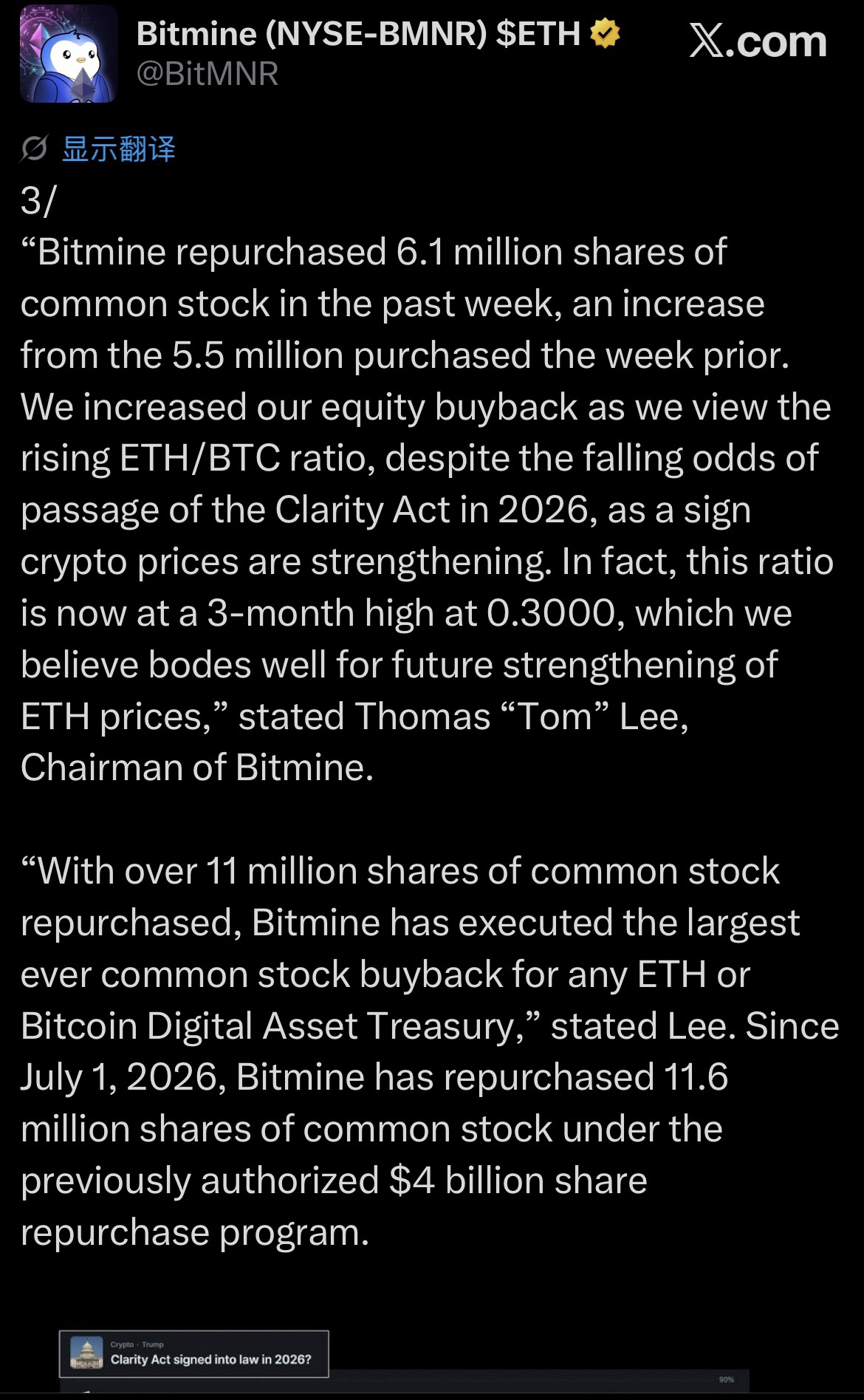

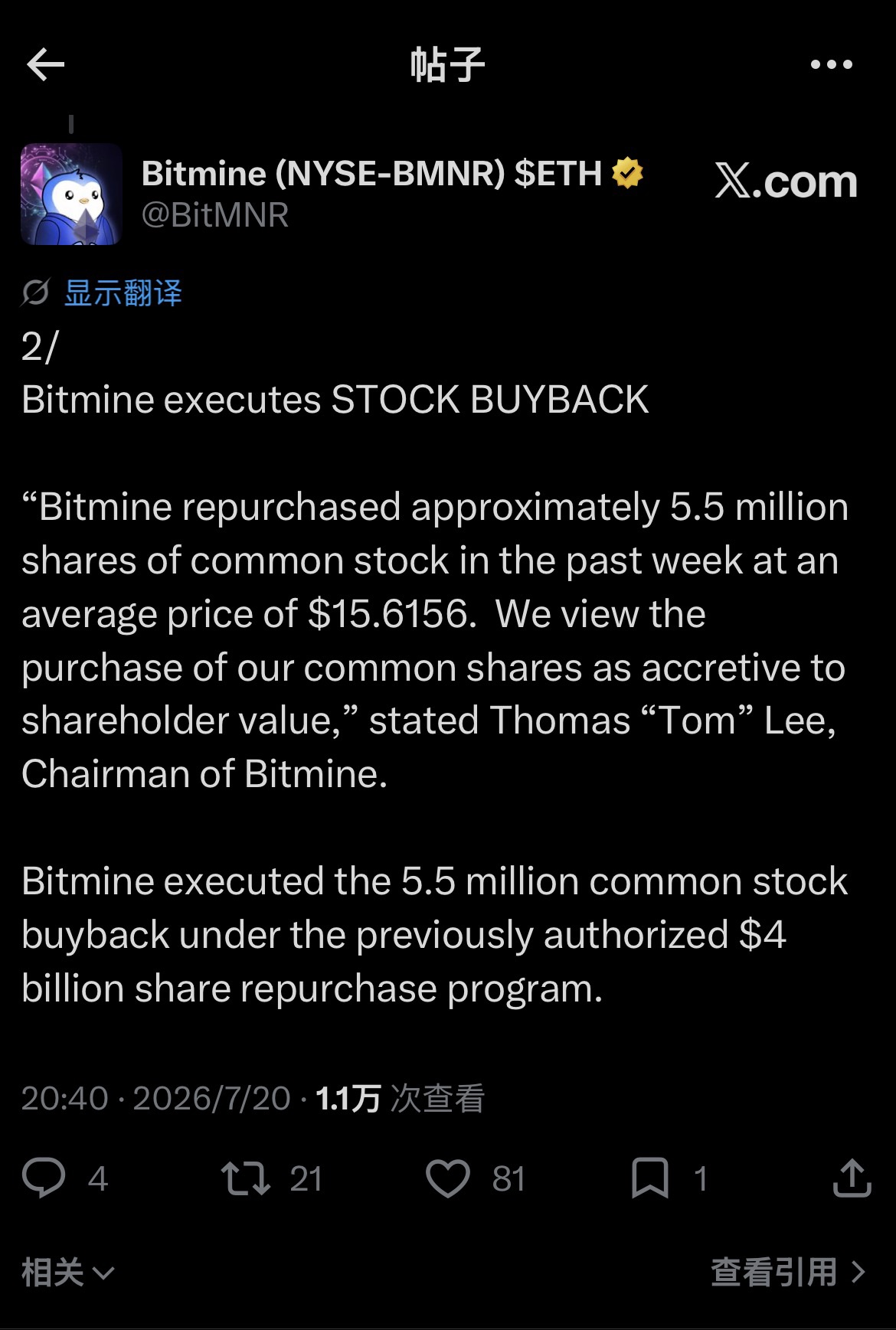

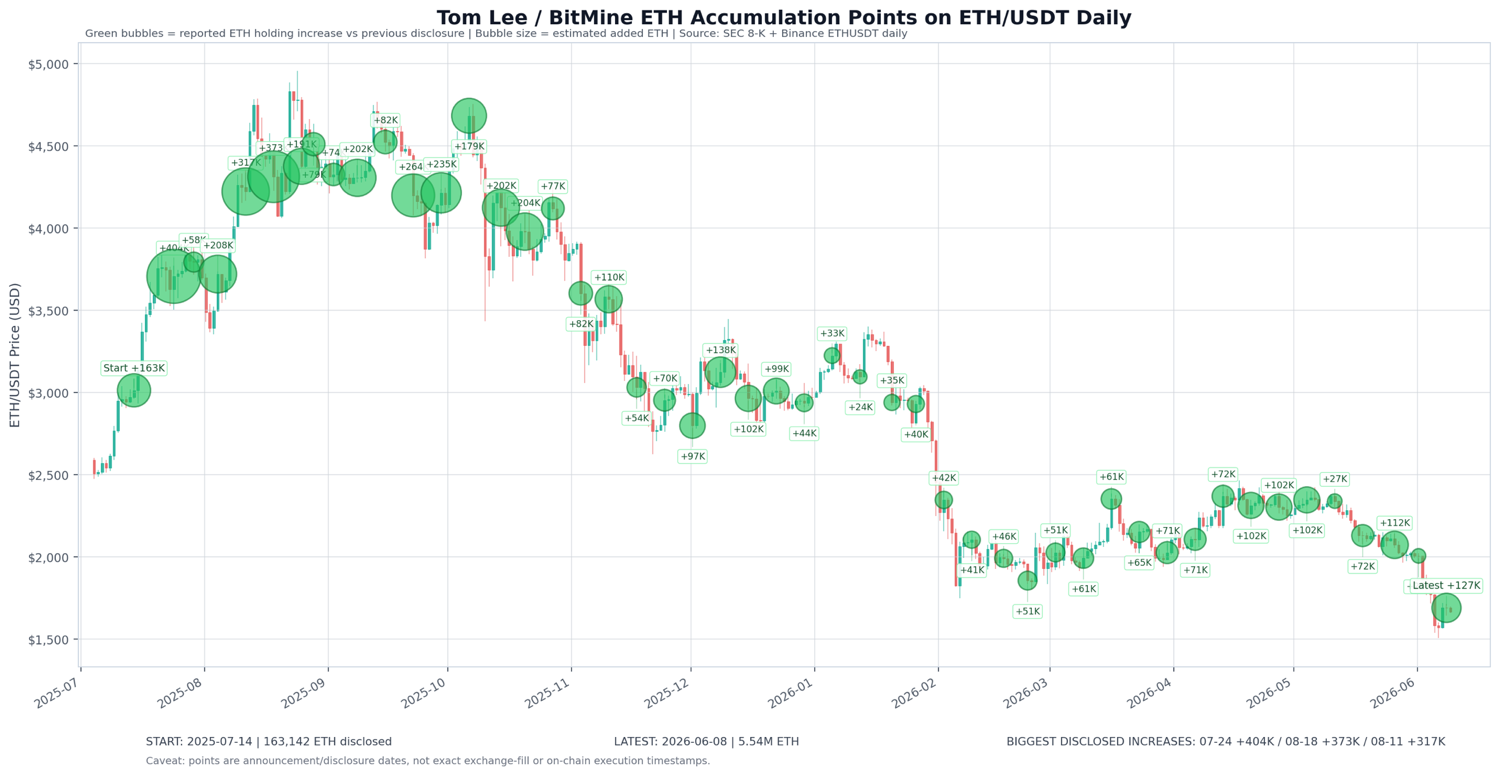

