美國股市反彈(SPX +0.4%,NDX +0.8%),微軟雲業務強勁增長令投資者安心,認為人工智能投資正在產生回報,且超大規模資本支出不會進一步升級,這抵消了通脹擔憂以及美聯儲維持利率不變後 30 年期國債收益率跳升的影響。Meta 在盤前下跌,因其第三季度營收指引偏輕。投資者關注點仍集中在人工智能資本支出的潛在過度支出及可能的回報上;標普 500 指數 2026 財年每股收益預期同比增長 25% 至 346 美元,相當於 21.1 倍遠期市盈率(4.7% 的盈利收益率),與 10 年期國債收益率持平。美伊衝突升級持續。由於長期盈利預期下降、自動駕駛網約車可能商品化以及估值過高,建議對特斯拉保持謹慎。

Gary Black Tracker

Daily quotes, trades and insights from Gary Black.

Gary Black Tracker推薦關注

G

$Meta(META.US) (-6%) 公佈了一份混亂的季度財報,儘管營收和非公認會計准則每股收益(排除一次性項目)高於預期,但第三季度營收指引略低,且 2026 財年資本支出指引略高於預期。第二季度自由現金流遠高於預期。我預計 $Meta(META.US) 將在未來幾天內反彈,因為投資者將意識到扣除一次性成本後,META 的利潤依然強勁。

第二季度業績:- 公認會計准則每股收益 6.18 美元,低於預期的 7.14 美元。排除 35.8 億美元的一次性法律和遣散費後,非公認會計准則每股收益為 7.35 美元,高於預期的 7.14 美元- 總營收 608 億美元(同比增長 28%),高於預期的 602 億美元- 日活躍用户 36 億(同比增長 3%),符合市場共識- 自由現金流 +7.84 億美元,而預期為 -12.15 億美元第三季度指引:- 營收 610-640 億美元,低於預期的 632 億美元2026 財年資本支出 1300-1450 億美元,此前指引為 1250-1450 億美元,華爾街預期為 1360 億美元。

G

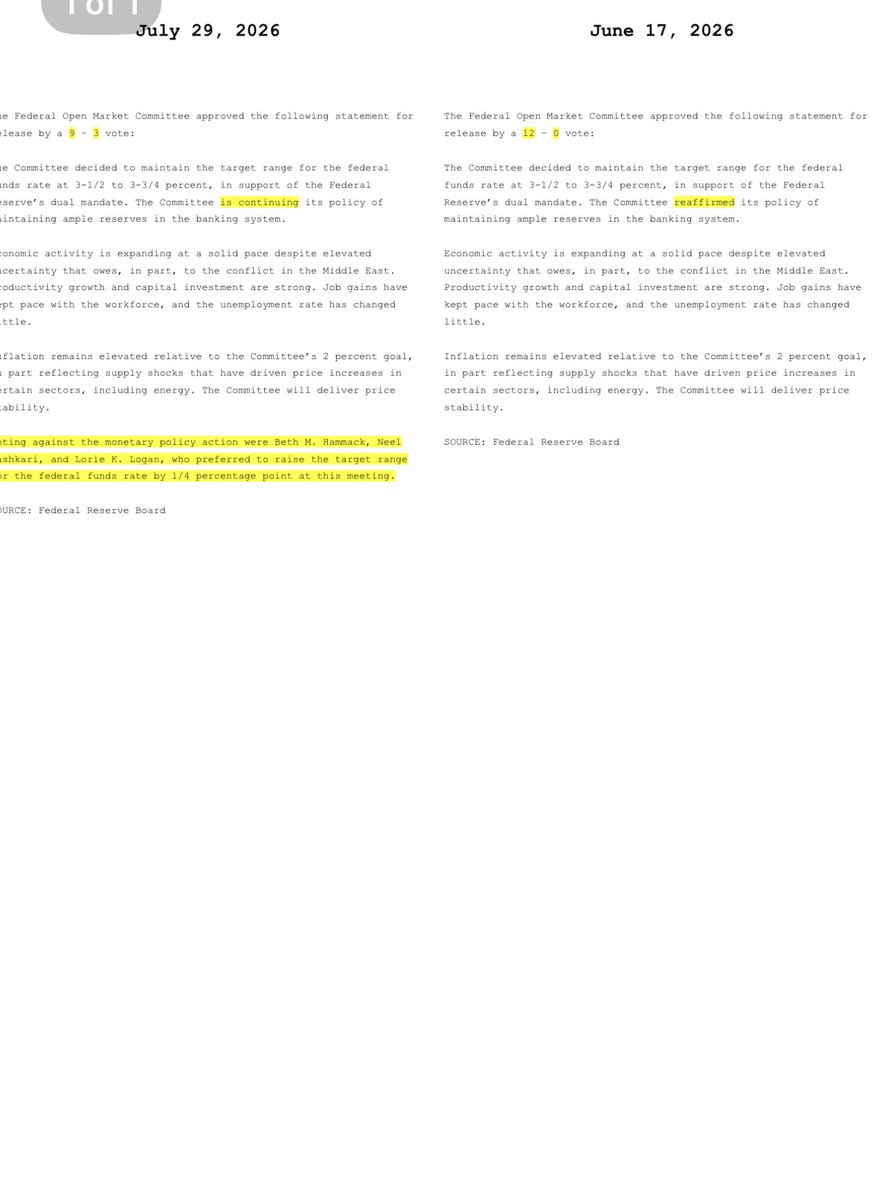

聯邦公開市場委員會以 9 比 3 的投票結果決定將基準利率維持在 3.5% 至 3.75% 的區間,三名委員反對並主張加息。委員會重申了其 “實現物價穩定” 的承諾,官員們將在週四獲得最新的通脹數據,同時圍繞伊朗衝突和通脹的壓力與不確定性日益加劇。

