Morgan Stanley: Broadcom $Broadcom(AVGO.US)

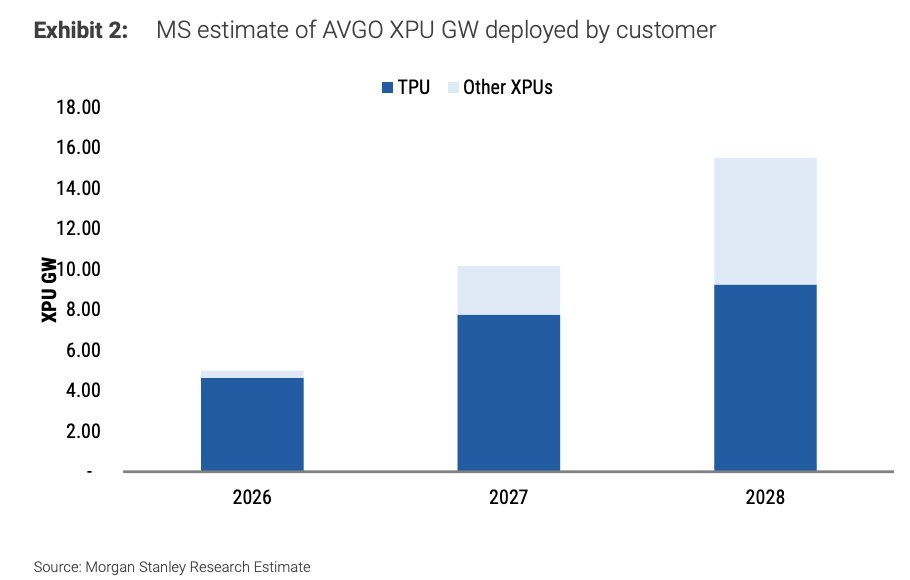

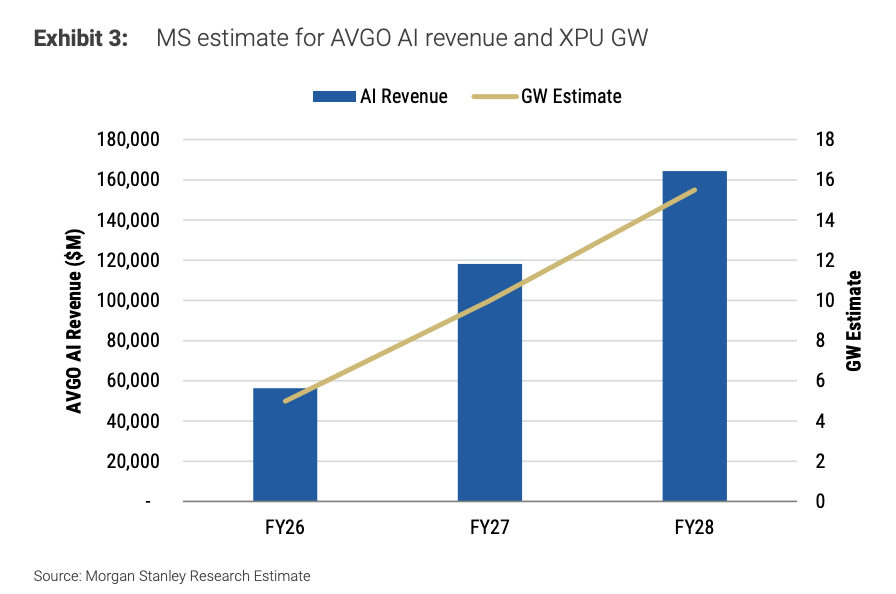

> Projected Dominance: Morgan Stanley expects Broadcom to retain a ~80% majority share of Google TPUs over time, backed by its advantages in High Bandwidth Memory (HBM) supply, advanced packaging execution, and sheer platform scale.> AI Revenue Projections: Morgan Stanley expects Broadcom to remain a core AI winner and a close number 2 to NVIDIA. They estimate Broadcom will generate roughly $120 billion in AI revenue for FY27, with TPU-related deployments accounting for approximately $80 billion (75% of a 10GW total deployment).> Growth Diversification: By FY28, TPU is expected to drop to 60% of Broadcom's AI revenue mix, not because TPU is slowing down, but because a pipeline of alternative Custom ASIC customers will begin ramping up in the second half of 2027.> Advanced Packaging Risks: Bears are assuming a massive, rapid ramp for competing 2nm TPUs using Intel's EMIB advanced packaging. However, Morgan Stanley’s Taiwan team indicates that EMIB remains highly uncertain and complex for Google's required standards, leaving TSMC's CoWoS as the more dependable mechanism—an area where Broadcom holds strong system qualification and execution history.> The HBM Supply Advantage: A key reason competing solutions will struggle to achieve expected cost reductions is High Bandwidth Memory (HBM) procurement. While buying HBM off the shelf has become very expensive due to tight open-market pricing, Broadcom has already secured its supply under previously locked-in, contractually agreed rates.

The copyright of this article belongs to the original author/organization.

The views expressed herein are solely those of the author and do not reflect the stance of the platform. The content is intended for investment reference purposes only and shall not be considered as investment advice. Please contact us if you have any questions or suggestions regarding the content services provided by the platform.

Post your comment

No Comments