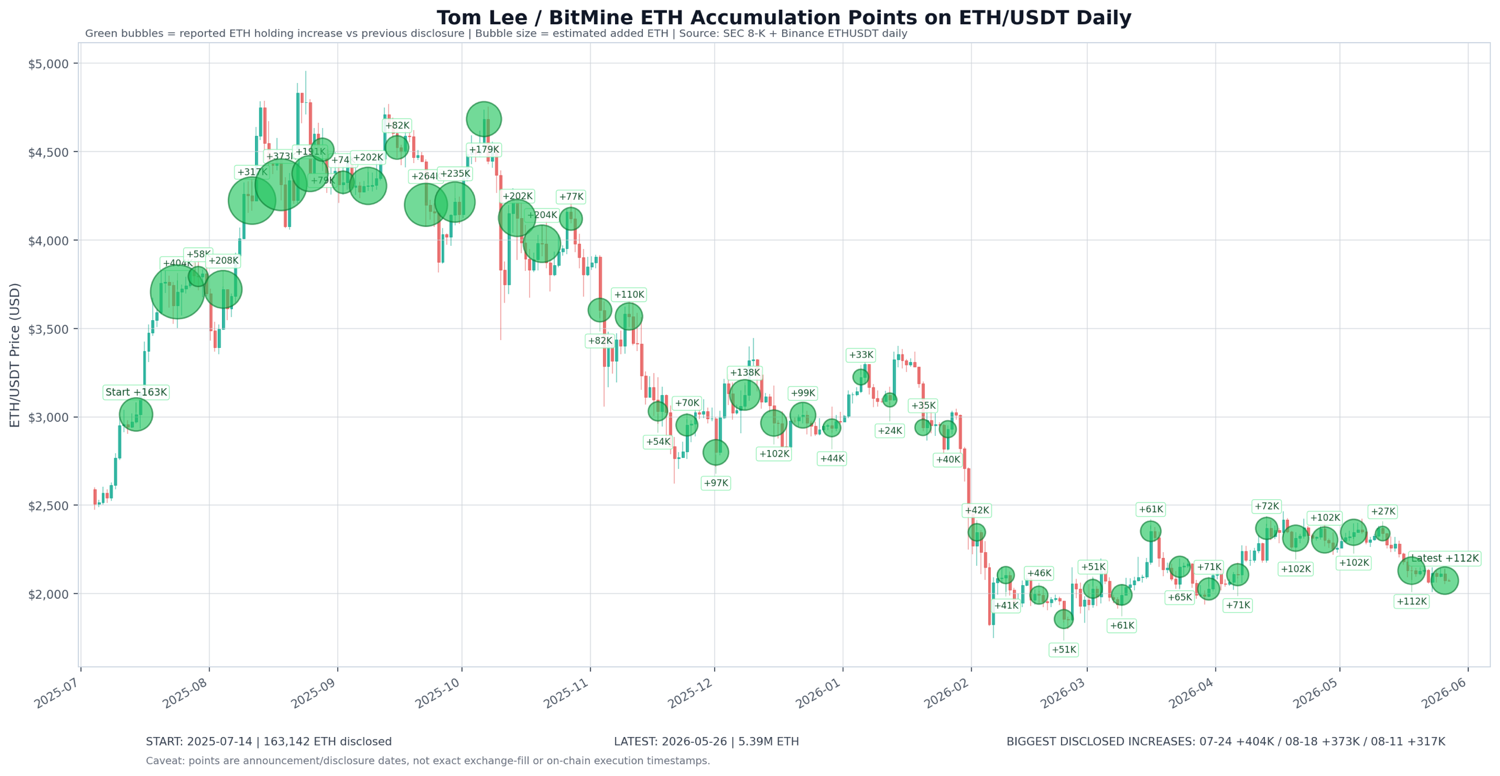

After the initial repurchase of 5.5 million shares, BMNR continued to repurchase another 6.1 million shares last week. mNAV is around 0.85, and ETH/BTC has rebounded to 0.03, a high point in nearly 3 months, with decent momentum.