決議公佈後,NDX 指數上漲 0.3%,兩年期國債收益率從 4.32% 降至 4.26%,9 月加息的概率在決議前從 95% 降至 75%。這一決定不應改變投資者對未來貨幣政策的看法,因為整個聲明中僅有一個詞的變動。今天公告的方方面面都體現了耐心。

以下是今日美聯儲聲明與 6 月 17 日聲明的變化之處。

美聯儲主席沃什的新聞發佈會將於美東時間下午 11:30 開始。

G

Visa ($Visa(V.US)) 盤後下跌 1%,儘管 Visa 公佈的三季度財報、營收和支付數據均超出預期,但由於費用增長高於預期,其對四季度的盈利指引低於市場預期。

三季度實際業績- 調整後每股收益 3.32 美元, vs 預期的 2.98 美元- 淨營收 116 億美元(同比增長 14%), vs 預期的 114 億美元 - 運營費用 47.6 億美元(同比增長 19%), vs 預期的 40 億美元- 支付交易量(同比增長 10%), vs 預期的同比增長 9%。四季度指引- 調整後每股收益處於中雙位數增長的低端, vs 預期的 +16%- 淨營收處於低雙位數增長的高端, vs 預期的 +12%- 運營費用增長處於低雙位數增長, vs 預期的 +8%。我們認為,如果週三下午 5 點(美東時間)的電話會議確認三季度因費用增加導致的利潤率壓縮情況延續至四季度,$Visa(V.US) 的股價可能會進一步下跌(類似於上週 AXP 的走勢)。G

美國股市下跌,韓國半導體股暴跌及 AI 支出擔憂加劇了芯片製造商的拋售潮,其影響超過了油價和國債收益率下降帶來的漲幅。布倫特原油在美伊暫停衝突及霍爾木茲海峽談判期間下跌 3.5% 至 85 美元;10 年期國債收益率在預期維持利率不變的美聯儲會議前回落至 4.61%。大型科技股和消費者財報即將公佈,市場焦點集中在 AI 資本支出上。標普 500 指數 2026 年每股收益(EPS)預估已同比增長 25% 至 346 美元(市盈率 21.4 倍)。鑑於 forward earnings estimates(遠期盈利預估)下滑、無監督自動駕駛技術可能商品化以及估值看似過高,我對$特斯拉(TSLA.US) 保持謹慎。

G

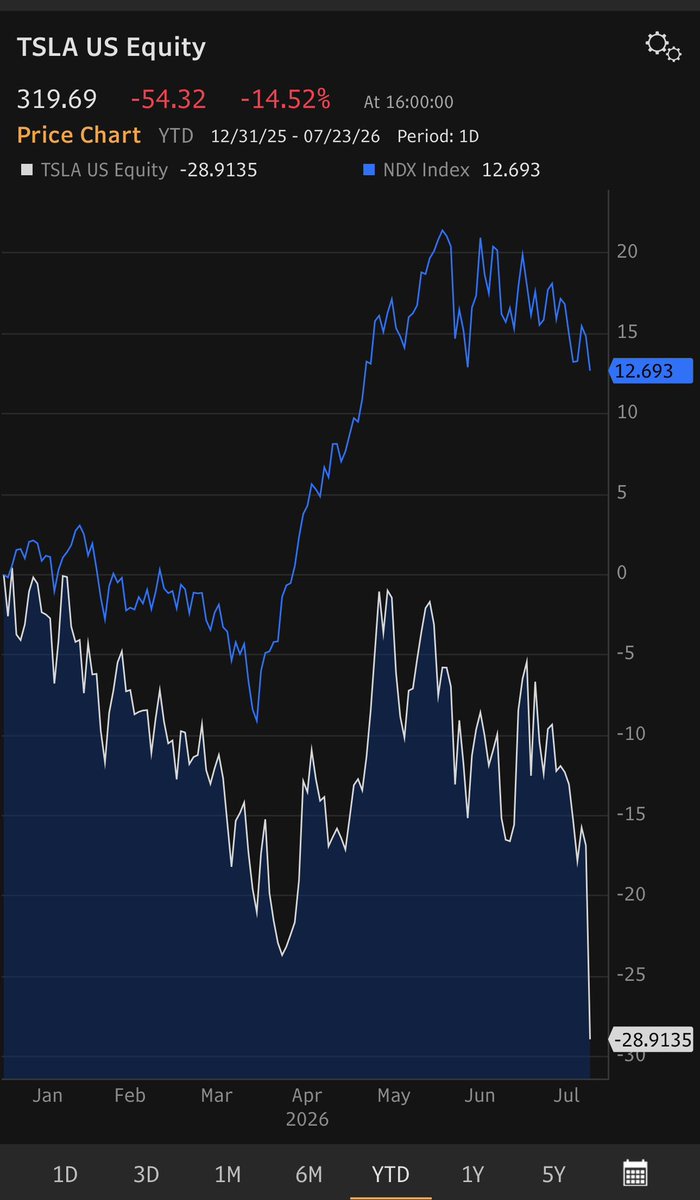

$特斯拉(TSLA.US) 今早下跌 7%,如果盤前跌幅持續,目前年初至今 (YTD) 跌幅達 23%,而納斯達克指數 (NDX) 同期上漲 15%。

特斯拉管理層本可在昨天的財報中提供一兩個常見的無監督自動駕駛指標:1/ 在沒有安全操作員的情況下運行的無監督自動駕駛車輛數量,我們估計約為 40 輛,而 Waymo 為 3,500 輛;或者其相近的指標:2/ 每週完成的無需安全監控人員的付費無監督自動駕駛行程數量(我們估計特斯拉為 4,000 次,而 Waymo 約為 50 萬次),這樣投資者就可以衡量特斯拉在無監督自動駕駛方面相對於同行的進展。相反,特斯拉在第二季度財報電話會議上提供的 largely irrelevant 指標,例如自啓動無監督自動駕駛網約車服務以來累計的無監督自動駕駛里程(38 萬公里),以及每週無監督駕駛里程的周環比增長率(每週 10% 以上),且未澄清該指標或提供起始基數。投資者厭惡不確定性,而特斯拉似乎不願或無法通過披露信息來減少與其無監督自動駕駛規模化相關的不確定性。這種模糊性顯然正在損害特斯拉的股價。認為特斯拉今早股價下跌是因為其計劃 2026 財年資本支出為 250 億美元(與之前相比沒有變化)的想法是荒謬的。@travisraxelrodG

