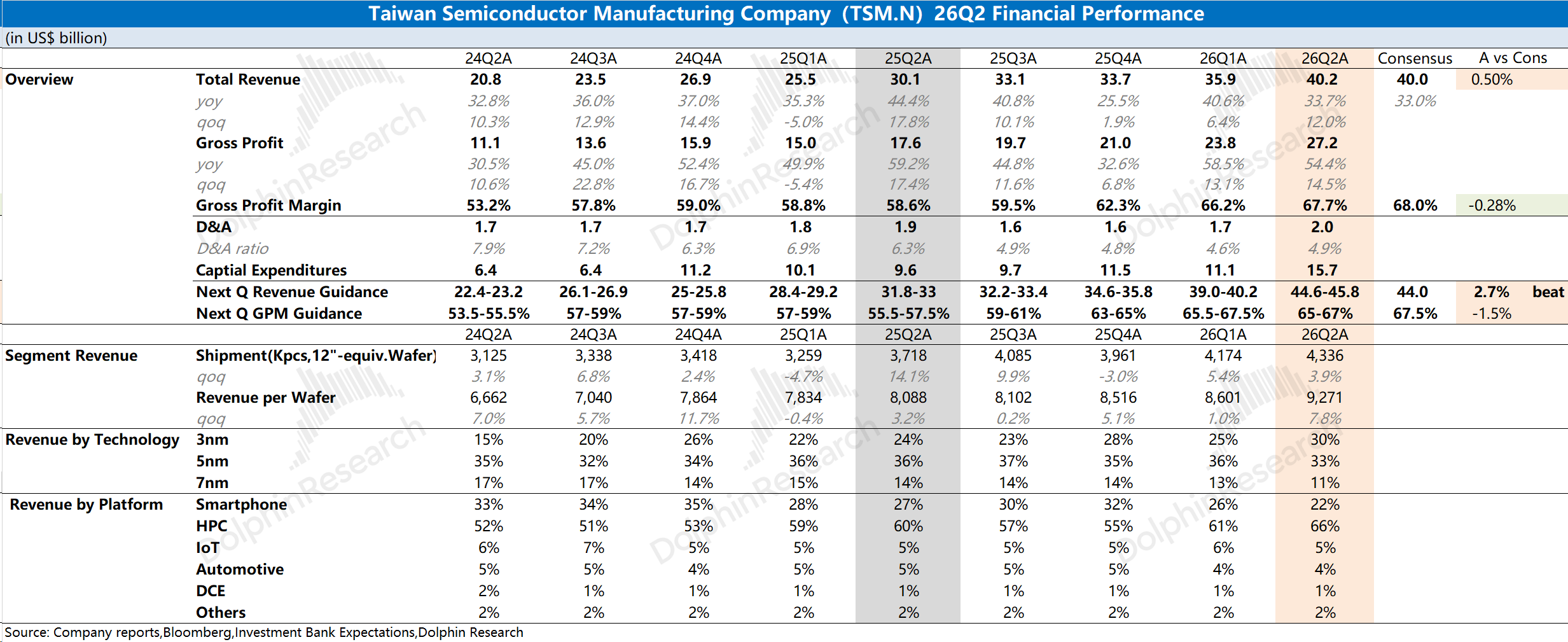

TSMC 26Q2 First Take: with the AI market in need of a confidence boost, this print is unlikely to satisfy. As the company discloses monthly ops data, revenue came in at $40.2bn, broadly in line with buy-side expectations (~$40bn).

Versus the top line, investors focused on gross margin. GPM was 67.7%, at the top end of guidance but slightly below raised buy-side expectations (some aggressive marks were 69%+).

Margins are still on an upward trend, driven by higher utilization and pricing. N5 and below have been running at >100% utilization, while rush orders lifted ASPs, with some orders carrying >50% premiums.

With fab loading tight, the company has more incentive to lift capex. Management raised capex to $60-64bn (from the higher end of $52-56bn), well above the Street at $58bn. This implies H2 capex of $33.2-37.2bn (+56%-75% YoY), aligning with ASML’s back-half-weighted revenue outlook.

On the outlook, next-quarter revenue is guided to $44.6-45.8bn, with GPM at 65%-67%. Since TSMC provided full-year growth guidance, the importance of next-quarter guidance is reduced. Management lifted the FY revenue growth target to 40% (vs. at least 30% prior), slightly above mainstream expectations (35%+).

Overall, the market had hoped for a more dazzling report to inject confidence into the AI supply chain, but the print and outlook did not deliver a big beat. Among the metrics, only capex clearly topped expectations, a relative positive for upstream equipment names such as ASML. For more, stay tuned for Dolphin Research’s follow-up take and transcript highlights. $Taiwan Semiconductor(TSM.US)

The copyright of this article belongs to the original author/organization.

The views expressed herein are solely those of the author and do not reflect the stance of the platform. The content is intended for investment reference purposes only and shall not be considered as investment advice. Please contact us if you have any questions or suggestions regarding the content services provided by the platform.