Didi 1Q26 First Take: headline results were weak, with adj. EBITA under RMB 200 mn amid heavy investment.However, vs. expectations the print was better — domestic profit release far exceeded forecasts, and Intl growth was strong while losses came in slightly lower than expected (still sizable in absolute terms).

Breakdown:

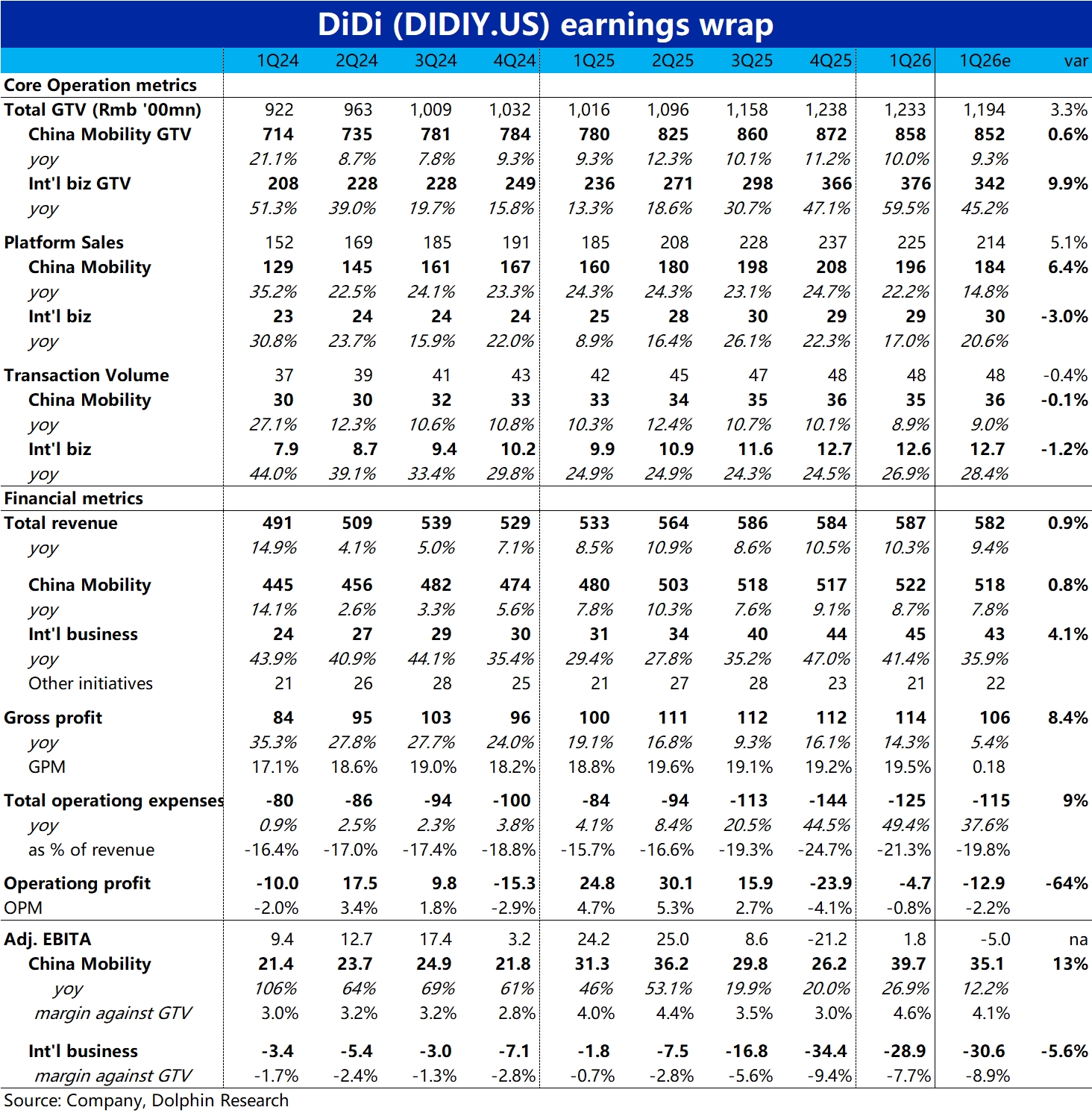

1) Domestic GTV rose 10% YoY, with growth easing QoQ but slightly above Bloomberg consensus; order growth showed a similar ~1ppt QoQ deceleration, indicating steady momentum.The standout was profit release, with domestic adj. EBITA near RMB 4 bn, well above the market's ~RMB 3.5 bn.Adj. EBITA margin was 4.6% on GTV, up 60bps YoY.

Domestic platform sales grew ~22% YoY, far outpacing GTV and revenue growth of ~10%.This implies a meaningful uplift in net take rate after driver revenue share and other direct costs, rising from 20.6% to 22.8%.

2) Intl was the highlight on growth, with GTV up 59% YoY; ex-FX, +49%, accelerating by over 10ppt QoQ.Orders rose 27% YoY, with only ~2ppt acceleration and well below GTV growth.Mix shifted toward higher-ticket food delivery, lifting GTV more than orders.

Beyond solid growth, Intl adj. EBITA loss was ~RMB 2.9 bn, still large but better than the market's ~RMB 3.1 bn loss estimate and Q4's RMB 3.4 bn.In other words, loss margin narrowed alongside strong growth.

3) Overall, domestic growth was steady while Intl growth was strong; domestic profit release expanded, and Intl losses narrowed.Company revenue maintained ~10% growth.Absolute profit was still under RMB 200 mn, but vs. the market's expected RMB 500 mn loss, this was a clear beat. $DiDi(DIDIY.US)

The copyright of this article belongs to the original author/organization.

The views expressed herein are solely those of the author and do not reflect the stance of the platform. The content is intended for investment reference purposes only and shall not be considered as investment advice. Please contact us if you have any questions or suggestions regarding the content services provided by the platform.