$谷歌-C(GOOG.US) -3% AH after missing on 2Q non-GAAP earnings and boosting its FY’26 CapExp, potentially triggering a new CapExp arms race.

$谷歌-C(GOOG.US) now projects a 2026 CapEx range of $195B to $205B, up $15B from its prior guidance, which the company says is necessary to meet the demands of the AI infrastructure boom. Many analysts were expecting GOOG to lift its CapEx outlook, after Google announced an $85 billion equity raise last month. The higher guidance reflects the company’s efforts to accelerate its expansion of AI computing capacity and book more revenue from cloud-computing clients. Still, the negative free cash flow and heavy bill for AI infrastructure is fueling investor jitters.$谷歌-C(GOOG.US) 2Q cloud revenue totaled $24.8B, up +82% from a year ago and above the $22.5B analysts had expected. The company’s cloud backlog, a measure of contracted work that hasn’t yet been recorded as revenue, grew to $514B, up from roughly $460B, a quarter earlier.At a 2026 P/E of 23.6x and +15% forward long-term rev growth and +17% forward long-term eps growth, $谷歌-C(GOOG.US) still looks compelling and should be bought on weakness.

G

$特斯拉(TSLA.US) (-3% AH) 因未達標而表現不佳,排除監管信用後的汽車毛利率為 16.3%,低於預期的 18.4%,導致非公認會計准則每股收益出現巨大缺口(0.33 美元 vs 華爾街預估的 0.55 美元)。資本支出 58 億美元導致自由現金流轉為負值-11 億美元,這在預期之中。積極方面,活躍 FSD 訂閲用户數為 148 萬,環比增長 16%,第一季度年化增長率達 63%;第二季度 FSD 在北美交付車輛中的搭載率創下 55% 的歷史新高。Optimus 的生產仍計劃於 2026 年底開始。

電話會議將於美東時間 5:30 舉行。投資者最希望聽到的是,無需安全監控人員監督的無人駕駛技術(目前特斯拉有 40 輛車,而 Waymo 有 3,500 輛)能多快實現規模化。

G

我問過 Grok,在股市歷史上,是否曾有過像 $SpaceX(SPCX.US) 這樣市值超過 1 萬億美元、且交易價格高於遠期企業價值/營收(EV/Rev)40 倍的公司?

Grok 的回答是:沒有。從未有過一家公司能在維持超過 1 萬億美元市值的同時,以高於遠期 EV/Revenue 40 倍的倍數進行交易。$SpaceX(SPCX.US) 的股票處於未知領域,很可能因其極端的估值而繼續下跌。$英偉達(NVDA.US) 是最接近的候選者,但即使它,在萬億規模下,其遠期 EV/Rev 倍數也未超過 40 倍。• NVDA 首次觸及約 1 萬億美元市值是在 2023 年 5 月,此後已達到 4 萬億至 5 萬億美元以上。• 歷史最高 trailing EV/Rev 約為 44.9 倍。• 遠期(未來 12 個月)EV/Rev 顯著較低,在其 1 萬億美元以上的時期通常處於 10–25 倍區間,反映了激進的營收增長預測(數據中心/AI 領域往往同比增長 50%+)。分析師模型中的近期估值徘徊在遠期營收的 11–13 倍左右。極高的遠期 EV/Revenue 倍數(>40 倍)意味着極度的樂觀,這種樂觀甚至在南達(Nvidia)炒作高峰期也缺乏共識估計的支持。其遠期 P/E 有時超過 40 倍,但由於銷售規模的擴大,營收倍數壓縮得更快。

G

別説我沒警告過你。

$SpaceX(SPCX.US) 目前股價為每股 126 美元——相較於其 IPO 後 226 美元的峯值,短短一個月內出現了驚人的 45% 反轉,且遠低於其 135 美元的 IPO 發行價。SPCX 的遠期(FY’2026)企業價值/營收倍數仍高達 45 倍。來源:Financial Review標誌性的華爾街投資者彼得·林奇並不看好買入小盤 IPO 股票,他喜歡説 IPO 代表 “可能定價過高”(it’s probably overpriced)。那些完全未經證實的在太空建設數據中心的計劃被 endlessly 剖析。SPCX 的招股書列出了該公司聲稱的荒謬總可觸達市場(TAM):28.5 萬億美元,接近美國整個 GDP。SpaceX 的虧損情況也被披露和討論。確實,歷史上可能沒有哪次 IPO 像這次一樣受到如此嚴密的審視。如果投資者在知曉所有風險後仍然想要買入,那他們只能自食其果。這在一定程度上是公平的,但它忽略了 SpaceX、其投資銀行家及其顧問以看似毫不在意長期投資者利益的方式,通過結構化設計此次 IPO 來操縱短期收益——以及一個 5000 億美元的佣金池。正如施羅德澳大利亞股票主管 Martin Conlon 本週所寫,投資銀行知道,“大量流向基於規則的投資流程的資金”,如被動投資和算法交易,已經改變了市場的運作方式。因此,他們成功遊説了納斯達克和富時羅素等指數市場運營商——用 Conlon 的話來説——扭曲並操縱規則,使得像 SpaceX 這樣的大型虧損公司能夠幾乎立即被納入主要股市指數。SPCX 的銀行家們成功遊説了納斯達克和富時羅素等指數市場運營商,操縱規則,使得像 SpaceX 這樣的大型虧損公司能夠幾乎立即被納入主要股市指數。SpaceX 的 IPO 融資額創下歷史紀錄,達到 850 億美元——是歷史上第二大 IPO 規模的三倍。但銀行家們知道,他們可以創造一個 “高度失衡的供需局面”,其中不到 1000 億美元的自由流通股本將為超過 2 萬億美元的賬面市值設定價格。這就是我們今天看到的現狀,SPCX 的 2026 年 EV/Revs 倍數仍高達 45 倍,看起來荒謬地高估。然而,在啓動對 SPCX 覆蓋的 36 位華爾街分析師中,有 80% 給予該股票買入評級。只有一家——晨星(Morningstar),大概是因為無法從 SPCX 獲得未來的銀行佣金——給出了賣出評級。這説明了所有問題。

