Samsung reported an explosive 250 fold increase on 2026Q2 operating profit. Revenue jumps 130% YOY and increases 28% quarterly to US$119 billion. HBM delivers the strongest sales by amounting to >60% of the revenue. The stocks rise 4% after this report but quickly drop to closed at 1% lower. It seems that this wonderful report still fails to stop the rout in the Korean stock market. Analysts expect this to continue until most of the investors who use leverage to invest are being flushed out. Is Korean memory stock uninvest able or investor just waiting to do bottom fishing?$SK Hynix(SKHY.US)

SK Hynix

SKHY149.00017.52% ( +22.210 )

Share your thoughts

Write something you'd like to share with our community...

- D

The oil price situation is erratic. One day it is up and the next it is down. This is why risk management is essential.

☕️ [Task Coins Giveaway] Daily Market Talk — Microsoft Rips 8%, Meta Cracks 10%

Microsoft and Meta reported minutes apart last night and the market split them right down the middle: MSFT ripped about 8% after hours as Azure grew 43%, while Meta's free cash flow collapsed to $784 ...

- D

What a week it has been. This is what sentiment is. At the top, everyone wants to buy. Down here, no one wants to buy. But prices are much cheaper here. Thats how trends are also. Not many has the courage to do things using their own thought process.

☕️ [Task Coins Giveaway] Daily Market Talk — Microsoft Rips 8%, Meta Cracks 10%

Microsoft and Meta reported minutes apart last night and the market split them right down the middle: MSFT ripped about 8% after hours as Azure grew 43%, while Meta's free cash flow collapsed to $784 ...

- N

Standard Chartered Bank Hongkong stocks profit rose. Though AI trading becomes the trend, I wonder on the businesses purposes.

Korea stocks fall is a concern.

I wonder on the jobless percentage on Thursday report.

Today is 30 July and why is there a report for 31 July on the employment cost?

However, the oil price increases.

☕️ [Task Coins Giveaway] Daily Market Talk — Microsoft Rips 8%, Meta Cracks 10%

Microsoft and Meta reported minutes apart last night and the market split them right down the middle: MSFT ripped about 8% after hours as Azure grew 43%, while Meta's free cash flow collapsed to $784 ...

- D

Shaky times because it’s earning season and plenty of geo uncertainties. DYODD well

☕️ [Task Coins Giveaway] Daily Market Talk — Microsoft Rips 8%, Meta Cracks 10%

Microsoft and Meta reported minutes apart last night and the market split them right down the middle: MSFT ripped about 8% after hours as Azure grew 43%, while Meta's free cash flow collapsed to $784 ...

- R

Markets are entering a high-volatility window with economic data, earnings, and geopolitical headlines all colliding. I’m keeping more cash on hand and waiting for higher-conviction setups instead of reacting to every headline.

☕️ [Task Coins Giveaway] Daily Market Talk — Microsoft Rips 8%, Meta Cracks 10%

Microsoft and Meta reported minutes apart last night and the market split them right down the middle: MSFT ripped about 8% after hours as Azure grew 43%, while Meta's free cash flow collapsed to $784 ...

- F

REITs and bank stock investors should also take note with recent Fed rate decision and his tone.

Chairman Kevin Warsh struck a clearly hawkish tone after the meeting:

He repeatedly said that the inflation is "still too high" and he will not accept inflation staying above 2%

He also pushed back firmly against market hopes for rate cuts and ruled out any plan to raise or soften the inflation target

Barclays has called the current outcome a "hawkish pause" and this will likely make markets price in a higher chance of rate hikes ahead.

Hence bad for REITs and good for bank stocks.

☕️ [Task Coins Giveaway] Daily Market Talk — Microsoft Rips 8%, Meta Cracks 10%

Microsoft and Meta reported minutes apart last night and the market split them right down the middle: MSFT ripped about 8% after hours as Azure grew 43%, while Meta's free cash flow collapsed to $784 ...