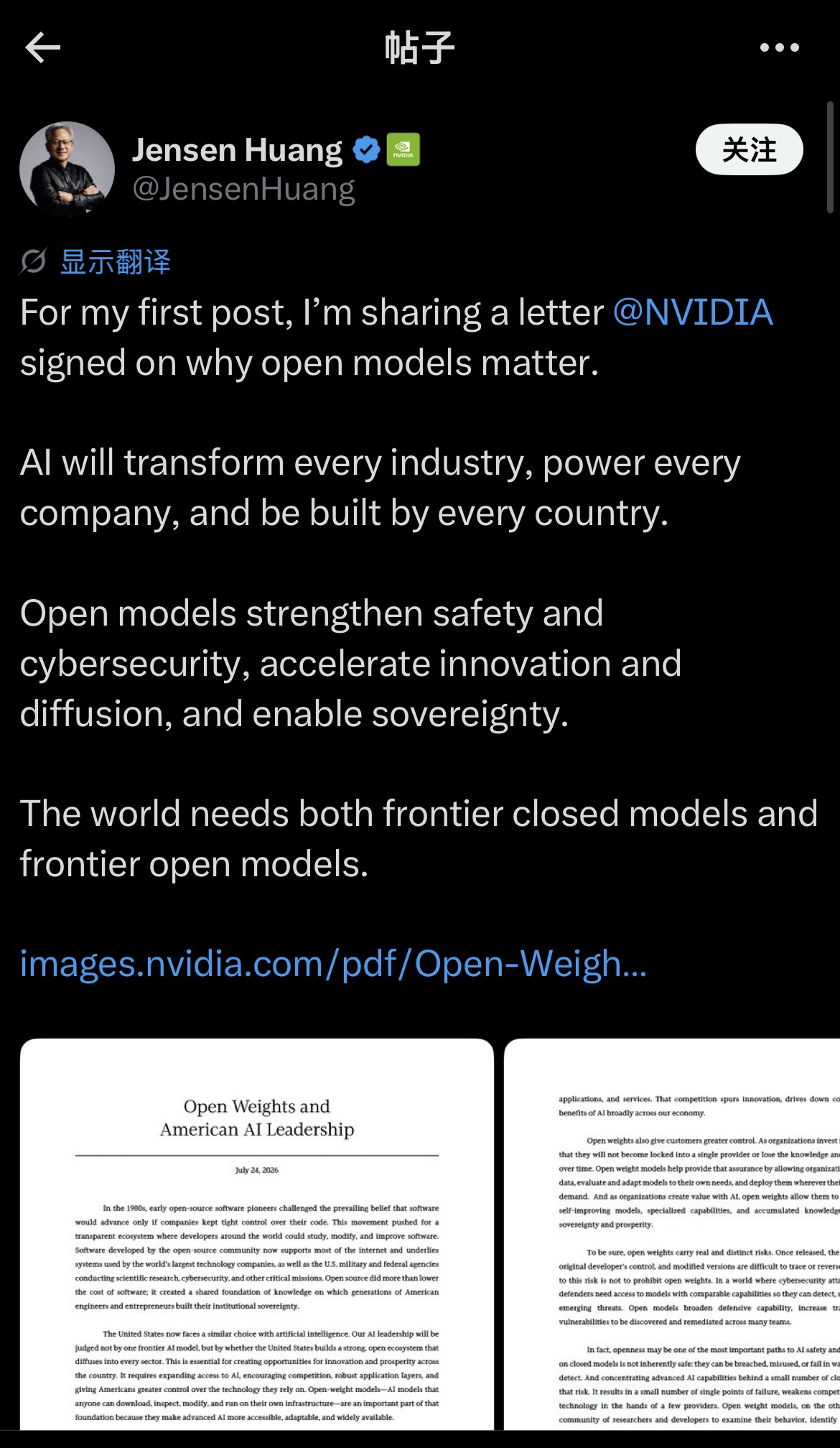

The biggest news yesterday was Huang Xiaoming opening an X account and posting his first tweet. An open letter initiated by a16z, jointly signed by NVIDIA, Microsoft, PLTR, PerplexityAI, Ollama, and other tech companies, explicitly advocates that "cutting-edge open-source models and cutting-edge closed-source models should coexist and develop."

Among so many companies, who didn't sign? Obviously Company A.

There is a data point: the weekly token share of Chinese open-source models used by US enterprises is approaching 60%. With open-source models accounting for such a large proportion of token consumption in US enterprises, if they are banned or restricted, enterprise costs will surge dramatically.

We previously discussed two paths for AI competition: model expansion and platform expansion. Now, enterprise AI adoption has entered the engineering era, with AI adoption in the enterprise market increasingly shifting to scenario-specific application models:

1) High-value scenarios continue to use high-value tokens from cutting-edge closed-source large models;

2) In high-frequency, low-complexity task scenarios, enterprises are increasingly favoring high cost-performance tokens (mostly from open-source models).

This trend is inevitable:

- For chip manufacturers, whether using which model, training and inference are required;

- For cloud providers, the more model choices offered to enterprise customers, the higher the gross margin;

- For deployment layers (such as PLTR) or application-oriented companies, there is naturally a stronger incentive to choose high cost-performance tokens.

The co-signing enterprises on this open letter basically fall into these three categories, so behind the open letter lies extremely strong commercial demands and huge commercial value. In other words, the attitude of O and A making money while blaming customers is increasingly causing dissatisfaction among customers and the industry, and the competition is becoming increasingly fierce.