G

$奈飛 (NFLX.US) 盤後下跌 7.7%,此前公佈的二季度業績符合預期,但給出的三季度及 2026 財年指引不及預期。管理層將 2026 年業績不及預期歸咎於冬季奧運會和世界盃,但投資者將繼續關注奈飛缺乏新內容的問題。

二季度業績:

- 營收 125.6 億美元,預期 125.8 億美元- 調整後每股收益 0.80 美元,預期 0.79 美元- 營業利潤 41.9 億美元,預期 41.3 億美元- 營業利潤率 33.4%,預期 33.0%三季度指引:

- 營收 128.6 億美元,預期 130.0 億美元- 調整後每股收益 0.82 美元,預期 0.84 美元- 營業利潤 42.7 億美元,預期 43.6 億美元2026 財年指引:

- 營收 510-514 億美元,此前指引為 507-517 億美元(預期 514 億美元)- 全年營收增長 13-14%,此前指引為 12-14%- 廣告收入維持 30 億美元不變奈飛管理層可能會試圖讓投資者關注 2026 年上半年觀看時長(同比增長 2%,而 2025 年上半年為 1.5%),但在我看來,這種單位增長水平並不令人印象深刻。話雖如此,如果公司能夠實現 10-12% 的長期營收增長和 15-17% 的長期每股收益增長(市場預期),那麼以 19.4 倍 2026 年調整後每股收益的估值來看,它似乎很便宜。

G

$奈飛(NFLX.US) 盤後公佈第二季度業績符合預期,但給出的第三季度和 2026 財年指引未達預期,股價下跌 7.7%。管理層將 2026 年指引的不足歸咎於冬季奧運會和世界盃,但投資者將繼續關注 NFLX 缺乏新內容的問題。

第二季度業績:

- 營收 125.6 億美元,預期 125.8 億美元- 調整後每股收益 0.80 美元,預期 0.79 美元- 營業利潤 41.9 億美元,預期 41.3 億美元- 營業利潤率 33.4%,預期 33.0%第三季度指引:

- 營收 128.6 億美元,預期 130.0 億美元- 調整後每股收益 0.82 美元,預期 0.84 美元- 營業利潤 42.7 億美元,預期 43.6 億美元2026 財年指引:

- 營收 510-514 億美元,此前指引為 507-517 億美元(預期 514 億美元)- 全年營收增長 13-14%,此前指引為 12-14%- 廣告收入指引維持 30 億美元不變

G

還是不明白人們把$SpaceX(SPCX.US) 看作什麼投資。它已經是個巨無霸了(市值 1.8 萬億美元),所以上漲空間有限。它要到 2027 年才能產生利潤。它的 2026 年企業價值/收入比是 47 倍($特斯拉 (TSLA.US) 是 14 倍),2026 年企業價值/息税折舊攤銷前利潤比是 110 倍($特斯拉 (TSLA.US) 是 97 倍)。我理解一旦其他航空公司效仿邊疆航空,將 SpaceX 星鏈作為商業航空公司的標準 WiFi 套餐,會帶來新的總可尋址市場的故事。但 SPCX 有 20% 的股份將在 8 月解鎖出售,44% 的股份將在 9 月初解鎖出售,這將使可交易流通股增加大約 900%。估值在某個時間點總得是重要的。