- C

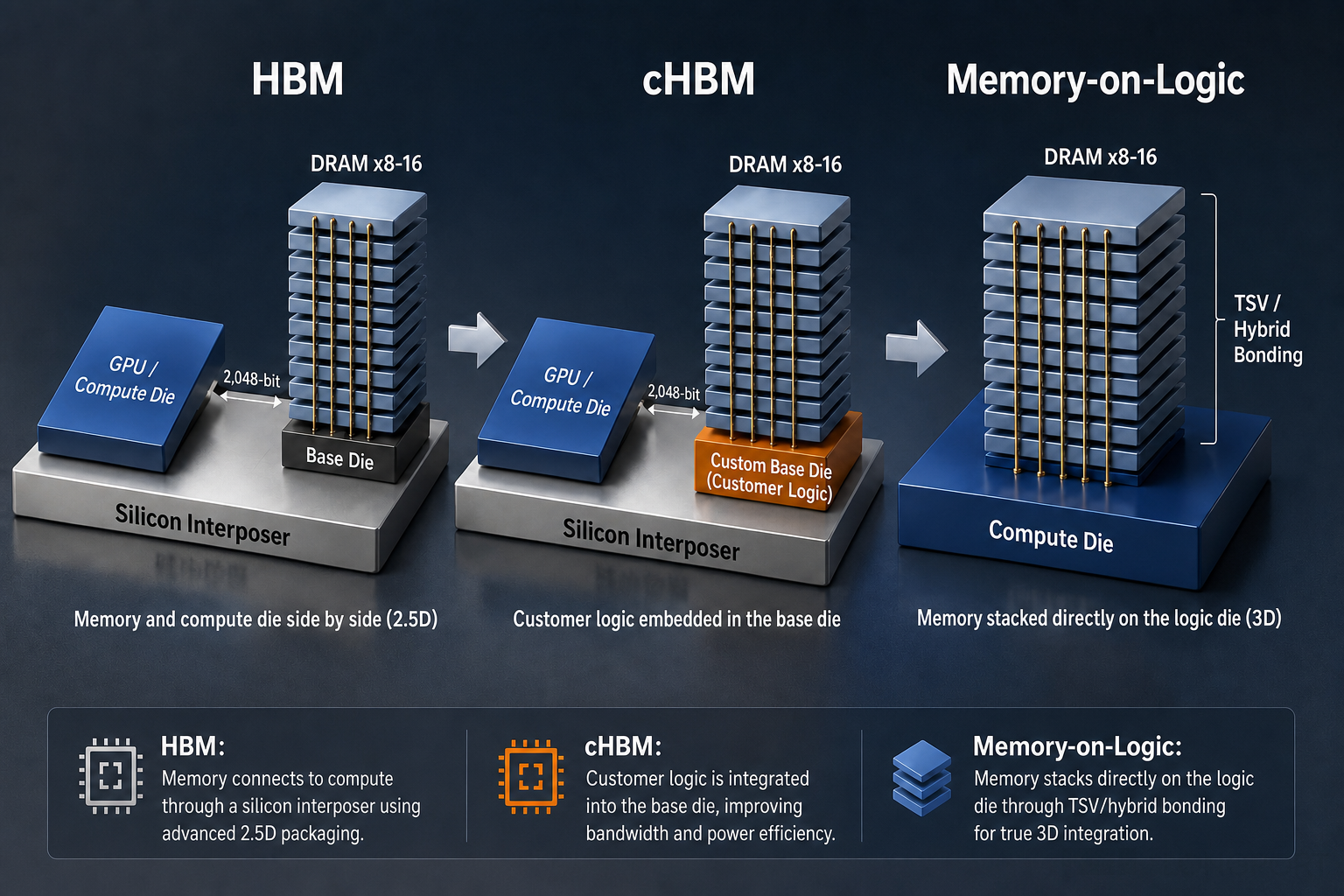

SK hynix: After Standard HBM Expansion, Is Customization the Next Act?

HBM is evolving from a standardized memory product into a customer-specific, tightly integrated component. From HBM4 process shifts to custom HBM and memory-on-logic, this transition could reshape the memory industry’s cyclicality and valuation.

- C

☕️ [Task Coins Giveaway] Daily Market Talk — Microsoft Rips 8%, Meta Cracks 10%

Microsoft and Meta reported minutes apart last night and the market split them right down the middle: MSFT ripped about 8% after hours as Azure grew 43%, while Meta's free cash flow collapsed to $784 ...

Earnings Week: MSFT, META, AAPL & AMZN Report - B

$XL2CSOPHYNIX(07709.HK) I'm here

- A

- SK Hynix 2Q26

- $52.8B revenue in 2Q26 (+51% q/q, +257% y/y); new ATH; 83% GM up from 79%in 1Q- DRAM and NAND demand projected to grow mid-20% and high teens in ‘26- Blended DRAM ASP affected by shipment delays for some high-value products and product-mix changes- 2026 CapEx expected in the high KRW 40T range ($30B+)- LTAs completed with around 10 customers; Typical LTA duration around 5 yrs- HBM4 mass production shipments started in 2Q26; ramp planned in 2H26- HBM4 yield and quality already approaching mature HBM3E levels- HBM4E samples delivered to major customers in 1H26Source: Sravan Kundojjala

- S

Similar spaceX 🚀situation...we have only this pool of investors daily ..it hard to maximise when scattered

SK hynix: Memory Rally Over; Are LTAs the Safe Harbor?