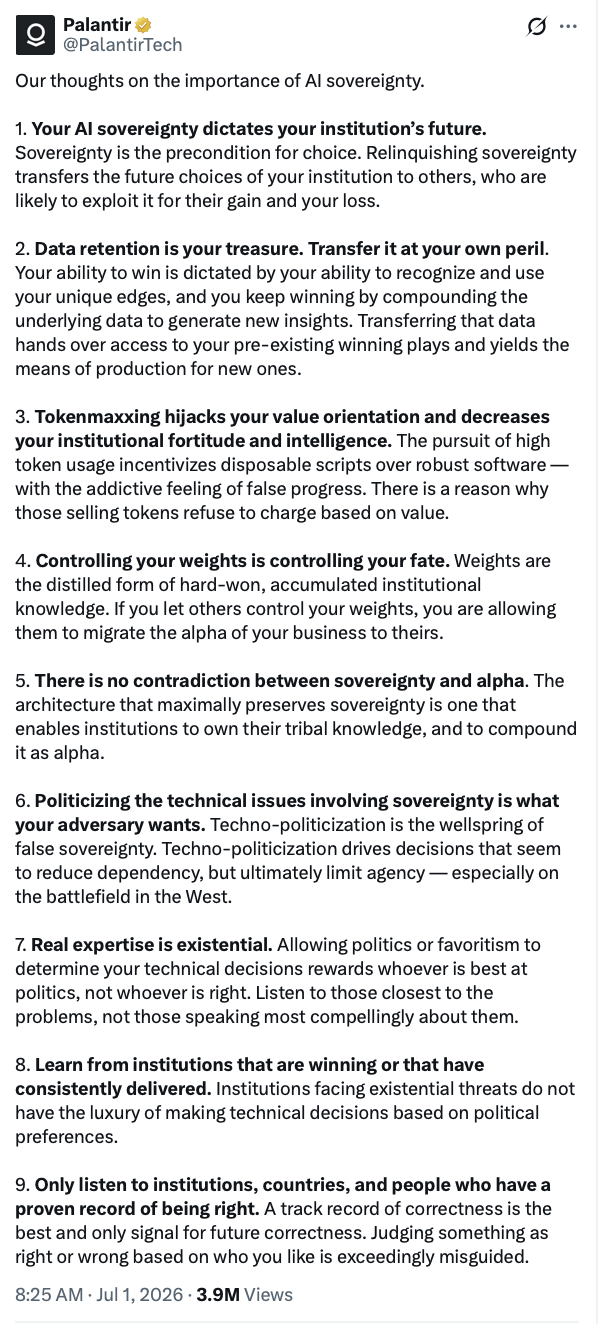

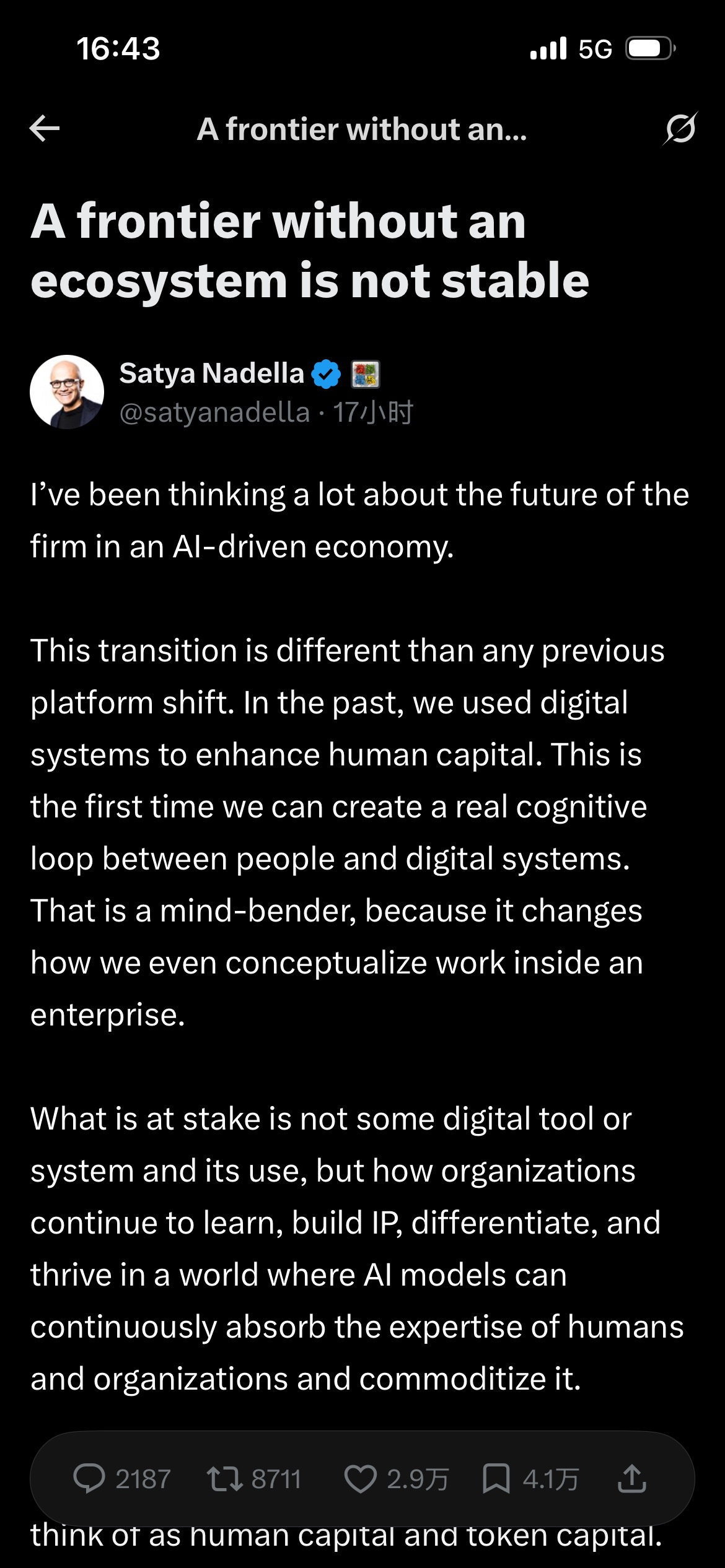

Nadella has published another long article discussing the economic reflexivity of AI. The concept of the Information Paradox describes the dilemma for information sellers: to prove the value of information, they must first disclose it; but once the information is disclosed, its value is captured for free by buyers. In the AI era, buyers who want to use good AI models instead risk handing over valuable know-how. The result is paying twice: once for tokens, and once for proprietary knowledge. Nadella directly quotes Karp's view in the article, "What technology customers want is control over their own computing power, models, data stack, and alpha. They need to be sure they own the means of production, not that it's being transferred to someone else."

Currently, it seems the new narrative for AI applications is a competition between two paths.

Camp A: The Token Economics of Model Vendors

Stronger models are better -> Higher usage is better -> Feedback for model training -> Shared weights

Form: Token consumption / Subscription-based

Camp B: Controlling AI Sovereignty / Learning Loop

Models are switchable -> Data/Logic stays within the enterprise -> The loop and data are the true AI Alpha

Form: Cloud platform / Sovereign stack / Heavy on-premise deployment

The current situation is that Camp B has been suppressed by Camp A for over half a year and is now starting to counterattack, vying for the right to define the narrative. Who will win?

$Apple(AAPL.US) is suing OpenAI for ingesting trade secrets and intellectual property during their collaboration. OpenAI might delay its IPO process as a result.

However, looking at the bigger picture, this echoes the importance of data sovereignty advocated by $Palantir Tech(PLTR.US)'s Karp. If corporate data isn't properly restricted, it's essentially handing over the most critical assets to model providers. You'd be paying for tokens while the model providers learn your core business, thus losing the biggest AI Alpha. PLTR just released a Sovereign AI Playbook, which details how to avoid this situation.

The biggest risk currently facing PLTR is not its performance, but its narrative. PLTR's performance remains excellent, but compared to last year's stock price decline, competitors have emerged in the market that may threaten its monopoly position. In the past, the market was willing to pay a high valuation premium for PLTR, recognizing its unique competitiveness in the toG market as the sole gateway to the OS operating system in the AI era.

However, entering 2026, both OpenAI and Anthropic have shown the potential to directly sign cooperation agreements with governments. Even if they still need to be integrated into PLTR's compliant data platforms such as Foundry, Ghothm, and Fedstatt, they still pose a competitive threat. This competition itself has shaken the monopoly expectation, thereby suppressing the valuation premium.

I think this is also the reason why Karp has been directly counterattacking recently. He is actively defining new competitive advantages, emphasizing that enterprises/institutions should possess data sovereignty that cannot be replaced.

This article released by PLTR corresponds to Karp's recent interview on CNBC, expressing a similar viewpoint to the lengthy piece by Microsoft's Nadella earlier.

In the AI era, the core assets of an institution are data retention + weights/institutional knowledge + autonomous architecture; selling AI by token is hollowing out the customer.