G

$Lucid(LCID.US) 暴跌 -45% 至 $2.98,此前一份電動汽車通訊(

G

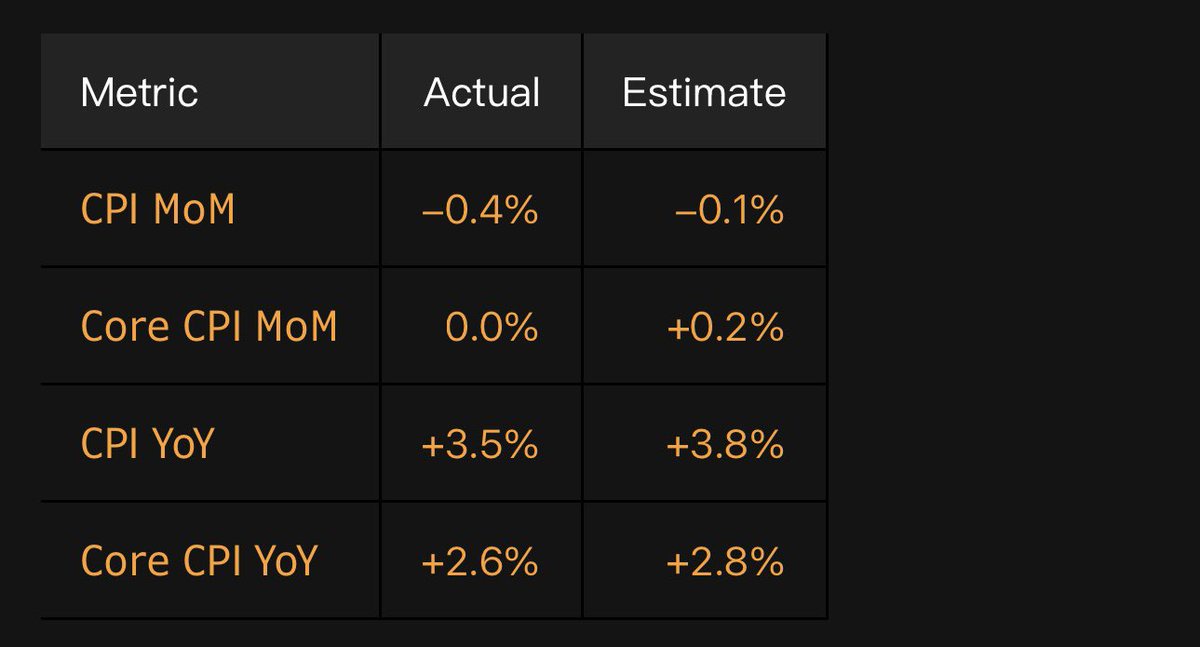

美國 6 月 CPI 數據遠低於預期,包括六年來首次出現環比下降,這減輕了美聯儲新任主席凱文·沃什(Kevin Warsh)加息的壓力。

G

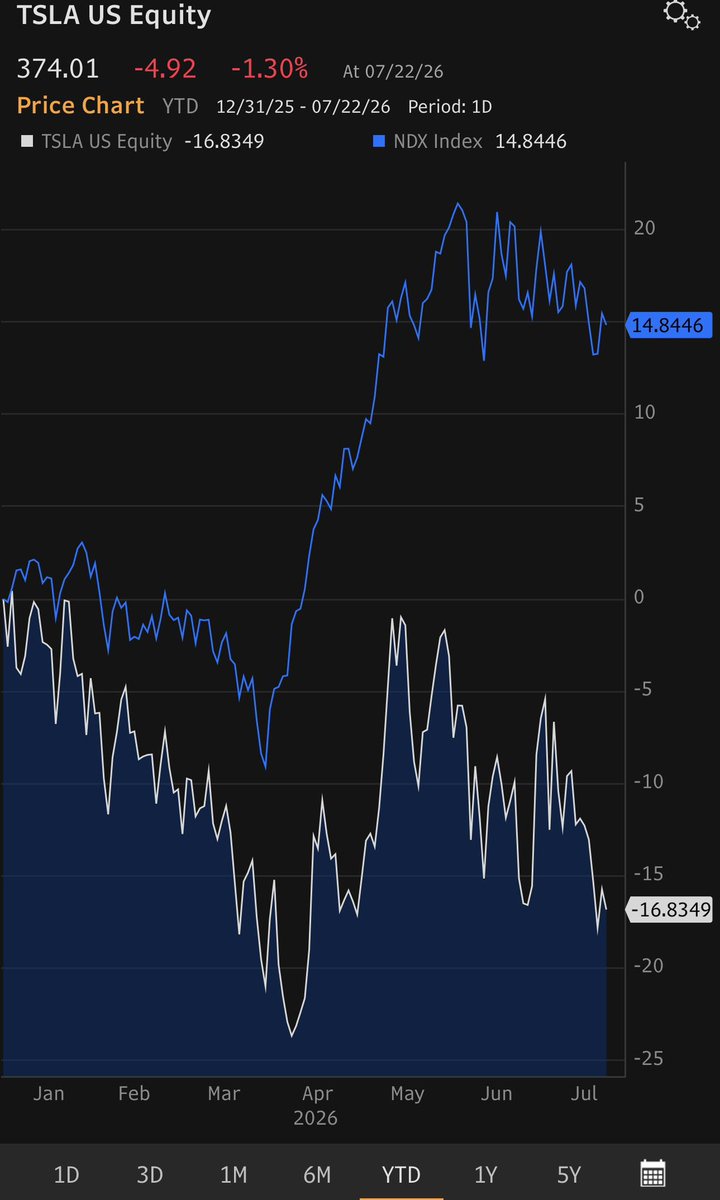

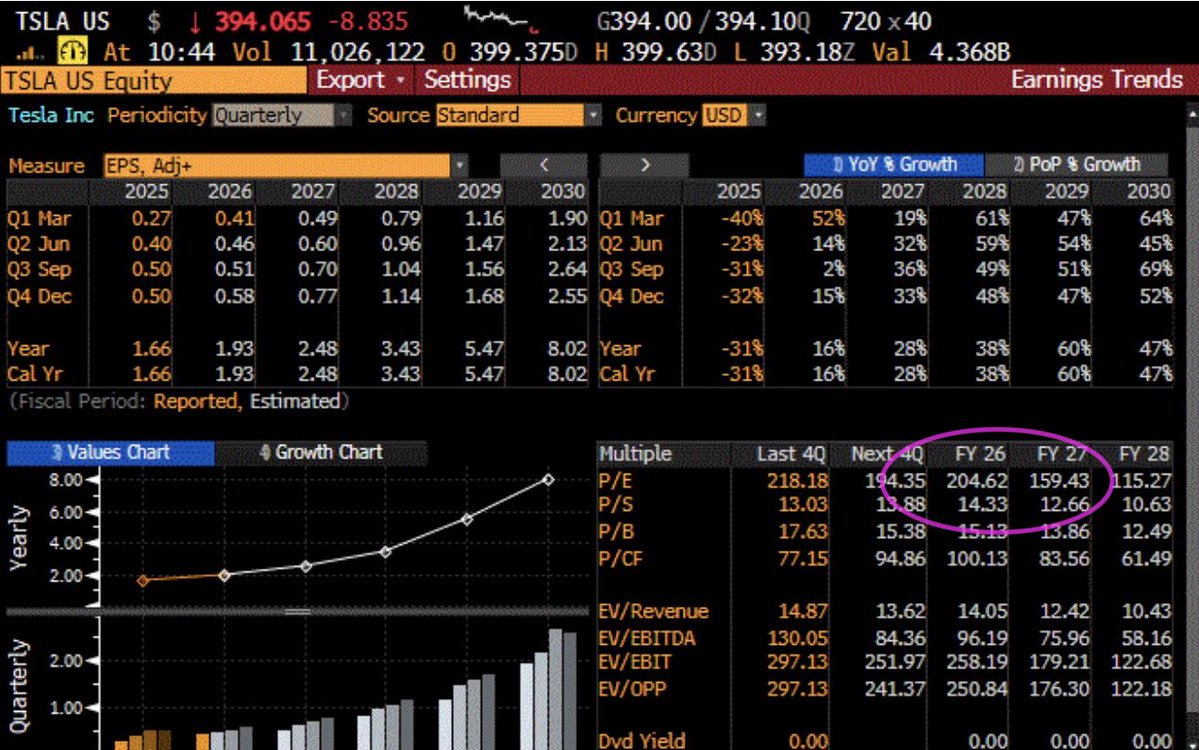

儘管我非常喜歡$特斯拉 (TSLA.US) 這家公司,但很難支持其估值(2026 年市盈率 209 倍 vs 長期每股收益增長 +35%,市盈增長比率 6 倍),與其他 “八大金剛” 股票(平均市盈增長比率 2 倍)相比,其估值仍然過高。大多數 X 平台上的特斯拉支持者在討論$特斯拉 (TSLA.US) 時,都選擇無視估值,因為無監督自動駕駛正變得商品化,這也是為什麼特斯拉年初至今持續表現不佳(特斯拉-7% vs 納斯達克 100 指數 +18%)。與此同時,$太空資本 (SPCX.US) 很可能很快會跌破其 135 美元的首次公開募股價,因為 8 月初將有 20% 的限售股解禁。

G

$特斯拉 (TSLA.US) 被高估的估值(2026 年市盈率 205 倍,而 2026-2030 年每股收益增長率為 +35%,市盈率相對盈利增長比率 6.0 倍)以及不斷下調的遠期盈利預期(2027 年每股收益預期年初至今下調 17%)是大多數機構投資者回避該股票的原因。每個人都認可特斯拉全自動駕駛(FSLA)擁有的獨特技術優勢,但大多數社交媒體大 V 不會談論估值問題,也不會解釋為何分析師們的預期持續下調。這兩個原因(估值過高和預期下調)導致 $特斯拉 (TSLA.US) 持續跑輸納斯達克 100 指數。

G

著名投資者傑里米·格蘭瑟姆表示,歷史終將嘲笑$SpaceX(SPCX.US),這個剛剛加入納斯達克 100 指數的 “人類歷史上最瘋狂的 IPO”。