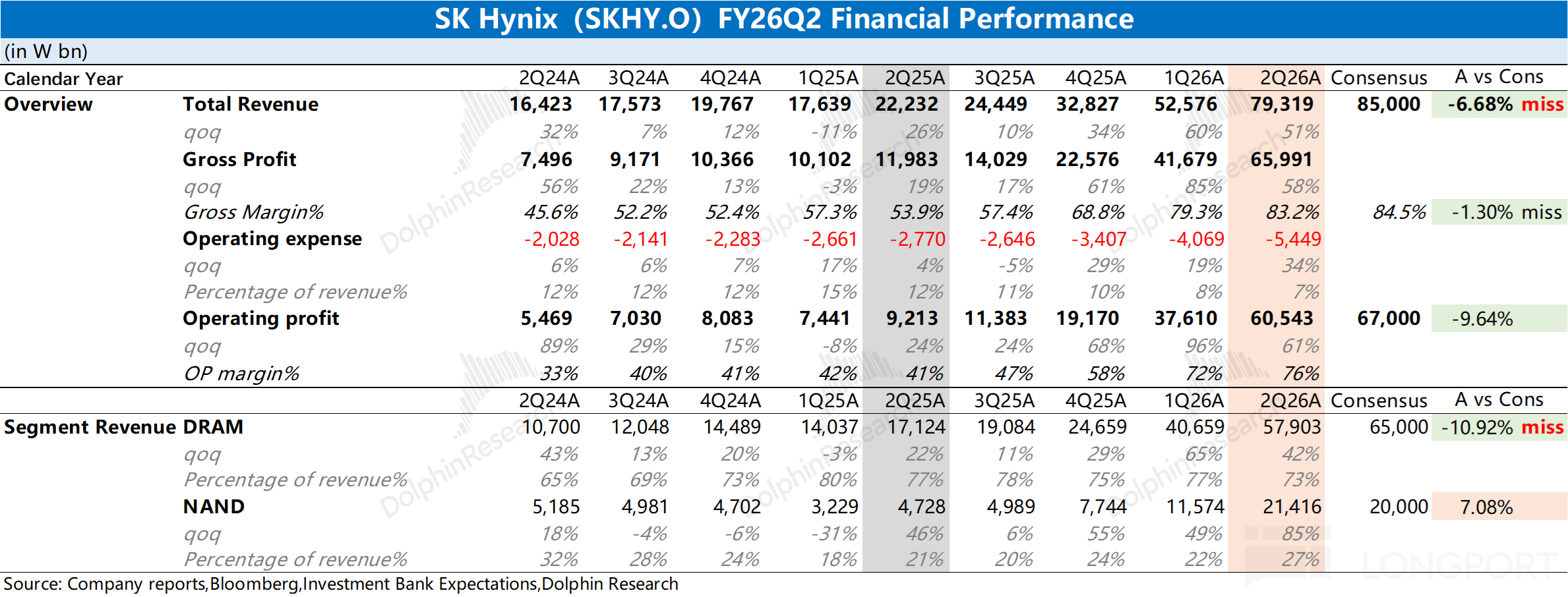

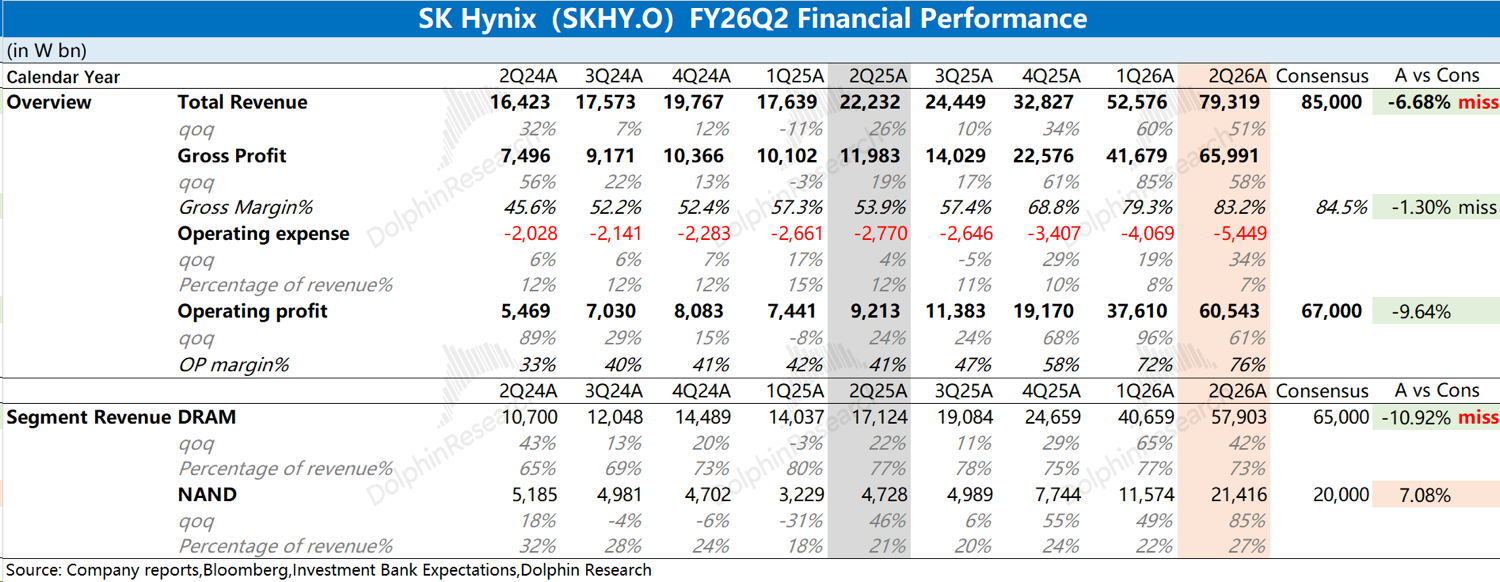

SK hynix released its FY26 Q2 results (quarter ended Jun 2026) after the U.S. close, in the morning of Jul 29 (Beijing time). Key takeaways: 1) Core metrics: revenue of KRW 79 tn (+51% QoQ), below consensus (KRW 85 tn).

Growth was driven by both DRAM and NAND, with memory price hikes the largest contributor. GPM was 83%, below street (84–85%)...

+7

- F

So let me get this straight,

1. First Hynix ER came shit then memory crashes, bears made fun of bulls2. Then during the call it went back, so bulls made fun of bears3. Ah, KOSPI as expected started the day crashing and now bears partying again.I told you a million times don't worry about them right now. The memory and chips trend is gone, money is in energy and healthcare and even effing coca cola is going. Focus on what's moving now, not what's behind. - D

SK hynix: Memory Rally Over; Are LTAs the Safe Harbor?

SK hynix released its FY26 Q2 results (quarter ended Jun 2026) after the U.S. close, in the morning of Jul 29 (Beijing time). Key takeaways: 1) Core metrics: revenue of KRW 79 tn (+51% QoQ), below consensus (KRW 85 tn).

Growth was driven by both DRAM and NAND, with memory price hikes the largest contributor. GPM was 83%, below street (84–85%)...

SK HynixFinancial Analysis - A

A TON OF THINGS HAPPENED IN THE STOCK MARKET TODAY.