Institutions must keep data, weights (institutional knowledge sedimented within the model), and decision-making power in their own hands; ceding sovereignty means giving up future options and alpha.

This is also PLTR's product philosophy: whose hands the data is in → who sediments the weights/knowledge → can the model be swapped without losing institutional memory → to whom does the value compound.

Saylor announced a new active capital management framework on 6.29. Last week, through MSTR's additional share issuance financing, cash positions were restored. The framework consists of 5 parts:

- USD Reserve Policy (Build a $2.55 billion reserve, dedicated to preferred share dividends + debt interest payments, minimum coverage of 12 months, current reserve can cover 17.5 months)

- STRC dividend increased to 12%

- $1 billion credit line to repurchase preferred shares (STRC, etc.)

- $1 billion credit line to repurchase MSTR common shares

- BTC Monetization: $1.25 billion credit line to sell BTC to replenish reserves, pay interest, and fund repurchases

We previously discussed Saylor facing the bear market "impossible triangle" of "STRC 100", "BTC per share", and "BTC holdings". It now appears Saylor chose to first secure "STRC 100", and will maintain "BTC per share" through repurchases, while "BTC holdings" will shift from buy-only to active management. This is equivalent to Saylor acknowledging the fragility of the "only in, never out" pure Hold model under a structure with high fixed costs (high dividends), thus requiring the establishment of defensive tools.

From market feedback, it's clearly positive for STRC holders. After the dividend increase and cash reserve build-up, STRC's face value has also rebounded significantly.

For MSTR, the repurchase authorization is positive, but BTC monetization introduces potential selling pressure. However, in the short term, the risk of a blow-up FUD has eased somewhat, and MSTR has also rebounded strongly.

I believe upgrading from "simple holding" to an "active asset management strategy" greatly reduces the risk of a death spiral blow-up from being forced to sell coins at low prices during a bear market. The extreme narrative of "only buying, never selling" is less important than survival; not blowing up is the top priority. What BMNR can learn from this is that, although it doesn't have debt, interest payment pressure, or other blow-up risks, its mNAV has already fallen to 0.83, and the previously authorized $4 billion repurchase has also reached its theoretical execution window.

Active management encompassing strategies for common shares, preferred shares, USD reserves, repurchase discipline, etc., should be the next stage of evolution for all DAT companies. MSTR is once again leading the way.

Over the past few days, both MSTR and BMNR have fallen a lot. BTC breaking below 60k and ETH breaking below 1.6k are of course the main reasons, but the two DATs have fallen even more, which means their premiums have compressed further. I believe the primary cause is STRC's significant de-pegging to 70+, deviating too much from the 100 target price without recovery for a long time, reflecting the market's extremely low confidence in MSTR's credit premium. I'll try to analyze why this is happening.

Since STRC started increasing volume in March '26, it has already raised 10 billion for MSTR to hoard coins. Its financing logic has also become "STRC issues more to hoard coins, MSTR issues more to pay interest." The implied meaning is that Saylor prioritizes the interests of STRC preferred shareholders, covering STRC's high dividends through MSTR issuance, and using dividend adjustments to anchor STRC at a price of 100. This logic worked well before, until May when Saylor sold 32 BTC. With insufficient cash reserves, the market began to worry that MSTR lacked the ability to pay interest and would sell coins to cover it. To quell market concerns, Saylor proposed that selling coins is fine, as long as the per-share coin holding increases. But the market didn't buy it. What followed was a continuous decline in MSTR's premium, STRC falling to 90/80/70, and BTC breaking below 60k.

I believe from this point on, Saylor's market expectation management has gone wrong. The management of the three expectations—STRC at 100, per-share coin holding, and BTC holdings—is very delicate. It's fine during a bull cycle, but in a bear market, it's almost an impossible trinity. Maintaining per-share coin holding means MSTR cannot be issued at a low premium. With limited cash, how can the interest rights of STRC creditors be guaranteed? So STRC holders voted with their feet, driving the price down to 70+. According to the original plan, Saylor could fix STRC at 100 by adjusting the interest rate. But currently, with limited cash, financing closed, and needing to raise rates further, the market would be even more skeptical of your ability to pay interest.

This is like a juggler in a circus throwing balls into the air. Keeping one or two balls from falling isn't hard, but keeping three balls from falling simultaneously requires great skill. Therefore, to restore confidence in STRC and prove Saylor's ability to pay interest, the other two expectations must be broken: either issue MSTR at a low premium (damaging per-share coin holding) or sell coins (damaging the coin-hoarding expectation).

As for BMNR, over the past week, mNAV has fallen to 0.85, a historical low. The logic is the same. Doubts about confidence in STRC will spread to all DAT business models; they're all grasshoppers tied to the same rope. Although BMNR has no debt and ETH staking provides interest-paying capability, the market doesn't care. It's a blanket sell-off now.