彭博 AI 摘要

▪傑里米·格蘭瑟姆表示,歷史終將嘲笑 SpaceX,稱其為 “人類歷史上最瘋狂的 IPO”。▪格蘭瑟姆對 SpaceX“建立使生命多行星化所需的系統和技術” 的目標不以為然,並認為其招股説明書對未來的投資者來説將是可笑的。▪儘管格蘭瑟姆持懷疑態度,華爾街對於 SpaceX 能飛多高存在分歧,一些分析師將目標價設定在 300 美元、205 美元和 225 美元,並普遍認為其將飆升。作者:埃莉諾·普林格爾

2026 年 07 月 08 日 07:25:45 [FOT](財富)隨着埃隆·馬斯克的 SpaceX 現已納入納斯達克 100 指數,這家火箭公司的前景——直接或間接地——現已進入全球數百萬人的股票投資組合。但加入納斯達克指數並未能説服批評者,他們對該公司的高遠目標持懷疑態度。在其發行前的招股説明書中,SpaceX 表示其目標是 “建立使生命多行星化、理解宇宙真實本質以及將意識之光延伸至星辰所需的系統和技術。”

投資巨頭 GMO 的聯合創始人傑裏米·格蘭瑟姆表示,此類聲明對未來的投資者來説將是可笑的。誠然,這位英國億萬富翁投資者以其懷疑態度而聞名:他自稱是 “永久看空者”,並警告 AI 的影響將導致 “血流成河”。

那麼,他對 SpaceX(字面意義上)超脱塵世的意圖不以為然或許並不令人驚訝。格蘭瑟姆在今天早上發佈的一期晨星的《長遠觀點》播客中表示:“每個人都在排隊告訴你購買人類歷史上最瘋狂的 IPO”,“50 年後,他們會講述和撰寫關於 SpaceX 的故事,他們會引用招股説明書中的段落給你聽,而你將會嘲笑它。”

自 SpaceX 上市以來,即使是最看漲的投資者可能也感受到了現實的檢驗。在撰寫本文時,SpaceX 在過去一個月下跌了 7%,股價徘徊在每股 150 美元左右——僅略高於其上市時 135 美元的目標價。

華爾街對 SpaceX 能飛多高存在分歧,儘管他們普遍認為其將飆升:例如,據報道摩根士丹利將目標價設定在 300 美元,而高盛的埃裏克·謝里丹及其團隊在《財富》看到的一份報告中寫道,他們認為其價格更接近 205 美元。