Here's a full recap:1. SK Hynix $SK Hynix(SKHY.US) reported Q2’26 revenue of $54.6B vs $57.7B expected, up 257% YoY and 51% QoQ, while operating profit came in at $41.6B vs $44.2B expected, up 557% YoY. Operating margin hit a record 76%, with gross margin at 83% and EBITDA of $44.4B, or an 81% margin. Pricing remained extremely strong, with DRAM ASP up ~30% QoQ and NAND ASP up mid-50% QoQ, while Q3 guidance calls for DRAM bit growth of about 10% QoQ and NAND bit growth in the low-single digits. SK Hynix also said HBM4 shipments began in Q2 with a full ramp planned in 2H, while HBM4E samples were supplied to a major customer in 1H. Net profit surged to $64.6B, boosted by $43.5B of investment-asset gains, meaning net income exceeded revenue due to $42.8B of non-operating profit.2. The Trump administration is proposing a change that would allow the FAA to waive certain environmental review requirements for commercial launch sites, rocket launches, and spacecraft reentries, according to WSJ. The move could speed up approvals as annual launches and reentries are expected to rise from 214 this fiscal year to more than 500 over the next decade. SpaceX $SpaceX(SPCX.US), Rocket Lab $Rocket Lab(RKLB.US), Blue Origin, and Stoke Space could benefit, though the proposal still has to go through public comment.3. U.S. Central Command said IRGC forces launched multiple ballistic missiles from Iran today in an attempted surprise attack on U.S. forces stationed in the Middle East. CENTCOM said all Iranian missiles were successfully intercepted and that U.S. forces remain on high alert and ready to respond. Oil was up 5% after hours on the news even though it went down 4% today on earlier reports that Egypt, Qatar, and Pakistan were working to bring back the original MOU between the US and Iran. No updates on that original MOU coming back are in place yet, but the attacks after hours showcased further escalation. 4. The top 10 most active options today by contracts traded were $NVIDIA(NVDA.US) with 2.4M contracts, $Tesla(TSLA.US) with 1.7M contracts, $Apple(AAPL.US) with 1.0M contracts, $Intel(INTC.US) with 820K contracts, $SpaceX(SPCX.US) with 750K contracts, $Micron Tech(MU.US) with 737K contracts, $AMD(AMD.US) with 573K contracts, $SoFi Tech(SOFI.US) with 558K contracts, $Amazon(AMZN.US) with 495K contracts, and $Palantir Tech(PLTR.US) with 461K contracts.5. Nvidia $NVIDIA(NVDA.US) CEO Jensen Huang reportedly met with Commerce Secretary Howard Lutnick as Nvidia faces growing scrutiny over China chip exports, per Axios. The meeting comes while the Commerce Department investigates potential violations tied to Nvidia’s Blackwell shipments to China, though the details of their discussion were not disclosed. Huang is also meeting with lawmakers from both parties as Washington prepares a broader AI framework covering advanced models, open-source AI, and China, expected by August 1.6. OpenAI and Anthropic are reportedly lobbying the Trump administration ahead of an August 1 deadline for deciding which frontier AI models should face government evaluation, per The Information. The companies want rival models from players like Meta $Meta Platforms(META.US) and SpaceXAI included as well. Qualifying models could be subject to review at least 30 days before release if they raise cybersecurity or national-security concerns. OpenAI and Anthropic are also warning about Chinese open-source models allegedly built in part using their outputs, citing privacy, IP theft, and cybersecurity risks.7. Moonshot AI is reportedly looking for more Nvidia $NVIDIA(NVDA.US) Blackwell chips as it discusses Kimi K4, a model expected to be significantly larger than its 2.8T-parameter Kimi K3, per The Information. K3 was reportedly trained partly in China using Blackwell chips accessed through multiple Chinese cloud providers, with Moonshot linking separate 8-chip servers across providers and data centers because no single provider had enough capacity. Inference is now another constraint, with Moonshot pausing new subscriptions within 48 hours of launch as demand overwhelmed capacity. The company reportedly uses Nvidia H20 chips for inference and recommends