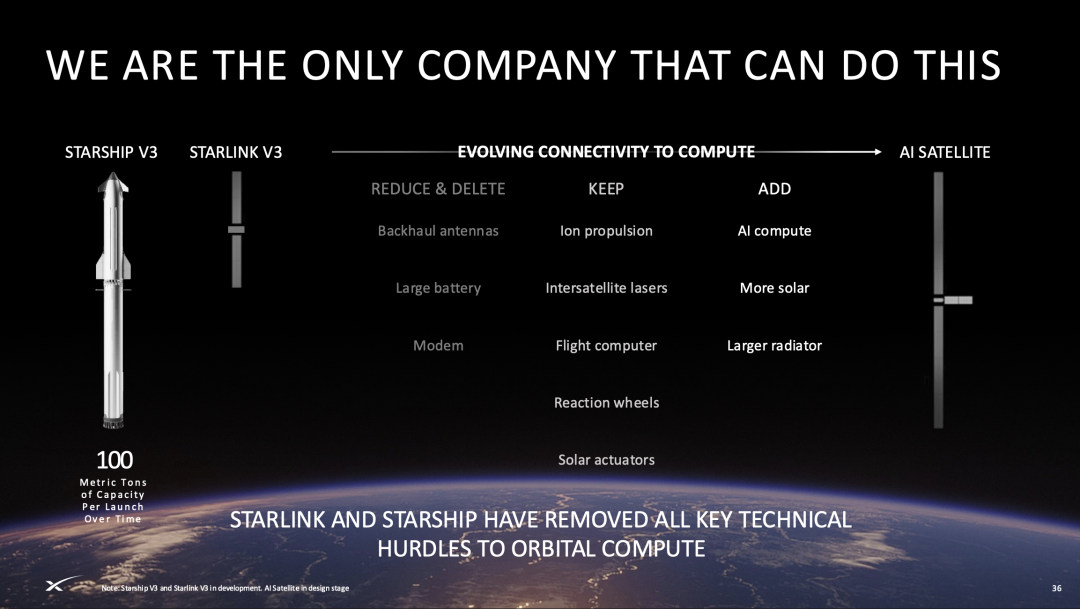

$SpaceX(SPCX.US)1 trillion up, 1 trillion down, a textbook example of low liquidity leveraging high market cap volatility, like aiming a high-magnification sniper rifle, a slight hand tremor results in a screen-spanning displacement.

$SpaceX(SPCX.US) Think of SPCX as the ship that explored the New World during the Age of Discovery. By analogy, investors buying at a premium now are like the royal nobles who funded Columbus back then.

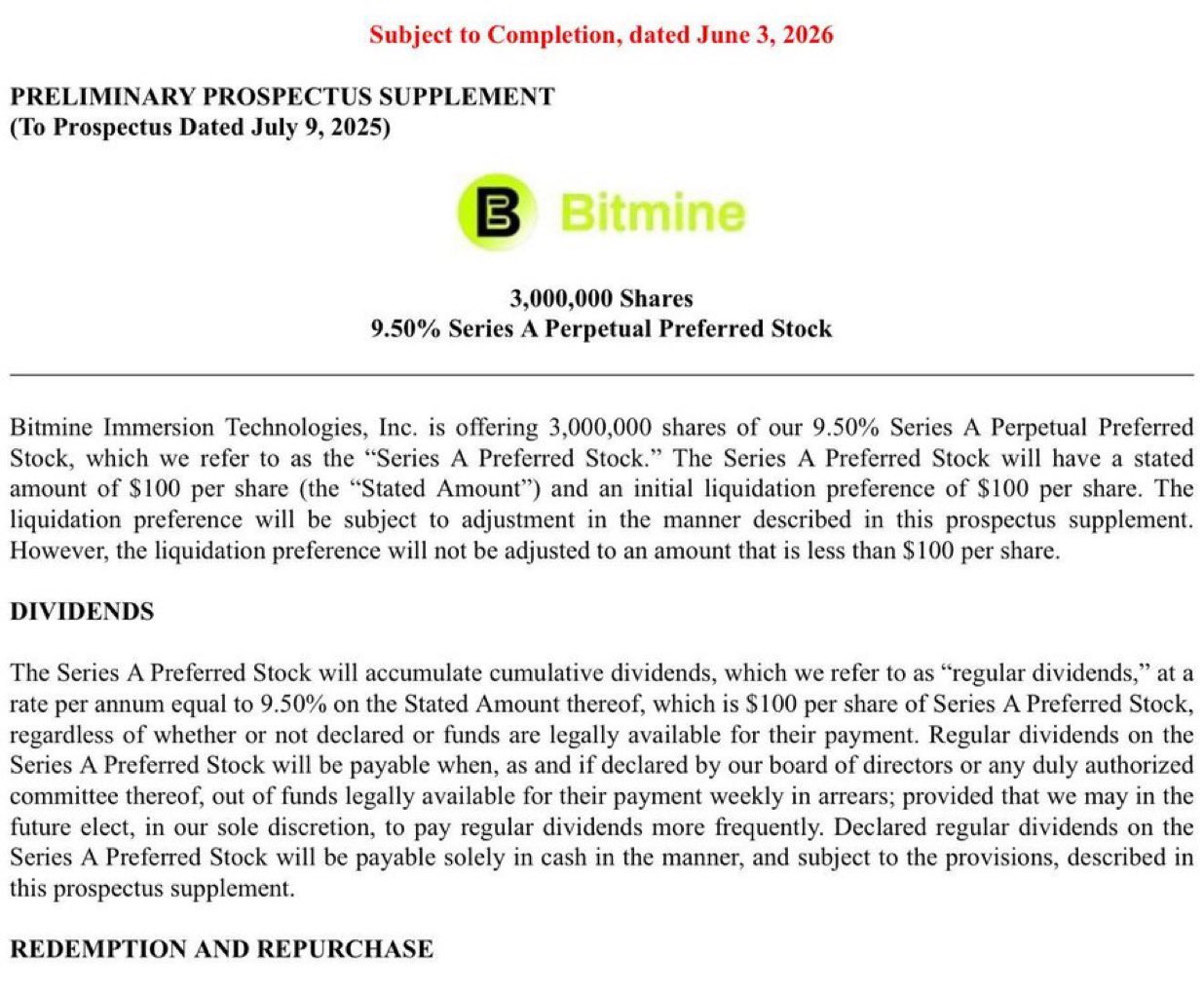

$Bitmine Immersion Tech Pref Shares BMNP 9.5 Perp 07/15/26(BMNP.US) has quietly gone public. The only metric to watch going forward is the trading volume.

$Microsoft(MSFT.US) Nadella published a lengthy article, the core idea of which is that "in the AI era, corporate competition is not about choosing the best model, but about whether one can establish a sustainable, compounding learning loop." That is to say, can you replace the general-purpose model while preserving the organization's unique accumulated learning?

For enterprise AI operating systems, selling the loop is better than selling tokens.