分析師的情緒總體上是積極的。摩根大通寫道,其目標價為 225 美元,並補充説,它認為埃隆·馬斯克到 2031 年達到 1 萬億美元收入的目標是可能的,“但需要在雄心勃勃的時間表上強力執行。”

由道格·安穆斯、塞斯·塞夫曼、塞巴斯蒂亞諾·佩蒂和理查德·趙撰寫的報告強調了一些擔憂,其中之一是 “只有一個埃隆” 這一事實。他們寫道,馬斯克的 “過大的影響力和控制權(82% 的投票權)是 SpaceX 文化、願景和運營戰略的核心,我們相信他的領導力一直是公司成功的關鍵驅動力。同時,這種控制權的集中引發了公司治理方面的考慮,並使公司面臨領導層過渡的風險。”

格蘭瑟姆表示,他對華爾街銀行建議客户購買 SpaceX 感到困惑。他補充道:“最終,現實會顯現,這當然會變成我如此珍視的、回顧歷史時具有里程碑意義的歷史事件之一。順便説一句,如果它不崩盤,那將是驚人的,因為它將需要 AI 如此巨大的發展,以至於我們的整個生活都完全不同。”

即使更高價格的合理性成為現實,世界也將是一個 “奇怪的世界”,並且 “如果我們不被我們的自動化朋友所支配,那將是很幸運的。”格蘭瑟姆補充説,這種 “相當可怕的” 前景比崩盤的可能性要小。”G