at least 64 chips to host K3. The report also says Alibaba trained its 2.4T-parameter Qwen3.8-Max using Nvidia chips, including Blackwell.8. OpenAI CEO Sam Altman said a compute oversupply could emerge within 2 years if AI models become efficient enough to handle most tasks while human attention becomes the real bottleneck. He also said oversupply risk could rise if the industry hits a scaling wall and costs stop falling, making additional compute less economically attractive.9. Bloom Energy $Bloom Energy(BE.US) crushed Q2’26 earnings, with revenue rising 166% YoY to $1.07B vs $827.6M expected and adjusted EPS jumping 680% YoY to $0.78 vs $0.41 expected. Product revenue surged 215.4% YoY to $935.4M, while adjusted gross margin expanded 604 bps to 34.3%. Bloom also raised FY26 guidance, now expecting revenue of $3.9B–$4.2B vs $3.73B expected and adjusted EPS of $2.55–$2.85 vs $2.16 expected. Management said all major U.S. hyperscalers, plus over a dozen neoclouds, AI labs, and data center operators, have approved Bloom’s power solutions for AI factories, calling Bloom a new standard for AI onsite power.10. ADP data shows U.S. private hiring has slowed for the fifth straight week, averaging just 15,000 jobs per week through July 11, less than half the 35,750 weekly pace seen in early May. At the same time, Visa $Visa(V.US) is reportedly cutting 7% of its workforce, or about 2,600 jobs, adding to signs that labor-market momentum is cooling.11. Retail investors are leaning heavily into Big Tech upside, with call options on U.S. Big Tech stocks now making up roughly 55% of all new retail options positions on a 20-day average basis, near the highest level on record. This tracks newly opened call positions, not total volume, making it a clearer read on directional retail bets. The figure is up 10 percentage points since the late-March market bottom, compared with a 57% peak during the 2020 pandemic rebound and a 35% low during the 2022 bear market.12. Every component in the semiconductor index $SOX is now trading below its 50-day moving average for the first time since April 2025, a sharp reversal from early June when all 30 members were above that level. The SOX is down 18.9% so far in July, putting it on pace for its worst monthly decline since 2008, and now trades 11% below its 50-day moving average, the widest gap since March 30. Despite the pullback, semis remain up 63% YTD. Meanwhile, the semiconductor ETF $SMH has seen $1.3B of outflows month-to-date, tracking toward its second-largest monthly outflow on record.WALL STREET IS THE GREATEST SHOW ON EARTH.Source: amit

- D

SK hynix (Trans): LTAs include deposits; capacity adds won't cause immediate oversupply

The following is Dolphin Research's Trans of $SK Hynix(SKHY.US) FY26 Q2 earnings call. It compiles key points from management's discussion.

Core highlights recap begins with shareholder returns. Cash generation has reached a record high, aided by the sale of the Kioxia stake and the ADR offering.The company is assessing multiple incremental return-of-capital options. Due to regulatory and procedural constraints tied to the ADR offering, it cannot yet disclose the form, size, or timing. It aims to update the market within the year... SK HynixConference Minutes

SK HynixConference Minutes - D

SK Hynix 2Q26 First Take: results disappointed despite an expected sharp memory upcycle. Revenue and GPM both came in below street expectations.

The shortfall mainly stemmed from DRAM, which accounts for over 70% of revenue. DRAM rose 42% QoQ, with shipments up high single digits (~8%) and ASP up ~30% QoQ.

Commodity DRAM prices in Q2 climbed more than 50% QoQ at the market level. SK Hynix’s ASP increase was materially weaker.

This softer ASP reflects a capacity pivot toward HBM. With smaller exposure to commodity DRAM, recent price hikes contributed less than the market had hoped.

The current memory upcycle has been driven by AI capex. With Meta leasing compute, the K3 model in focus, and Anthropic’s ARR growth slowing, investors have started to question the durability of CSP capex, prompting a pullback across the AI pricing chain, including memory.