After reading the whole article, my feeling is, isn't this exactly the value that PLTR has been creating all along?$Palantir Tech(PLTR.US)

Elon Musk: ” I want to take anyone who wants to be beyond the solar system. I want to take you there. you. literally you. to the moon. to mars. to beyond.“

Tonight, $SpaceX(SPCX.US) goes public. There are several key milestones worth watching:

On 6.12, the listing day, 4.2% of the float will be released;

On 7.7, Nasdaq gave SPCX the green light to join the Nasdaq 100 just 15 working days after listing, which will bring passive buying from index funds;

In early August, after the Q2 earnings report, a lock-up release of 7% occurs. If the stock price exceeds 30% above 135 at that time, an additional 3.5% will be released, totaling a maximum release of 10.5% of the float;

In early November, after the Q3 earnings report, another 10% lock-up is released;

There might be a surge after the listing tonight, but this doesn't reflect the fundamentals; it's more about the low float premium. The subsequent two rounds of lock-up releases will involve 2~3 times the number of shares in the IPO float. So, before the lock-up releases, it might be more like a game of greater fool theory.

Over the past week, both BTC and ETH experienced significant declines, but for BMNR, it was still a milestone week. The company finally expanded its financing toolbox beyond ATM - the preferred stock BMNP. BMNP has a total authorized issuance of 20 million shares. The first batch was planned to issue 3 million shares at a price of 100 with an interest rate of 9.5%, paying interest weekly. The actual issuance was 3.5 million shares at a discounted price of 80, with the interest rate and payment method unchanged. Considering the downturn in the crypto market, a certain degree of discount was within expectations...

$SpaceX(SPCX.US) This page in the roadshow materials is the most stunning; no other company can replicate this vertically integrated supply chain.

Self-developed rockets (lowering launch costs) → Self-developed satellites (lowering manufacturing costs) → Self-built inter-satellite communication network (lowering data transmission costs) → Proprietary AI models (directly consuming computing power) → Owned end-user platform (X, 550 million MAU)

From silicon wafers to space, from space to the end-user, fully integrated across the entire chain. Valuation must consider a monopoly premium; the calculator is hard to figure out now.

BMNR has issued a preferred stock product BMNR, similar to STRC. The first batch will raise 300 million at a price of 100 yuan per share for 3 million shares, with a 9.5% annual interest rate, paying interest weekly, and requiring an annual payment of $28.5 million in perpetual dividends.

Currently, ETH staking rewards (currently about 2.7%) bring BMNR $296 million annually, meaning 10% of that income will be used for interest payments.

Finally, there is a new financing toolbox beyond ATM. Of course, there are also risks. If the ETH price reaches about $1,200, staking rewards will be unable to cover the debt.

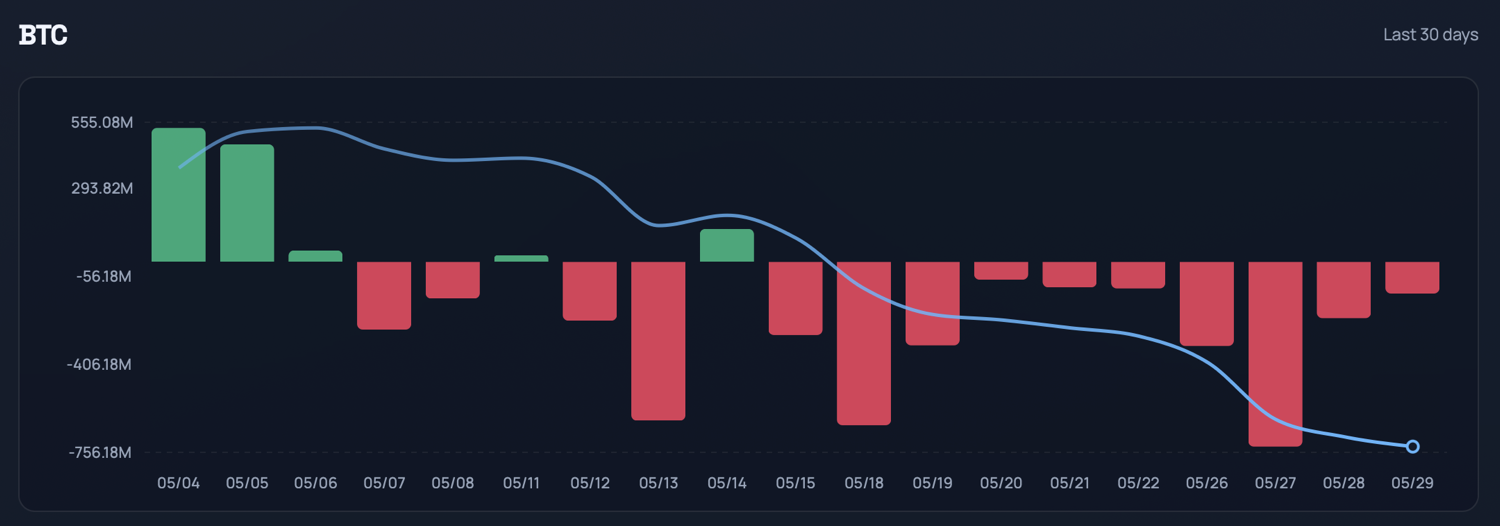

Over the past half month, BTC has fallen quite a bit, mainly due to ETF net outflows. From the data, there were only four or five days of ETF net inflows in May, with outflows on all other days. In fact, there have been continuous net outflows for over ten days from May 15th until now. For liquidity-sensitive assets like crypto, ETF fund flows have a significant impact on daily price movements. Meanwhile, MSTR has also started selling coins to pay interest. Although they only sold 32, which is negligible compared to their total holdings, this breaks Saylor's previous promise of never selling coins. The essence of DAT's business model is to hold the underlying assets long-term, not to buy low and sell high for short-term trading...

$Li Auto(LI.US)$XPeng(XPEV.US) reported earnings on the same day. @Dolphin Research Dolphin Research chose to prioritize covering XPeng, with earnings analysis and minutes promptly following. Li Auto didn't even get a quick earnings review... This also reflects market sentiment from an institutional perspective, I guess🤦

Over the past week, there have been two noteworthy pieces of information regarding BMNR. First, Vitalik published a lengthy article about EF's positioning and the vision for ETH...