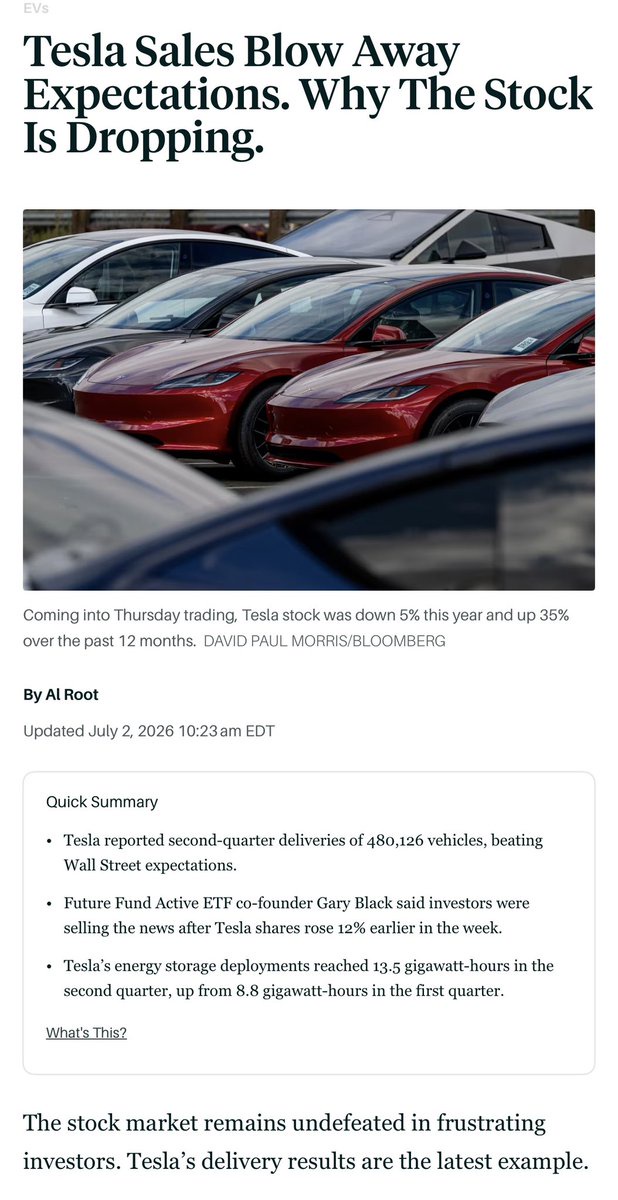

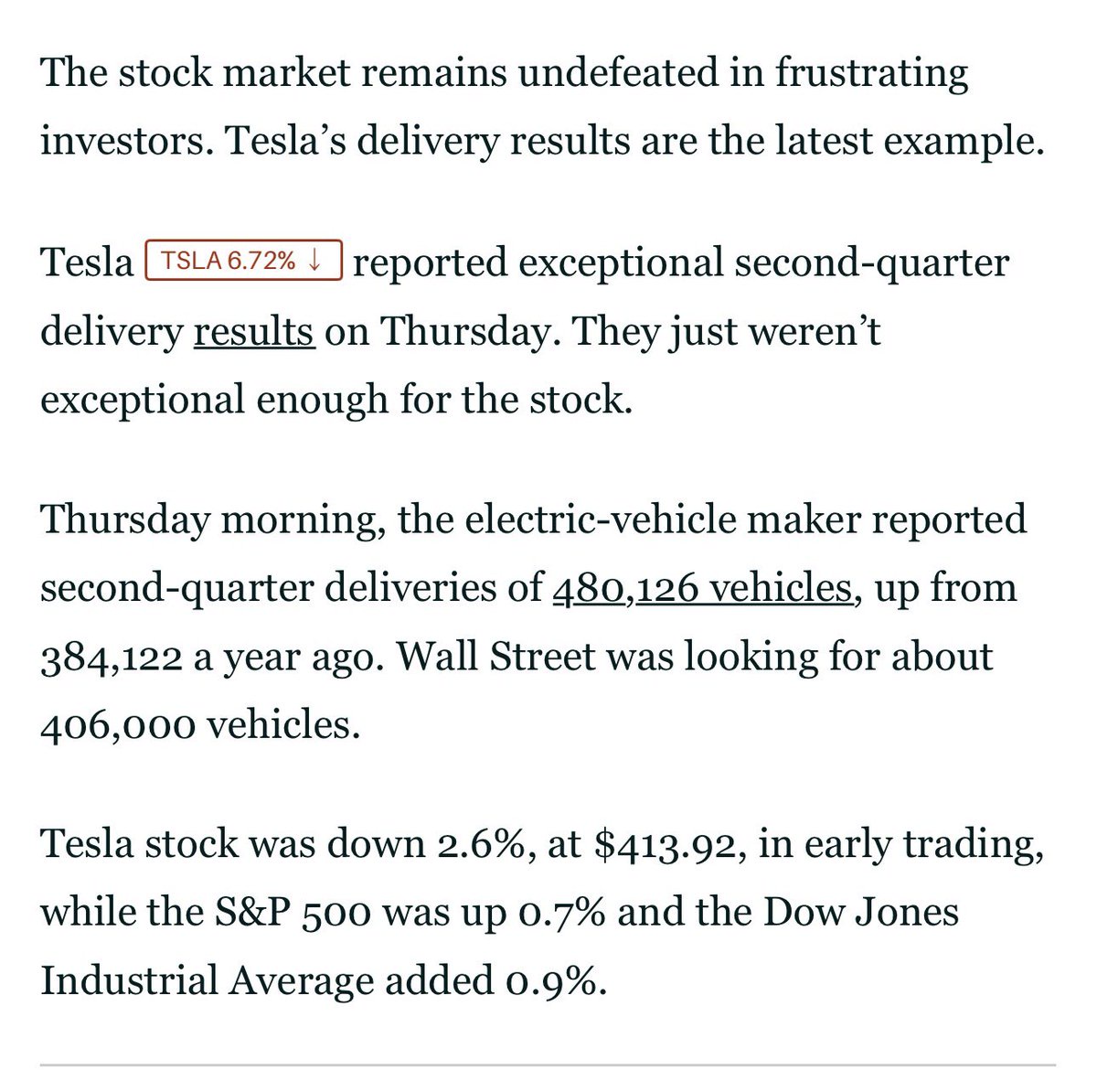

美國股市週一盤前上漲(標普 500 指數 +0.4%,納斯達克 100 指數 +1.0%),科技股在本週三星和 SK 海力士第二季度財報發佈前反彈,這將檢驗人工智能交易熱潮的持續可行性。$特斯拉 (TSLA.US) 在週四下跌 7.5% 並因第二季度交付量(48 萬輛,預期 40.6 萬輛)不及預期而重挫後,盤前反彈 +1.3%,這發生在伊朗衝突導致第二季度油價飆升的背景下。布倫特原油下跌 1% 至 71 美元/桶,因霍爾木茲海峽的石油流量恢復。標普 500 指數 2026 年的每股收益(EPS)預期已升至 342 美元(同比增長 23%),這意味着 21.9 倍的市盈率和 4.6% 的收益率,與 10 年期國債收益率持平。考慮到未來一年無監督自動駕駛技術可能商品化,以及相對於遠期盈利增長(6 倍 PEG)估值過高,我對特斯拉仍持謹慎態度。

G

美國 - 伊朗戰爭前,每加侖汽油的平均價格是 2.98 美元,在六月份達到 4.56 美元/加侖的峯值後,於七月四日週末期間上漲至 3.86 美元/加侖。汽油價格上漲很可能是導致第二季度電動汽車交付量同比激增的原因($特斯拉(TSLA.US) +25%,$Rivian Automotive(RIVN.US) +14%,$Lucid(LCID.US) +20%),而非近期 FSD/自動駕駛技術的進展,這些技術對大多數潛在電動汽車客户來説仍然幾乎不為人知。

歐佩克 + 已初步同意在八月再次適度提高石油產量配額,如果美伊和平協議能夠維持,這將增加更多供應最終再次衝擊市場的可能性。

如果週日的視頻會議批准,以沙特阿拉伯和俄羅斯為首的七個主要國家將把其產量目標提高每日 18.8 萬桶。這些紙面上微小的增幅開始累積:這意味着自戰爭開始以來,它們已將配額提高了每日 94 萬桶,相當於全球需求的近 1%。

石油期貨價格已從四月底戰時每桶 118 美元的峯值暴跌 43%,至今日的每桶 72 美元,許多預測者預計全球供應過剩將再次出現。歐佩克及其合作伙伴可能很快面臨在限制產量或通過潛在的價格戰爭奪市場份額之間做出選擇。

我預計$特斯拉(TSLA.US) 股票本週將反彈,因為賣方分析師爭相提高第二季度和 2026 財年的盈利預期,這可能會推高 TSLA 的目標價。話雖如此,考慮到其 2026 年市盈率超過 200 倍,而長期(2027-2032 年)每股收益增長率為 +35%,這相當於 6 倍的市盈率相對盈利增長比率,而$英偉達(NVDA.US)、$谷歌-C(GOOG.US)、$Meta(META.US)、$博通(AVGO.US) 等公司的該比率約為 2 倍,我仍然認為$特斯拉(TSLA.US) 的估值已完全反映在價格中。

G

+1

+1

$特斯拉 (TSLA.US) (今日-7%) 第二季度交付量遠超預期。 但投資者已提前預料到這一表現。

+1G

$特斯拉 (TSLA.US)(盤前 +0.7%)第二季度交付 48 萬輛汽車,同比增長 25%,遠超華爾街預期的 40.6 萬輛。若不計入即將停產的 Model S 和 Model Y,特斯拉第二季度交付量為 46.7 萬輛,仍同比增長 24%。庫存週轉天數從第一季度的 29 天降至第二季度的 17 天。