The market remains divided on the cycle’s path. Some houses expect memory prices to start rolling over in 2H27, while others argue that LTAs signed by memory majors could delay the downcycle.

A slower slope of price gains is now broadly consensus. Street expectations for QoQ price moves in 2026 Q1/Q2/Q3 are roughly 90% → 55% → 15%. From a second-derivative lens, the surge phase has passed.

In sum, the print was weak, and investors do not expect sustainably outsized profits (e.g., 80%+ GPM). More important than this quarter is the trajectory of LTAs and whether they support steady earnings over the next few years.

The -10% after-hours drop directly reflected the miss. The subsequent rebound followed the company’s slide deck first officially confirming that LTAs include prepayments and other financial mechanisms, though no specific amounts were disclosed (Micron has disclosed prepayments and RPO).

The low valuation also embeds concern over future uncertainty. Clearer disclosures on order and price locks under LTAs would be key to restoring confidence in the multiple. For more updates, follow Dolphin Research’s upcoming commentary and Trans.$SK Hynix(SKHY.US)

- G

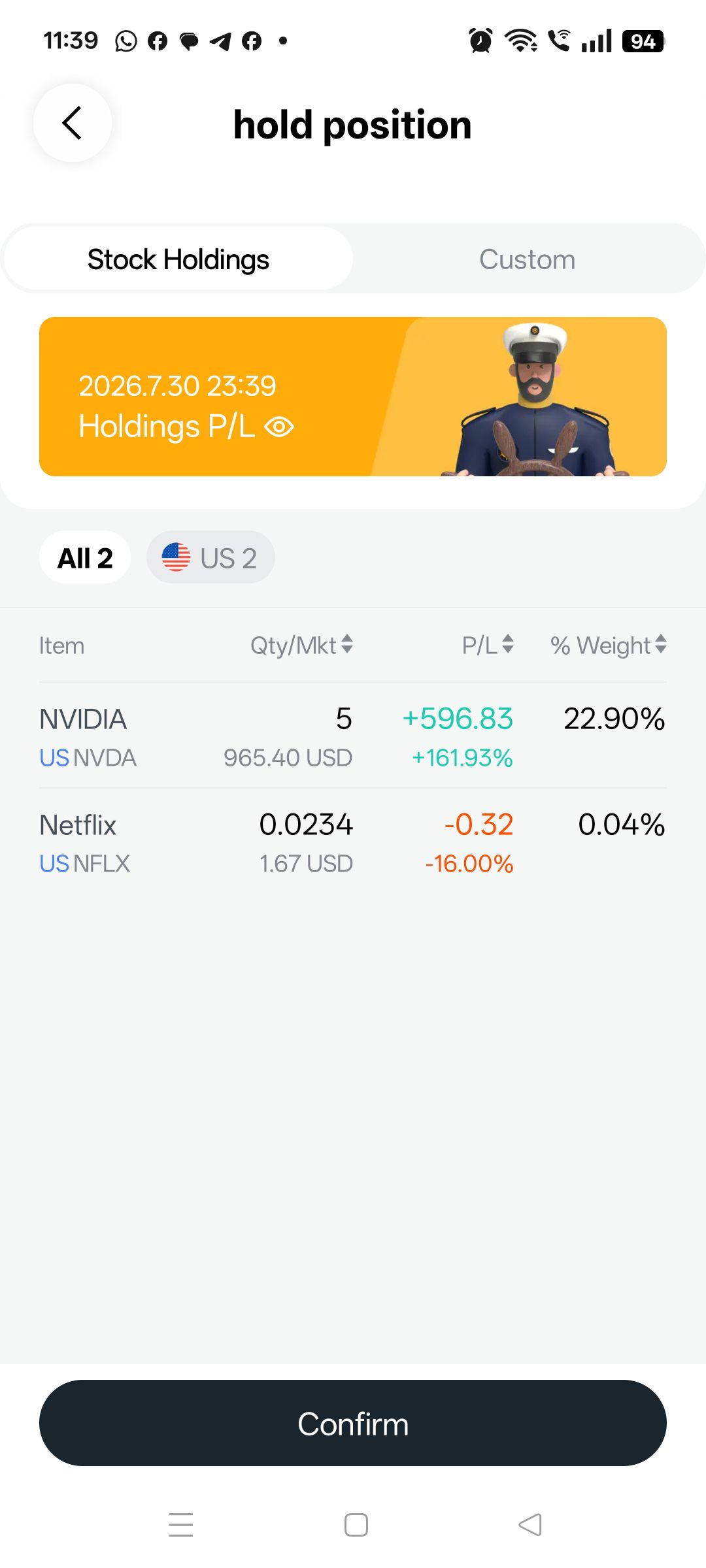

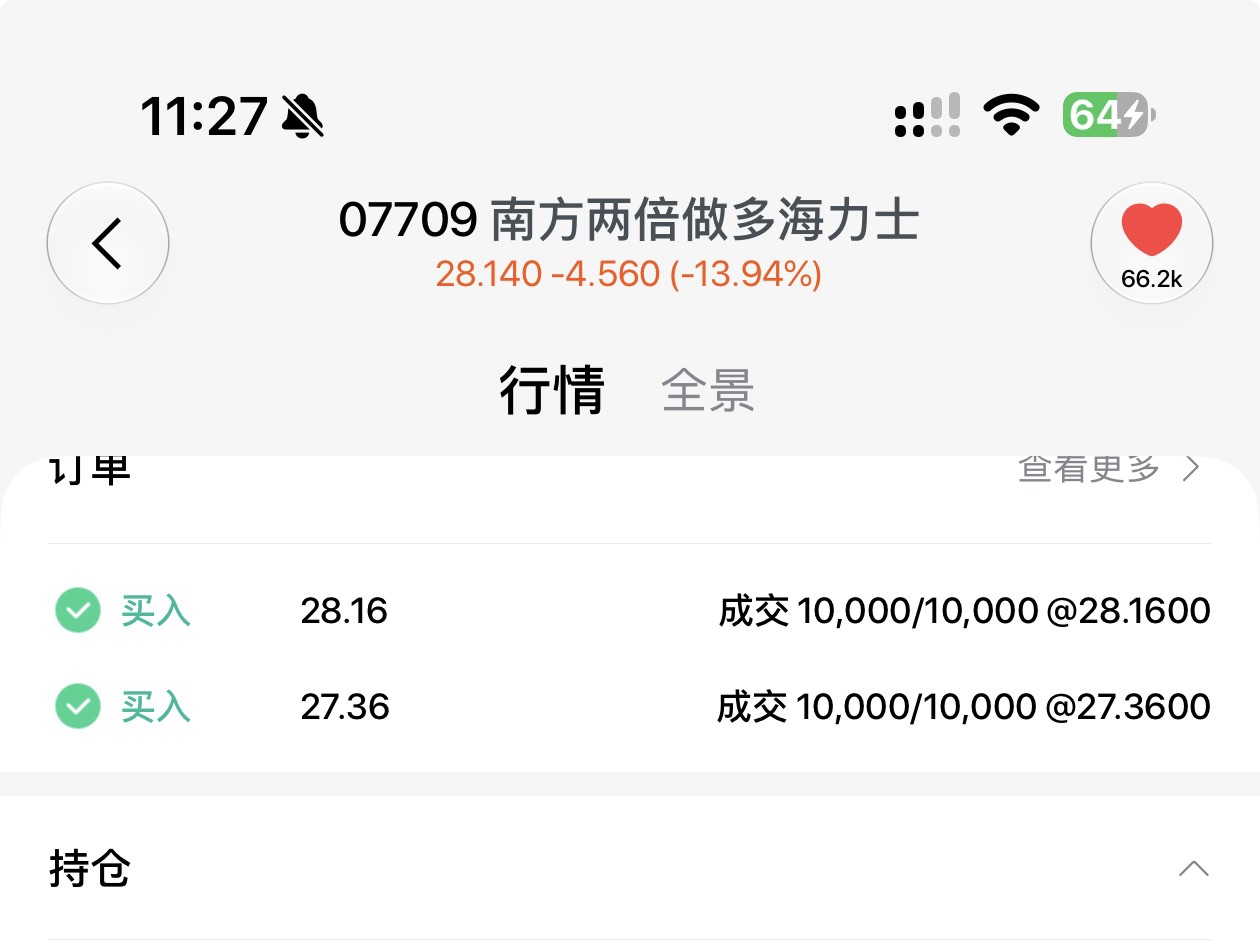

Kospi index has risen more than double since early 2025 (2399 at start of 2025 and 6023 as of 28 Jul), this is unprecended and an correction is expected.The rise of the index is caused retail investor leveraging on borrowed money which is not healthy. Kospi is very much consists of Skhynix and Samsung which were rocketed with their HBM product. Skhynix hold around 58% and Samsung 40% of market shares. To how low that the Kospi can go is anybody guess now. Currently, Skhynix ADR is cheaper than the IPO price of US$149, it might even get cheaper.$SK Hynix(SKHY.US)$NVIDIA(NVDA.US)$Netflix(NFLX.US)

Trade Showcase: Trade, Show & Earn Rewards!

Trade Showcase: Trade, Show & Earn Rewards! - H

🚨 Pre-market buzz!

