleration. Avg. loan GP margin ticked up from ~60% to ~63%, consistent with seasonal strength in Q4 rates.

NIMAL improved to 23.3% from 21% QoQ. Beyond higher GP margin, funding costs fell by over 2pct QoQ, partially offset by higher provisions.YoY, NIMAL declined by over 4pct due to mix shift toward lower-NIMAL credit cards, which is expected.

IV. Overall results: solid growth, margin pressure

With both commerce and credit performing well, MELI’s total revenue rose nearly 45% YoY to $8.76bn, a meaningful acceleration QoQ and about 3pct above Bloomberg consensus.Topline performance was strong.

Similar to last quarter, growth is supported by lower free-shipping thresholds, ongoing logistics investments, and elevated marketing, leaving margins under pressure.

Specifically, OPM was 10.1%, down more than 3pct YoY and slightly below consensus. Despite revenue beating by ~3pct, OP was approx. $890mn (+~8% YoY), only slightly above expectations.

On costs and expenses, GPM was 43.2%, down over 2pct YoY. While MELI does not disclose segment GPM, the lower free-shipping threshold and weaker monetization in payments and credit explain GPM pressure.Total opex surged ~50% YoY, accelerating vs. last quarter and outpacing revenue, about 5% above Bloomberg estimates. The expense ratio rose by 1.2pct YoY.

Marketing and credit losses were the primary drivers, up 55% YoY and ~97% YoY. G&A and R&D were restrained, both around ~15% YoY, indicating discipline in non-core internal expenses.

<End of text>

Dolphin Research historical [MELI] coverage:

Earnings reviews:

2025.10.30 Review: 'Meli: Profit miss? Likely just pre-victory 'growing pains''

2025.10.30 Call transcript: 'Mercado (Trans): Optimizing for long-term value over short-term profit'

2025.8.5 Call transcript: 'Mercado (Trans): No plan to cut free-shipping thresholds in other markets for now'

2025.8.5 Review: 'Growth vs. margin? The 'LatAm Alibaba' Mercado's choice'

Deep coverage:

2025-07-10 'Mercado: The 'LatAm Alibaba' and its gradual path to a $100bn market cap'

2025-09-16 'LatAm 'Alibaba' MELI: 'Pseudo' commerce, 'real' lending?'

2025-10-17 'LatAm Alibaba Mercado: Alibaba's 'face', Amazon's 'guts'?'

Risk disclosure and statement: Dolphin Research disclaimer and general disclosure

The copyright of this article belongs to the original author/organization.

The views expressed herein are solely those of the author and do not reflect the stance of the platform. The content is intended for investment reference purposes only and shall not be considered as investment advice. Please contact us if you have any questions or suggestions regarding the content services provided by the platform.