$Sherwin Williams(SHW.US) $Core Scientific, Inc.(CORZ.US) $Welltower Op(WELL.US) $Coca Cola(KO.US) $Cadence Design(CDNS.US) $Oshkosh Truck(OSK.US) $Stryker(SYK.US) $American Tower(AMT.US) $Boeing(BA.US) $S&P Global(SPGI.US) $Hilton Worldwide(HLT.US) $Broadcom(AVGO.US) $Paypal(PYPL.US) $AMD(AMD.US) $Universal Health Service-B(UHS.US) $Intel(INTC.US) $Super Micro Computer(SMCI.US) $Celestica(CLS.US) $Rambus(RMBS.US) $SK Hynix(SKHY.US) $Western Digital(WDC.US) $Micron Tech(MU.US) $T1 Energy(TE.US) $Sandisk(SNDK.US) $Commvault Systm(CVLT.US) $Amkor Tech(AMKR.US) $Corning(GLW.US) $Replimune(REPL.US)

- F

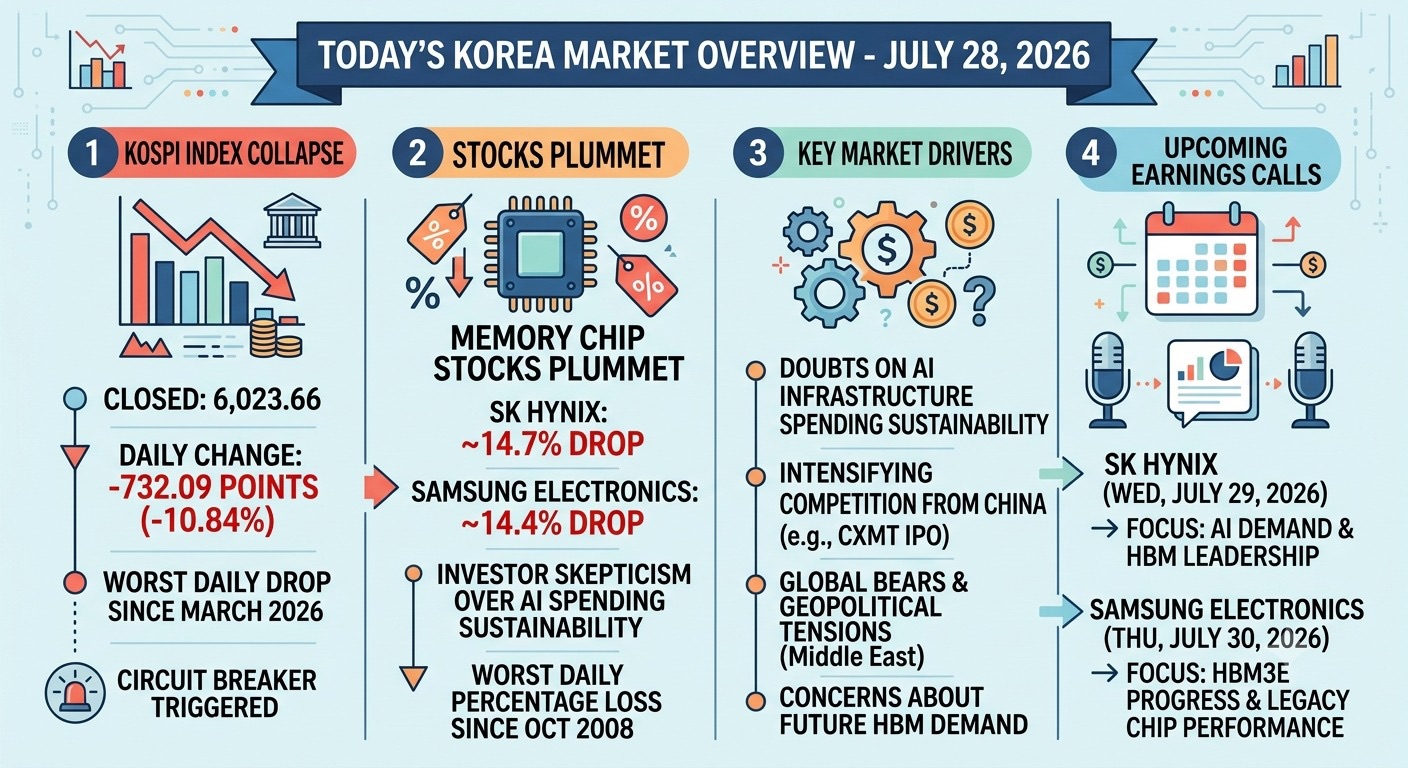

⏰ What’s Happened To Korea’s Market?

South Korea saw a historic sell‑off today( 28 July 2026). The KOSPI plunged -10.84% , its worst single day since March 2026.

Leading the crash: SK Hynix down 14.7% and Samsung Electronics down 14.4%, both posting record one‑day falls.

This sharp drop is driven by three big worries:

Doubts over whether heavy AI spending can keep up, geopolitical tensions and fast‑rising competition from China.

The fall also remind or signals a much more cautious outlook for the whole global memory sector.

Before rushing to “buy the dip,” remember: weakness in these giants may be a warning for memory stocks everywhere.

Key watchpoint: Both companies report earnings this week, their updates will decide if sentiment stabilises or worsens. Trade carefully and do your homework first.

$SK Hynix(SKHY.US)